Global corporate bonds have done well so far this year despite spells of economic uncertainty and geopolitical volatility. While those factors remain, we are positive on the asset class. We see support from robust growth in the US, demand for corporate bonds as investors search for yield, and the US monetary easing cycle.

Global corporate bonds have returned 2.93% for the year through 29 October 2024. This compares to 1.17% over the same period for global government bonds (all data from Bloomberg Global Aggregate indices for returns hedged into euro).

That is an attractive pick-up for investors seeking incremental yield. With corporate balance sheets generally still in good health, we remain positive on allocations to corporate debt.

While the historical data is somewhat mixed on how corporate bonds perform during an rate cutting cycle, our analysis suggests that in each instance where there was either no recession or only a minor one, corporate bonds did well relative to other asset classes.

Lower interest rates in the US should support the outlook for companies not just there, but across the developed world, while declining global government bond yields could benefit total returns on corporate bonds, even if yield spreads remain stable.

Demand for corporate bonds has remained robust. We do not expect this to change in the coming quarters. Despite uncertainty and volatility, the near-record issuance of investment-grade corporate bonds was quickly consumed — in the US, demand has exceeded supply by 3.7 times year-to-date.

As lower short-dated yields fall with lower policy rates, we could see demand rise further in the coming quarters as investors rotate from increasingly lower-yielding money market funds to higher-yielding corporate bond funds.

We believe strong fundamentals and steady demand justify maintaining exposure to corporate bonds.

Declining volatility in US business cycle – remarkable

Rate cuts in the eurozone and the US should boost economic activity and corporate profits.

The US Federal Reserve’s likely success in achieving a soft landing for the economy signals that the country’s business cycle has evolved. Aside from a short-lived dip during the pandemic, the last time the US was in a technical recession was more than 15 years ago after the 2008 Global Financial Crisis. Compared to the prior 40-year period, when there were eight recessions, the declining volatility in the US business cycle is remarkable.

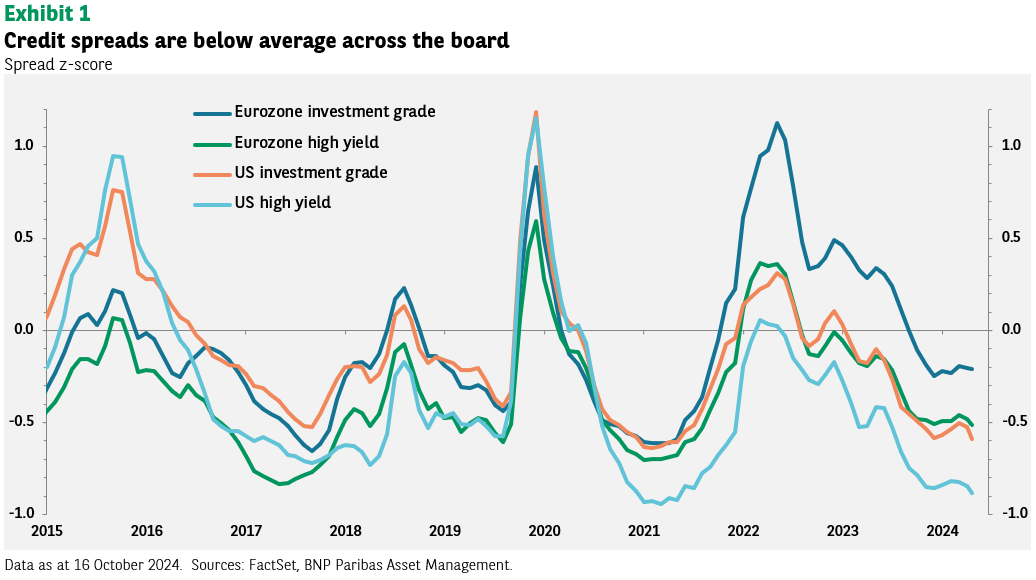

This drop in volatility could reduce the risk premium required for holding corporate bonds over government bonds, allowing corporate bond yield spreads to narrow or at least to stay narrow (see exhibit 1).

Sector and security selection still matter

Softer earnings (and profit warnings) in certain sectors are a reminder that sector and security selection are important for both management and finding opportunities for capital appreciation.

For example, we are increasingly optimistic on global real estate, both in the investment-grade and high-yield markets. Many real estate companies — particularly in the eurozone — suffered when interest rates were high, but falling rates could relieve pressure on their funding costs.

In the banking sector, we believe conditions are supportive for outperformance, but some countries may do better than others. In the eurozone, for example, the ECB has confirmed the sector is broadly resilient, with plenty of capital and liquidity.

However, we are more cautious on the outlook in France given the political and economic environment, and more positive on ‘peripheral’ eurozone markets such as Greece and Spain. Greece looks likely to regain its investment-grade credit rating, while Spain’s economic recovery is accelerating faster than that of many of its eurozone peers.

Finally, we recommend greater selectivity in more cyclical sectors, particularly the car sector. In the eurozone, for example, demand has been tepid, and we expect continued pressure on profit margins from regulations, competition from Asia, and the cost of transitioning to electric vehicles.

Stay invested, but monitor geopolitical risks

While we are constructive on both US and eurozone investment-grade and high-yield credit, bonds have become more expensive, making the asset class vulnerable to worsening investor sentiment. War in Ukraine, increasing tensions in the Middle East, supply disruptions in the Gulf of Arabia — all of these could create market volatility and weigh on sentiment.

Likewise, we expect investors to be cautious ahead of the November US elections. As markets dislike uncertainty, anything short of a clear win by one party or another, with clear policy implications, could increase volatility.