The swing in the US Federal Reserve’s preoccupation from tariff-induced inflation risk to labour market weakness – and the consequential 25bp interest rate cut at its last policy meeting – has been a tonic for financial markets. US equities have gained, and US bond yields have fallen, but complacency concerns are now creeping in.

Listen to the article

While the recent revisions to US non-farm payrolls figures painted the picture of a labour market that is far less robust than was thought so far, subsequent data has indicated the US economy remains resilient.

One concern was that if job growth weakened, consumers would feel less confident and pull back on spending, but August’s retail sales data beat analyst expectations. Importantly, the monthly change in real (inflation-adjusted) sales was also positive, showing that the higher dollar value of sales did not simply reflect price increases as a result of the tariffs on imports into the US (see Exhibit 1).

On the business side of the economy, industrial production data came in better than forecast, showing growth rather than the contraction that had been forecast. The main weak point in recent data was housing starts, but with interest rates moving down, they, too, should begin to recover.

China – A halting recovery

In contrast to the US data, China’s retail sales were flat versus July. It is disappointing that they have remained so weak. The numbers for the month after the government’s growth-boosting trade-in programme in May had been forecast to be negative: these sorts of initiatives generally pull demand forward rather than increasing it.

However, July’s sales growth was also negative (albeit less so), while sales in August were merely flat.

This is a far slower pace of recovery than many had expected. One hopes the upcoming discussions between Chinese President Xi Jinping and US President Donald Trump provide some relief for the economy.

The strongly positive figures for the UK economy are one of the few bright spots for the country, as investors focus on debt levels and Gilt yields, and anticipate tax hikes in the upcoming budget. The UK equity market was one of worst performers last week.

Impact of interest rates on equity markets

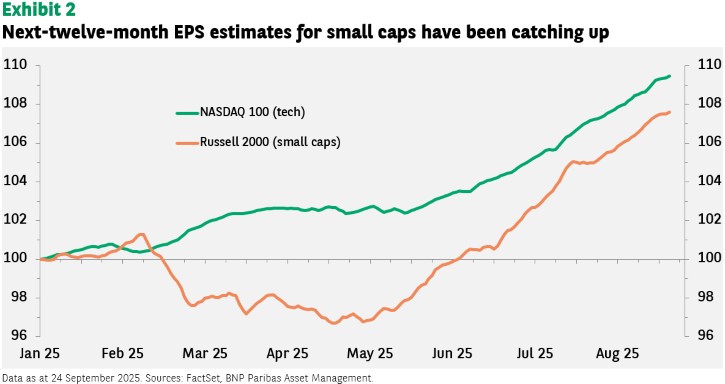

Those parts of the equity market most sensitive to interest rates are technology stocks, due to the long duration of their earnings, and small-cap stocks, given their strong link to domestic demand.

So, it is no surprise that the tech-heavy NASDAQ 100 and Russell 2000 indices have been among the best performers over the last few weeks. The positive momentum in the US economy should continue to support these indices in the months ahead.

Success, however, creates its own challenges. The sharp rise in stock prices has outpaced earnings growth forecasts, leading to high forward price-earnings ratios. The forward P/E for the NASDAQ has now reached 28x, while for the Russell 2000, it is 25x – both are now a decent amount above their long-run averages.

Assuming one believes these figures will revert to their respective means, the question is how. Echoing US FCC Chair Brendan Carr1, it can happen “the easy way or the hard way.”

- The easy way is that earnings rise faster than index prices, leading to a compression in the multiple, though this suggest returns from here will be somewhat lower.

- The hard way is that prices fall sharply. While the latter is always a risk, barring a negative catalyst, we do not anticipate such a scenario in the near term.

The scenario of the index ‘growing into the multiple’ is conceivable for both indices.

- A pickup in earnings for NASDAQ stocks would stem from the return on the massive capital expenditures by companies to develop artificial intelligence capabilities.

- For small capitalisation shares, the forecast trend of earnings is so high that multiples could compress quickly while still allowing for attractive gains in the index price (see Exhibit 2).

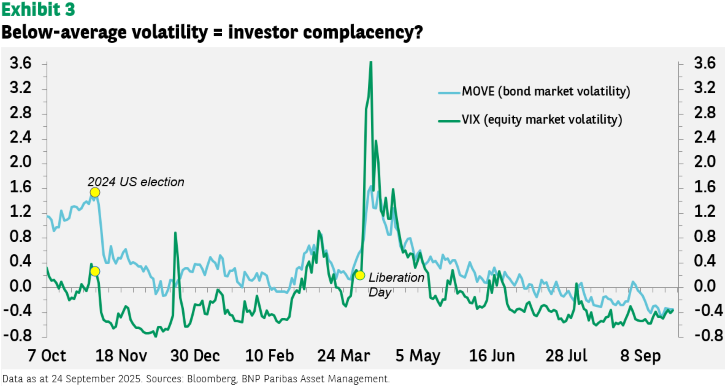

Low volatility = complacency?

The other warning sign, however, can be seen in the volatility indices for both US equities and fixed income markets – both are well below average (see Exhibit 3).

While investors have been keen to participate in the market gains (the FOMO factor: Fear of Missing Out), volatility is likely to revert to mean levels, which would entail lower equity prices.

Fixed income yields could go either way given the multiple factors at play (market concerns over the Fed’s independence, term premia, inflation expectations, and economic growth).

Investors looking to hedge this risk appear to prefer gold. The yellow metal has continued to hit all-time highs. Its price has also been supported by lower US interest rates: lower rates reduce the opportunity cost in terms of interest income foregone by holding gold.

Our multi-asset teams concur on the view that gold is worthwhile holding on to – despite its gains over the last 12 months – while awaiting the next (unpleasant) surprise for the markets.

[1] https://www.fcc.gov/about/leadership/brendan-carr