We view the current strength of US GDP growth as heavily reliant on the investment boom related to AI, both in terms of capital expenditure and the wealth effect of surging equity valuations. Without this support, we think the negative impact of tariffs and uncertainty over growth and employment would have been more evident. Nonetheless, we anticipate further rate cuts from the US Federal Reserve as it pursues an accommodative monetary policy.

Although the Artifical Intelligence (AI) investment cycle is probably still in its early stages, equity valuations are clearly stretched, meaning that AI stocks need to deliver on ambitious earnings forecasts to justify valuations. This provides considerable scope for an AI-sector equity pullback that would have negative consequences for confidence, consumption and investment.

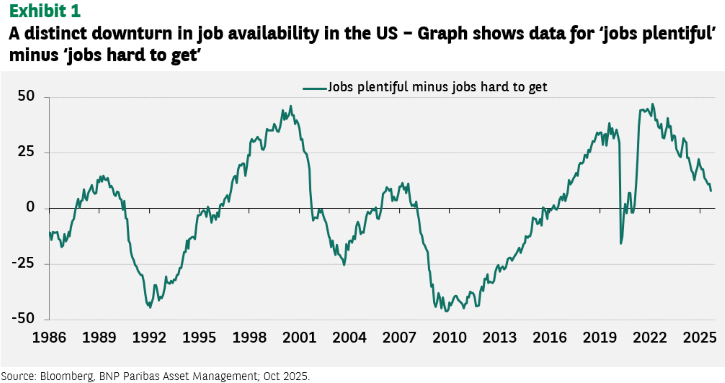

No hiring, no firing status quo in US job market

In the meantime, US labour market data after significant revisions is showing a notable deceleration in hiring, mostly – but not entirely – explained by tighter immigration policies and stalling participation rates. So far, the job market is characterised by a ‘no hiring, no firing’ status quo.

However, with private sector job creation threatening to turn negative and surveys suggesting jobs are increasingly hard to find, the probability of an external shock starting a wave of layoffs is, in our view, not small. Tariffs, for example, will lower profits and squeeze household purchasing power.

In addition, the Department of Government Efficiency (DOGE) layoffs from the first and second quarters will be counted in October, and the federal government is also threatening to fire employees during the shutdown rather than furlough them.

For these reasons, we expect US payrolls data to deteriorate further in the fourth quarter. Looking ahead to 2026, however, we are mindful that fiscal policy is set to deliver a modest 0.3% boost to GDP growth, that the tariff impact will be largely behind us, and that the administration’s deregulation agenda could be supportive of growth. In addition, should they be delivered, foreign pledges of direct investment into the US could provide another source of investment and growth.

US inflation to run above Fed’s target

On the inflation side, we expect tariffs to contribute 80-100bp to the overall US consumer price index over some nine months, beginning around May 2026. This impact is likely to be a one-off and will reduce real incomes. Businesses will also likely absorb a large proportion of the tariff bill, with implications for profits.

A soft labour market is likely to prevent second-round effects via higher wage demands. But we nevertheless expect the less open, more protectionist environment promoted by the Trump administration to have longer-term consequences for prices. In addition, the surge in electricity demand from AI datacentres looks set to maintain upward pressure on energy prices for some time. All this suggests a normalisation of inflation after the tariff-induced peak.

Our view is that US core CPI inflation will have difficulty returning to the 2.3% level that is consistent with the 2.0 % target for personal consumption expenditures (PCE).

Accommodative monetary policy from the Fed

In the absence of a sudden deterioration in labour market data, the policy-setting Federal Open Market Committee will wish to be cautious about cutting rates and signalling a destination for the policy rate.

The minutes of the September FOMC reveal two groups on the committee:

- A hawkish group that is uneasy about cutting while overall financial conditions are loose, inflation remains above target and tariffs are driving prices higher

- A dovish group focused on rising unemployment. They see the divergence between growth and employment gains as indicative of accelerating productivity and tariffs as a one-off inflation story. For these reasons they think policy rates are still restrictive.

