Euro fixed income has a wide range of performance drivers that can enhance portfolio diversification. Credit spreads are tight, but there are still opportunities to capture historically absolute high yields. With eurozone inflation at target, growth resilient, and a positive fiscal profile relative to other developed economies, fundamentals are solid.

In the context of higher economic and political uncertainty and market volatility, a flexible and dynamic approach should enable investors to navigate market cycles.

Euro fixed income became the byword in 2025 for those investors looking to diversify away from US policy-driven uncertainty. Currently, concerns over US tariffs have diminished and the appointment of a new US Federal Reserve chair looks less contentious. In Europe, fiscal slippage has boosted already heavy debt supply. Can euro fixed income still attract investors?

We believe there are five reasons to consider euro fixed income as part of an investor’s bond allocation:

Exposure to multiple performance drivers

A wide range of performance engines can enable portfolios to navigate market cycles. Indeed, the euro segment offers exposure to a multitude of sovereign bonds as well as quasi-sovereigns, both investment-grade and high-yield debt.

In 2025, despite sovereign debt not contributing strongly to overall returns, some countries performed far better than others. ‘Peripheral’ sovereign debt, for example, outperformed core eurozone sovereigns by nearly 3% due to greater fiscal discipline and brighter growth prospects.

The same goes for euro investment-grade credit. Thanks to sound margins and a resilient economy, it delivered more than 3% returns. The subordinated IG segment delivered more than 5%.

This diversification of the sources of return highlights how active bond management can affect returns and offer opportunities in 2026.

Euro bond yields near historical highs

Many bond investors may naturally turn to high-yield bonds to enhance income, but they are not necessarily being paid for the additional risk of going down the credit quality spectrum given already tight spreads.

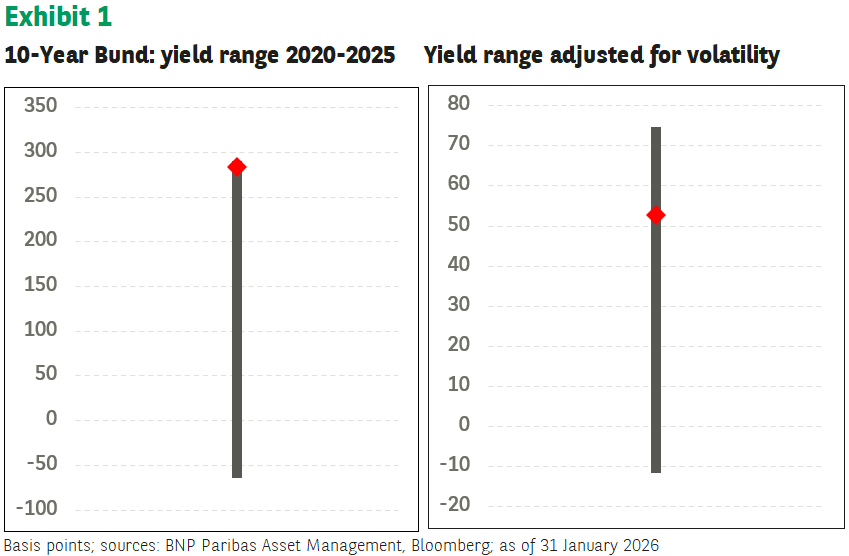

This environment is where the high quality and diverse nature of euro fixed income can play an important role. At close to 3%, the 10-year German Bund yield is back at 2011 levels and well above its 1.8% average over the past 20 years.

Meanwhile, money market rates have declined as the ECB cut rates to 2%. At the same time, 10-year US Treasury yields are now far off their 5% highs. Back in the 4.20% range, this gives 2.50% once hedged back to euro.

Rates volatility initially doubled in 2022 and the years following. Yet in 2025 this reversed. Rates rose further but this wasn’t accompanied by a pick-up in volatility. This divergence is important: not only are 10-year Bund yields historically high, but they are also high when adjusted for volatility.

We believe that this makes euro bonds look particularly good both in absolute and relative terms and offers investors a compelling investment opportunity.

Eurozone fundamentals look good

Inflation is now at the ECB’s 2% target and could undershoot that objective in 2026. Even when considering the German fiscal plan, the eurozone’s budget deficit is expected to stay slightly above 3% of GDP. This is a different picture from the US where inflation is still well above the Federal Reserve’s target, and the administration’s budget deficit might head towards 6%.

In the meantime, the eurozone economy is expected to increasingly benefit from additional fiscal spending, supporting the area’s growth prospects and company fundamentals. Hence, with inflation now under control, better growth prospects, more fiscal leeway, and a neutral central bank rate, euro fixed income appears to be in a good place.

A strong role of drawdown mitigation

Fixed income generally plays a defensive role in a multi-asset global allocation. In risk-averse periods when equity prices drop, bonds should act as a buffer thanks to declining yields.

Allocating to fixed income is generally not about seeking to enhance returns, but rather about managing the portfolio’s risk profile. Indeed, historical data shows that mixing fixed Income and equity reduces maximum drawdowns without affecting the Sharpe ratio.

At a time of high uncertainty after years of strong equity returns, this might be a good time to think about drawdown mitigation. In this context, euro fixed income, which has the lowest correlation to equity compared to other fixed income segments, looks particularly appropriate and could act as a safe haven.[1]

Higher volatility: opportunities to enhance returns

While euro fixed income’s volatility fell in 2025, it remains well above the average of the past 10 years.

Interestingly it is the rates component of volatility that has driven the sharp rise in volatility over the past four years. Currently, rates volatility contributes almost 90% of the euro fixed income volatility compared to a historical average closer to 75%.

We believe this volatility offers opportunities. Over 2025, the 10-year Bund yield rose by almost 50bp. There were 10 moves of more than 30bp, four of them being downward. This is an argument for active and flexible duration management as it not only mitigates rate sell-offs, but it can also fully exploit rate rallies.

In a world defined by unpredictability and multiple tail risks, volatility is here to stay and the opportunities to enhance risk-return profiles along with it.

Conclusion

We believe euro fixed income is worth a look in 2026. It offers liquid and diversified exposure to a range of sovereign bonds as well as quasi-sovereign and IG credit. There are myriad opportunities for investors willing to actively exploit the segment’s multiple performance drivers, from duration management to asset and geographical allocation.

At a time of historically tight credit spreads, investors are not necessarily being rewarded for taking on additional risks. A diversified and flexible exposure to euro bonds may therefore be relevant, particularly as part of a broader allocation rather than on a stand-alone basis.

[1] Source: BNP Paribas Asset Management, as of 31 December 2025. Based on 10‑year (2015-2025) analysis of average annual absolute correlations. The Euro Agg index had the lowest correlation with MSCI World compared to Euro Gov, Euro IG, Euro HY, Global Agg, Global IG, Global HY and Global Treasury).