Like shifting sands, fast-moving events are forcing investors to continually readjust their policy and market outlook expectations. Economic prospects for Germany, China and the US now look, respectively, stronger, steadier, and a little weaker than consensus assessments earlier this year.

Listen to the article

Erratic US moves on tariffs are now having a negative impact on investor sentiment and valuations. In the meantime, Germany’s major fiscal policy shift could have implications for the US beyond the short term.

Europe answers wake-up call

Faced with US import tariffs, Europe can no longer rely on exports as a key driver of its economy. The drag on growth from the tariffs could be significant as the eurozone’s exports amount to more than 50% of its GDP, and 20% is destined for the US. The swift response from Germany to the Trump administration’s recent declarations has been to shelve the constitutional ‘debt brake’ and pledge to sharply raise defence spending and infrastructure investment.

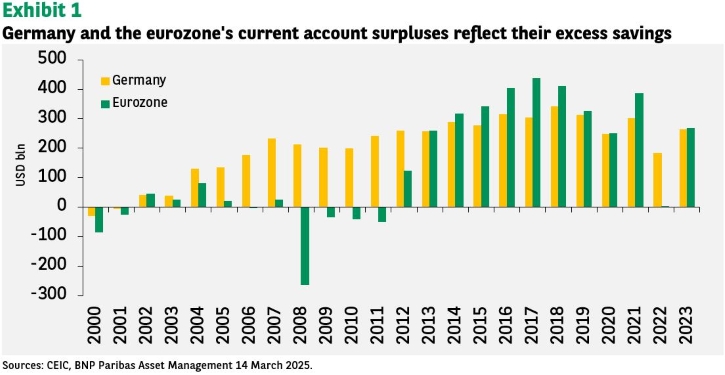

This shift in Germany’s fiscal policy has boosted European stocks, with investors now expecting a turnaround in the country’s economy – Europe’s largest – after two years stuck in the doldrums. Some analysts also argue that concerns over financing larger budget deficits in the eurozone were overblown despite the high debt burden in some countries given that Germany (and the bloc) still have large current account surpluses (see Exhibit 1).

Despite the rise in Bund yields in the wake of the policy pivot, German stock prices rose. The rebound in the eurozone’s industrial production in January (up by 0.8% month-on-month (MoM)) has reinforced the positive sentiment and could drive European stocks higher still.

However, we remain cautious: the eurozone faces strong structural headwinds, such as demographics and issues around productivity growth, on top of the US import tariffs. The EU economies likely all need significant policy support to sustain growth. So far, the magnitude of that support relative to the headwinds to growth remain unclear.

Impact on the US – A weaker dollar

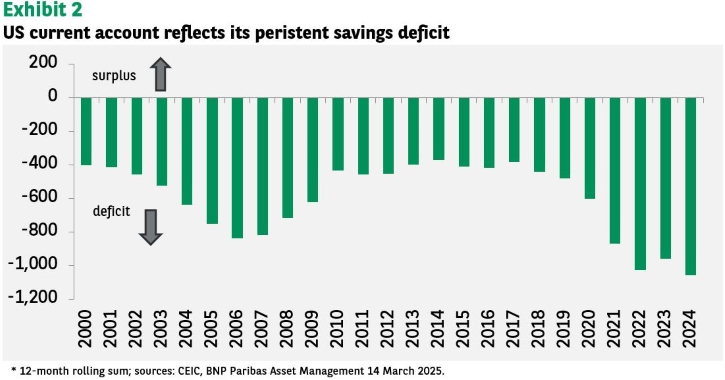

There could be adverse implications for the US. If more eurozone savings are deployed internally, less will flow overseas, notably to the US which runs a large (more than $1 trillion) and chronic current account deficit that needs funding (see Exhibit 2).

A drop in the outflows of the eurozone’s excess savings would likely mean one of two things for the US:

- Higher bond yields

- A weaker US dollar.