To clarify, we have much sympathy with the hawks, but the risks of further labour market deterioration over the next three months appear significant to us, and we think negative data on payrolls would force the Fed into a faster cutting cycle.

Over the next 12 to 18 months, though, we remain of the opinion that political pressure on the Fed, possible personnel changes on its board, and Chairman Jerome Powell’s replacement as Fed chair in May, will impact the FOMC’s reaction function, leading to a marginally more accommodative policy stance that is more tolerant of inflation overshoots. That is likely to result in rates being held below levels consistent with a prudent Taylor rule.

We now expect the Fed to lower rates twice more in 2025, and at least three times in 2026, taking policy rates below 3.00%.

Over time, of course, persistent tolerance of inflation in the upper end of a 1-3% range is likely to beg the question of whether the central bank has effectively raised the inflation target. Put another way, we note 2026 will be the sixth consecutive year in which core PCE inflation could print above the Fed’s target, and we see no realistic appetite within the FOMC to ensure that 2026 is the last year of an overshoot.

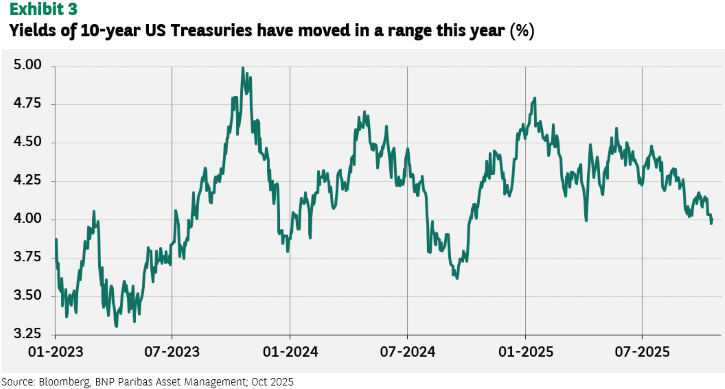

Views on US Treasuries

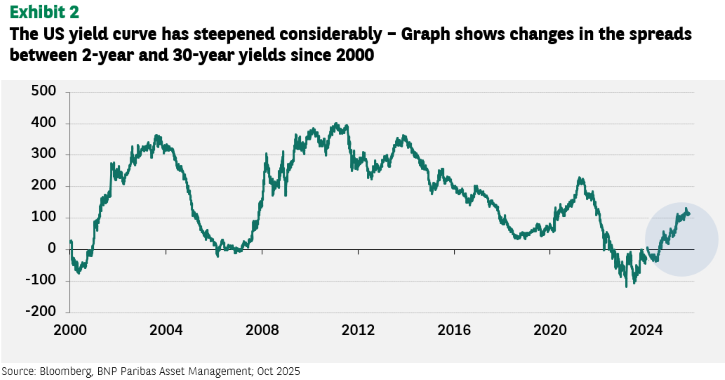

We expect further steepening of the US yield curve between 5 and 30 years. The curve shifted higher and steepened for much of the third quarter taking the US 5s30s Treasury curve to a peak of 125bp.

Although there was a sharp reversal towards the end of the third quarter, with longer-dated bonds outperforming short maturities, we believe the fundamental arguments for higher term premia and a steeper curve still hold.

The primary driver for a steeper yield curve has been investors pricing in a softening of the US labour market and a one-off tariff impact on inflation. This has opened the way for the Fed to focus on the employment side of its mandate and resume the rate cutting cycle.

We expect the Fed to take official rates to below the 3.00% ‘neutral’ level in 2026. We anticipate more Fed cuts than are currently priced into the market. For longer-dated US Treasuries, we think inflation and sovereign credit risks are not sufficiently rewarded.

The risk to our expectation of a steeper yield curve comes from the prospect of further positioning unwinds into year-end or the prospect of the FOMC defying political pressure and choosing to focus on upside inflation risks rather than downside employment risks. Curve steepening could also be thwarted if the US Treasury decided to shift issuance away from 30-year bonds to five and 10-year T-notes.

For the moment, we do not expect 10-year US Treasury yields to move into a range below 4.00%.