Exchange-traded funds aim to provide investors with a simple, cost-effective way to invest in assets such as stocks, bonds, or commodities by replicating a market index (or strategy). Replicating the performance of an index can be done in various ways: rebuilding the index by including all its stocks or bonds in a portfolio or using ‘synthetic replication’. Paul Xatard-Huberlant explains.

Features of a synthetic ETF

Investor interest in this approach, which uses a derivative such as a swap to replicate an index’s performance instead of buying the index’s underlying assets outright, is back: synthetic ETFs have been regaining market share.

The renewed appetite for ETFs follows a spell in which investors shunned products with counterparty risk. In synthetic ETFs, the risk relates to the financial institution that delivers the index performance and the risk that this institution defaults on its obligation and is no longer able to supply the performance. In particular after the 2008 financial crisis, investors worried about default risk.

Other concerns surrounded transparency. The complexity of synthetic ETFs kept investors looking for more straightforward funds. Regulatory scrutiny and negative publicity over synthetic ETFs as ‘black boxes’ deterred retail and even institutional investors.

In the meantime, improved regulations, including tighter rules on the use of collateral as a way of reducing counterparty risk, have helped to turn the tide. When the swap value changes, collateral is adjusted daily. If the swap counterparty defaults, the ETF still retains the cash collateral and can unwind or rebuild the position.

Investor calls for lower expense ratios for investment products in general have brought low-cost synthetic replication back into focus, as have tax advantages in selected jurisdictions.

Finally, liquidity has improved, and ETFs now often use multiple counterparties, reducing risk, and improving pricing.

Overall, we believe synthetic replication can now offer returns that exceed those of physical replication.

A look at the pros and cons of synthetic replication

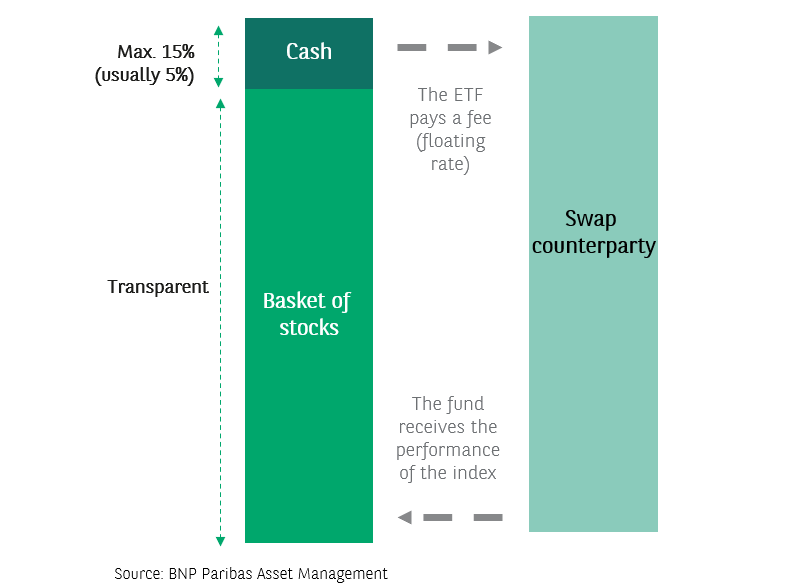

For a synthetic ETF, the replication is indirect – it is based on a swap transaction. The ETF enters into a contract with a bank or financial services provider which, in return for a fee, provides the index return. This process, known as a total return swap, is used for traditional synthetic replication.

The main feature of this approach is that there need not be a connection with the composition of replicated index. Theoretically, synthetic fixed income ETF may hold a substitute basket of shares as long as the performance it generates matches that of the chosen bond benchmark. While for an ETF manager, such an approach may simplify fund management, it is less intuitive for an investor.

A synthetic ETF requires less cash to build and entails fewer transaction fees. This approach allows a fund manager to put together a fund replicating a market of assets that are less liquid or even illiquid – and thus unattractive to hold – or a market that is so broad and diverse that buying the underlying assets is impractical – for example, commodities or emerging market stocks.

More traditional – Physical replication

A physically replicating ETF invests directly in the securities making up the index. An investor can thus see for himself what they are holding. So, for a CAC-40 ETF, the fund actually invests in all 40 companies and in the same proportion as their weights in the index.

For an investor, such an ETF is easy to understand. Transparency is high: what you see is what you get. There is a sense of security: as an ETF investor, you own the stocks. For the fund manager, looking after such an ETF requires substantial cash to buy and hold the underlying securities over time. A close check has to be kept on index composition with rebalacing when there are changes. This involves transaction costs which reduce net returns.

Finally, dividend payments or index changes can make replication less accurate, resulting in a higher tracking error relative to the benchmark. this could affect the appeal for investors keen to own a fund that closely replicates index performance.

The alternative – Synthetic ETFs

The absence of a need for full index replication results in lower transactions costs (the manager does not have to trade all stocks). This is particularly relevant when it comes to the costs associated with the replication of large indices and indices with a high turnover.

Synthetic ETFs typically involve more accurate replication (less of a deviation between fund performance and index performance) and can offer investors access to less regulated markets such as Chinese or Indian stocks. In some markets, specific synthetic ETFs may enjoy tax advantages that full replication funds miss out on such as the US dividend withholding tax on qualified index baskets.

Given that the performance swap transaction underlying the fund is provided by a counterparty, there is a risk the swap partner becomes insolvent. We contain that risk by implementing UCITS rules limiting exposure to derivative counterparties to no more than 10% of the fund’s net asset value. Furthermore, we implement strict UCITS diversification and liquidity rules.

We ensure that we choose counterparties from eligible institutions, based on their expertise, experience, and the quality of valuations and services provided. We are now working with a stable pool of eight or nine counterparties.

Furthermore, for synthetic ETFs, it is often unclear which securities the fund actually invests in. This can make it hard for investors to assess the actual risks. Other complexities involve the underlying swap mechanisms and the contract details.

A market in development

More innovative synthetic indexing strategies are being developed in the market, making it even more important for investors to understand the mechanisms of swap-based ETFs. At the same time, we see demand for synthetic ETFs covering markets such as China and India, or even emerging markets in general, from investors keen on cost efficiency and accurate replication.

We believe synthetic ETFs are making a comeback now that tighter regulation is in place. Collateral rules have been strengthened, so that collateral now typically is of a high quality, more diversified and subject to strict regulatory requirements. As a result, many investors now see counterparty risk as well-controlled and transparent.

More cost-aware investors now recognise the attractions of synthetic replication. In addition, synthetic structures can bypass some withholding-tax disadvantages that physical ETFs face and that weigh on their net performance. Thus, the outperformance of synthetic replication appeals to investors and is one of the factors driving the re-emergence of synthetic replication ETFs.