- Europe is allocating billions of euros to defence with investments expected to continue to grow

- The sector’s valuation is attractive and growth is well above that of other areas

- Industrial and technological resilience remains a key policy focus and boasts multiple potential long-term investment opportunities

This article is part of our 2026 Investment Outlook.

Europe is deepening its quest for strategic autonomy. What began as a post-pandemic policy slogan has evolved into a financial reality, with tangible investment implications – Europe now allocates billions annually to defence, industrial resilience, and key technology sectors.

Once an afterthought, now a priority, the money being put into European defence has significantly increased since 2022, amid the Russia/Ukraine conflict and more recently because of US President Donald Trump’s pressure on NATO members.1

But this is only the beginning. At the June 2025 NATO Summit in The Hague, allies made a commitment to investing 3.5% of GDP annually on core defence requirements and 1.5% of GDP on defence- and security-related spending by 2035.2

These ambitious targets were met with some prudence by the market, with some countries more reluctant than others to spend so much while already struggling with high public spending. However, the path is clear: several plans exist to help with this target, notably the European Union’s (EU) €800bn ReArm Europe Plan/Readiness 2030.3 Security spending will rise for years to come, which could create potential new opportunities for investors.

Investable market

The total addressable market for European defense companies should grow 29% per year until 2030, according to Oddo BHF. Its study uses a hypothesis of 3% of GDP spending on defence by 2030 (versus the 3.5% agreed by NATO members4,5, and 2% previously), taking progressively into account the 65% target of components from European companies, adjusting slightly higher also the proportion of spending on equipment versus staff.

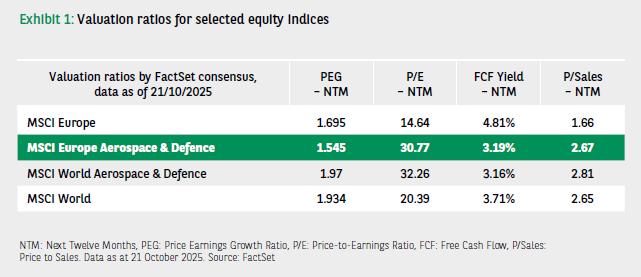

The sector has significantly re-rated since 2022, but its valuation is still below that of US peers and its growth is well above that of the other European sectors.

When looking at the subsector’s valuation ratio, accounting for its growth, the sector is still cheaper than the rest of the market.

In the short term, investors should be prepared for potential volatility, due to contradictory news on the probability of a ceasefire between Ukraine and Russia. But recent financial reports and order books have reassured the market; for example, TKMS (the recent marine spin-off from ThyssenKrupp) boasts backlogs extending to 2040.6

At the same time, the reorganisation of the European defence landscape is underway, evidenced by several changes: TKMS’ spin-off, Rheinmetall’s acquisition of Naval Vessels Lürssen, the Bromo satellite project combining the space businesses of Airbus, Thales and Leonardo – which all create potential additional opportunities to invest in the sector.

Industry, IT, utilities and basic resources

The industry, information technology, utilities and basic resources sectors are pillars to address vulnerabilities in supply chains, notably in chips, energy and critical raw materials essential for the green and digital transitions. Several policies and plans exist to support this:

- The EU’s REPowerEU programme which aims to divest from Russian energy imports before 20307: supported by €300bn of funding, notably through the Recovery and Resilience Facility8

- Approximately €100bn to be mobilised by 2030 to support decarbonation of energy-intensive industries9

- Germany’s Schuldenbremse (debt brake) reform, approved by parliament in March 2025, enabling the creation of a special €500bn fund to be deployed over several years (€83bn for 2026) dedicated to investments in infrastructure (transportation, energy, digital networks) and the green transition10

- The EU’s Critical Raw Materials Act which establishes benchmarks for EU extraction (10%), processing (40%), and recycling (25%) by 2030. It does not have a dedicated budget but aims to soften the administrative burden and timeline for permits.11 This initiative becomes more and more important with the Chinese government restricting rare earth material exports

- At the European level, the Chips Act is mobilising over €43bn in public-private commitments through 203012

On an even longer-term note, the Multiannual Financial Framework proposed by the European Commission in July 2025, covering 2028–2034, provides for a budget of €2trn aimed at strengthening the EU’s strategic autonomy and resilience. This is equivalent to 1.26% of EU GDP over the seven-year period, doubling the €1trn of the previous 2021-2027 budget.13 The plan establishes a European Competitiveness Fund of €409bn, intended to support strategic technologies in clean energy, digital transition, biotechnology, and defence.

In addition, €175bn is allocated to Horizon Europe, the EU’s flagship research programme, which aims to support innovation from conception to scale-up. This additional spending will likely open up new investment opportunities across these industries and potentially beyond.

A long-term investment trend

Europe’s strategic autonomy could solidify by 2030, with defence spending representing a significant 3.5% of the region’s GDP, not even taking into account the indirect 1.5% of GDP spending from the NATO commitment. Even if the full NATO engagement is not met, we believe this is a structural trend that is here to stay. Defence clearly dominates Europe’s balance sheet, while industrial and technological resilience remain smaller but fast-growing components as well. Sustained efforts are essential for a robust Europe, improving visibility for European companies, while creating potential long-term opportunities for investors.

[1] Defence Expenditure of Nato Countries 250827-def-exp-2025-en.pdf

[2] NATO – Topic: Defence expenditures and NATO’s 5% commitment

[3] EU defence funding | Epthinktank | European Parliament

[4] European Defence Agency Report, Defence Data 2024 – 2025.

[5] SAFE | Security Action for Europe – European Commission

[6] Major order of € 800 million for submarine modernization – TKMS Group Website

[7] RE PowerEU

[8] Recovery and Resilience Facility – European Commission

[9] Clean Industrial Deal – European Commission

[11] Critical Raw Materials Act – Internal Market, Industry, Entrepreneurship and SMEs

[12] European Chips Act – European Commission

[13] EU budget 2028-2034