Just over half a dozen large-cap stocks make up a ballooning share of the US equity market’s overall capitalisation1, in particular of the S&P 500 and the tech-heavy NASDAQ indices. The main driver of this outsized presence is the exceptional performance of the ‘Magnificent 7’ mega stocks. Does such a degree of market concentration matter? Raul Leote De Carvalho explains.

A high level of concentration in the US equity market’s capitalisation has made it tough to construct portfolios with a high level of conviction without either significantly underweighting or overinvesting in stocks with the largest capitalisation relative to the index.

Consequently, these large stocks have been dominating the contributions to the excess returns of high-conviction funds1 over the benchmark. That has complicated efforts to outperform benchmark indices.

The risk of underperforming the index has been high since high-conviction portfolio managers have been forced to fund their investment ideas by selling more of this handful of increasingly larger cap stocks. Moreover, in many high-conviction funds, traditional diversification rules and, in some cases, regulatory constraints designed to ensure portfolio diversification have prevented fund managers from holding big exposures to these weighty stocks, even if they wanted to.

The Magnificent-7 – What a run

In 2023 and 2024, the Mag-7 companies significantly outperformed the broader market, with an aggregate net return of 155% over the two years. In contrast, over the same period, the S&P 500 and NASDAQ excluding the Mag-7 gained only 23.7% and 0.6%, respectively.

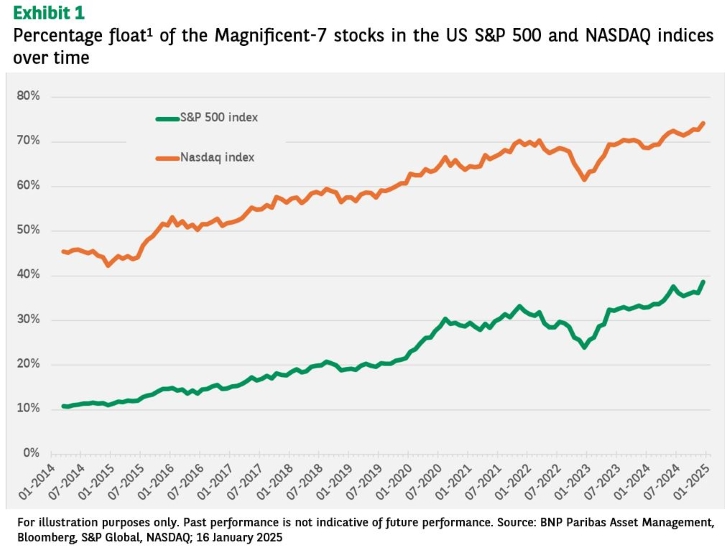

The share of the Mag-7 in the NASDAQ has risen by more than one-third from December 2014; in the S&P 500, their share has risen almost four-fold. That leaves the level of concentration of the US stock market at an all-time high – even more so than during the dot-com bubble of the late 1990s (see Exhibit 2).

The net income of the top 10 largest stocks has generally kept pace with their market cap growth. Currently, the valuations of the top 10 are akin to those of the other 490 S&P 500 stocks. Top-10 valuations may not look cheap now, but they are not as high as in 2000.

Beware the tracking error risk

Investors holding exchange-traded funds (ETFs) replicating market capitalisation weighted indices such as the S&P 500 or the MSCI USA may have been served well in the last few years. They have profited from being invested in these large-cap stocks while they grew in size. However, those investors could now be at risk.

While, as said, these large-cap companies have demonstrated an exceptionally strong earnings track record over the last few years, further increases in concentration will likely require sustaining this extraordinary net income growth. It may become increasingly challenging for them to maintain such a level of income growth.

Investors may now want to protect themselves against the risk of being overexposed to these large companies. If so, they could buy an active fund and delegate the timing of reducing the weight in these large caps to the fund manager or at least the diversification of the portfolio.

Another approach could be to invest in an equally weighted ETF. That would decrease the exposure to very large stocks and increase the exposure to smaller companies in the S&P 500.

This is an abbreviated version of our investment note The increasing concentration of the US equity market available here.

[1] High-conviction strategies invest in a small number of securities. Potential benefits of a more concentrated approach include higher returns, while potential risks include higher volatility, increased risk of loss, and possibly greater stress given the ‘bigger bets’ on a narrow group of stocks.