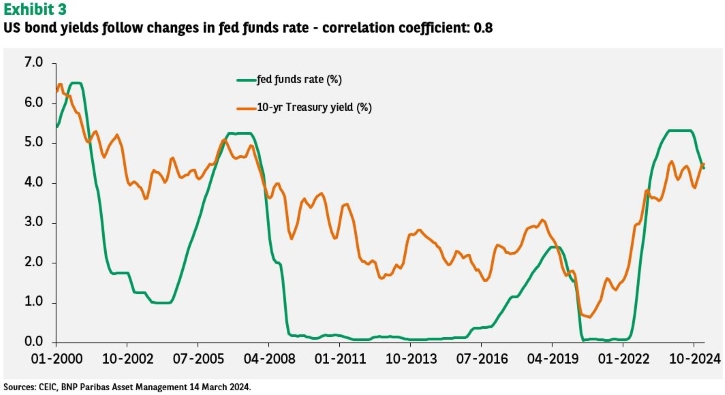

With an open capital account, the US is subject to the ‘impossible trinity’ policy constraint – i.e. with free capital flows, the authorities can control either interest rates or the exchange rate, but not both.

Since the Federal Reserve targets interest rates and not the level of the dollar, US bond yields will largely be determined by the Fed’s policy stance (see Exhibit 3). The dollar would bear the brunt of lower savings flows from the eurozone.

Recent price movements reflect this. US yields fell as the market priced in more rate cuts by the Fed, and as the differential between US and German yields narrowed, the dollar weakened against the euro.

US economy – Weakening ahead

President Donald Trump’s rapid imposition of a range of import tariffs has raised concerns that as a consequence, US growth will slow sharply. There are possibly still more tariffs in store for other countries, including ‘reciprocal’ tariffs, from 2 April.

Both consumer price and producer price inflation slowed by more than expected in February. However, tariffs might cause inflation expectations to rise. Softness in recent labour market and retail sales data is expected to continue as the Department of Government Efficiency has only just started on its staff-cutting plans.

Of the four key vectors – deregulation, fiscal policy, tariffs and immigration – only the first would be a positive for growth. It is not a factor in the Fed’s policy decisions. Implementation of the other three would slow growth. Tariffs can be as the biggest drag in terms of creating uncertainty. They would hit spending and boost short-term inflation; the latter would cause the Fed to delay further rate cuts.

Meanwhile, the fiscal impetus may not be as strong as expected: Democrats and Republicans are finding it hard to agree a spending plan. While the immigration restrictions have not been the market’s main focus, they can still have a double-whammy negative effect as they boost inflation and weigh on growth.

Amid all these crosscurrents, the Fed will likely stand pat on its rate policy in the short term. Once when the slowdown in the economy becomes evident, the Fed could resume cutting rates as long as inflation expectations remain anchored.

China acts for stabilisation

The annual National People’s Congress (NPC) announced economic targets and policies for the coming year that met market expectations. Crucially, the announcements included details on improving policy implementation, reviving private sector confidence, boosting consumption and strategic investment, and supporting key sectors including tech and property.

Furthermore, the NPC emphasised the urban-village renewal programme and pledged to prevent property developer defaults from creating a systemic shock. This suggests that China’s property woes could have bottomed out. Crucially, the leadership vowed to implement the Private Economy Promotion Law.

These are important follow-up measures after President Xi’s high-profile meeting in February with leaders of China’s high tech and private sector companies to revive ‘animal spirits’ and protect the rights of private firms. They signal that the regulatory crackdown on the tech and other private sectors is likely over.

What is important now is delivering on the policy pledges to pull the economy out of the deflation trap and build upon the recent improvement in sentiment towards Chinese assets. Recent AI product launches put Chinese tech stocks back on investors’ radars.

What’s happening this week?

Central bank policy meetings include those of the Fed, the Bank of England, Sweden’s Riksbank, the Bank of Japan, and the Swiss National Bank. The SNB is expected to cut rates by 25pb after its 50bp cut in December, but the other four central banks are expected to leave rates unchanged.

US retail sales for February are expected to have risen by 0.5% MoM after falling by 0.9% in January. Industrial production growth is expected to have eased to 0.4% MoM from 0.5% in January.

We will expect the preliminary reading of 2.4%.for inflation in the eurozone in February to be confirmed.

Lastly, China will release activity data for the January-February period together to smooth any distortions from the Chinese New Year celebrations. Industrial output, retail sales and fixed asset investment are all expected to show small improvements, while property investment is expected to have contracted by less than in the previous months.