Stock markets have stabilised after senior policymakers at the US Federal Reserve suggested policy rates may be lowered next month. Across Europe, efforts continue – in vain so far – to reset fiscal policy, while at the same time maintaining Europe’s welfare state.

Listen to the article

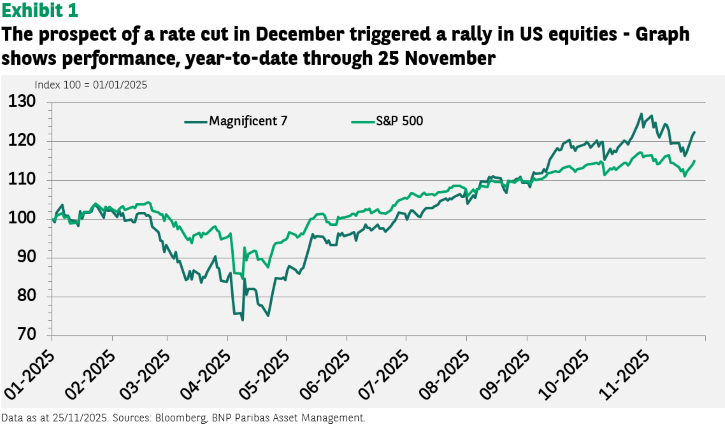

Fed speakers to the rescue

Equity markets have rallied this week after Fed policymakers suggested that a rate cut at the policy meeting on 9/10 December should not be excluded.

On 21 November, vice-chair of the Federal Open Market Committee John Williams said he saw room for the Fed to ease again in ‘the near term’as the labour market softens.

This comment was reinforced by further remarks from Fed governor Christopher Waller in favour of a rate cut based on his view that there is little evidence of rising inflation, while a ‘soft labour market’ is ‘continuing to weaken’.

We expect the Fed to implement this year’s third rate cut of 25bp in December, then lower rates a further three times in 2026.

The comments from Fed policymakers triggered a repricing in money markets, which now price a probability of around 75% for a 25bp cut on 9/10 December (it was 40% before John Williams’ comments).

Not an easy time to be governing in Europe

Across Europe, the last week has delivered more evidence of the difficulties governments encounter as they struggle with balancing the fiscal challenges involved in maintaining the ‘European model’ of a generous welfare state in the face of ageing populations, new security threats, climate change and higher interest rates.

Politicians are only too aware that electorates have repeatedly shown they are not ready to accept the harsh choices that the task of a major reset in public finances imposes.

Flip-flopping in the UK

Chancellor of the Exchequer Rachel Reeves has had to back down and reverse two key fiscal reforms.

Firstly, a set of welfare cuts that collapsed in the summer after a rebellion by members of her own party, followed by a plan to go back on manifesto commitments by raising income tax. This was flagged in the run-up to today’s Budget — only to be suddenly dropped.

Kicking the can down the road in France

The French government clarified last week that a ‘special law’ will be votedonif, as is likely, the budget does not get through Parliament by year-end (i.e., the same procedure as last year after the collapse of the Barnier government).

This law would extend budget discussions into early 2026. The measure may reduce the risk of near-term political instability, but it does not set France on a path to fiscal rectitude.

Pension reform in Germany?

The German Council of Economic Experts delivered distinctly downbeat independent advice in the form of its 600-page annual report to the government. The council forecast that GDP growth would edge up from 0.2% this year to only 0.9% in 2026, below the government’s projection of 1.3%.

According to the council, the government’s fiscal push will deliver 0.3% of growth next year, with a calendar effect (bank holidays falling on weekends) accounting for another 0.3%, leaving just 0.3% resulting from structural growth.

Meanwhile, after only six months at the head of the new coalition government, Chancellor Friedrich Merz faces a rebellion from the youth wing of his own centre-right CDU party over a pension bill it views as too generous to the older generation.

In Germany, it would be unusual for a piece of legislation based on an agreement between the governing coalition partners to determine the fate of a government. In the case of pension legislation, however, this could conceivably now happen.

The ruling coalition of the centre-right CDU/CSU and centre-left SPD agreed on a reform of the statutory pension system with the aim of stabilising the pension level. A group of young CDU/CSU parliamentarians, however, sees this as unjust for the younger generation and rejects the planned law in its current form.

This week, more parliamentarians have joined the rebels. Unless they back down, it will leave the coalition government without a majority, and the painfully negotiated compromise would fail – potentially rendering the coalition significantly more fragile.

But prompt action is necessary

In a note entitled “How Can Europe Pay for Things That It Can’t Afford”, the International Monetary Fund (IMF) this month warned that delaying policy action could be costly as the fiscal position of a number of European states would deteriorate, further complicating the task for policymakers.

According to the IMF’s note, policy delays could mean public debt levels more than double for the average European country over the next 15 years. The result would be higher interest rates, even weaker economic growth, and a negative impact on market confidence.

In high-debt countries, the IMF sees no alternative to a fundamental rethink of the scope of public services and the social contract between the state and citizens.