The implications of the outcome of the US presidential election for financial markets will depend on the policy changes implemented and how other countries react to them. If President-elect Trump delivers on his tariffs and immigration promises, inflation could rise in the short term and hamper growth in the medium term. The US dollar, Federal Reserve policy, and global markets would be impacted.

Listen to the article

First, a look at the latest data

The latest economic data has been a mixed bag.

Underscoring the weakness in US manufacturing, the ISM manufacturing purchasing managers’ index (PMI) dropped to 46.5 from 47.2. However, the non-manufacturing PMI rose by 1.1 points to 56.

The situation in the US labour market is unclear. The data for non-farm payrolls was distorted by bad weather and strikes. It registered job creation of just 12 000 in October. However, ADP data showed private employers added 233 000 jobs during the same period.

The US economy grew by an impressive but slightly weaker than expected 2.8%, against 3.0% reported previously, in the third quarter. Consumer spending remained strong, growing by 3.7%, after 2.8%, despite rising credit card debt and delinquencies.

Crucially, price pressures continued to moderate. The Employment Cost Index showed a 3.9% year-on-year (YoY) rise in the third quarter, slower than the 4.1% of the previous quarter. Personal consumption expenditures (PCE) inflation fell to 1.5% and core PCE to 2.2%, bringing it close to the Fed’s 2% policy target. Non-farm productivity rose, by a solid 2.2%.

Moderating inflation and much weaker growth were apparent in Europe. The eurozone economy grew by 0.9% in the third quarter; inflation came in at 1.7%, down from 2.2% in August. Stripping out the one-time boost of the Olympics in September, economic growth was likely weaker still.

Waiting for more fiscal easing in China

Meanwhile, in a surprise move, economic activity in China improved. Third-quarter GDP beat market expectation by rising by 4.6% YoY as retail sales, investment and industrial output growth picked up.

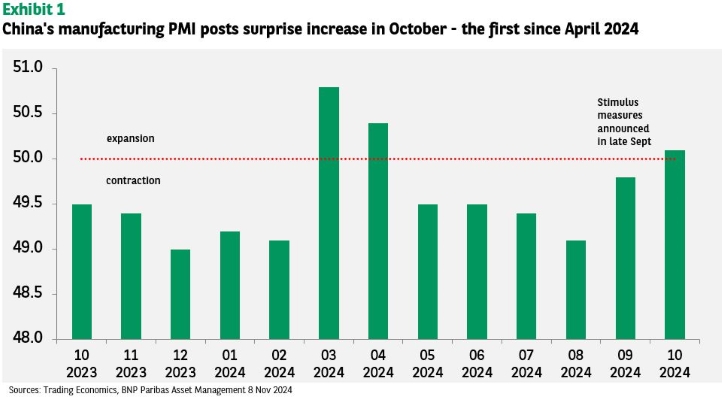

These nascent signs of economic stabilisation were echoed by the October manufacturing PMI, which posted an unexpected increase to 50.1, marking the first gain since April 2024 (see Exhibit 1). The non-manufacturing PMI nudged up from 50.0 to 50.2 in September.

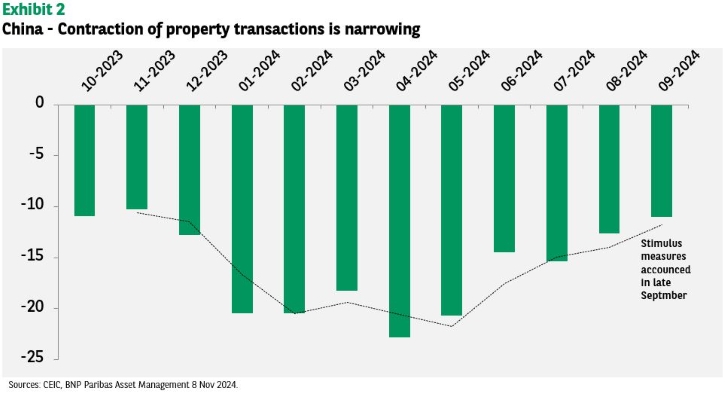

However, the improvement was not felt everywhere: construction and property transactions fell by more than 10% YoY, although the rate of contraction has slowed since April 2024 (see Exhibit 2).

To us, this underscores the need for more fiscal easing to revive China’s growth momentum.

The National People’s Congress Standing Committee on 8 November did not provide any specific fiscal spending for boosting growth. The RMB10 trillion package announced was earmarked for a local government debt swap spread over the next five years.

While the debt swap does not stimulate demand directly, it will help alleviate the debt overhang facing local governments and thus help keep existing deflationary pressures from worsening.

Rate cuts – Should we expect more?

The latest data suggests to us that the global outlook for more cuts to policy rates is intact. For now, there should be tailwinds rather than headwinds for global growth, creating a constructive backdrop for global equities after some post-US election market volatility.

Indeed, the Fed, the Bank of England and Sweden’s Riksbank all cut rates by 25bp in the second week of November, as expected.

After the meeting of the Federal Open Market Committee (FOMC) on 6-7 November, Fed Chair Powell expressed his confidence that inflation would continue to moderate while conditions in the US labour market moderate. He noted that with the fed funds rate at 4.5%-4.75%, policy was still restrictive. This could be seen as signalling another 25bp rate cut from the FOMC in December. Interestingly, but not unexpectedly, he flatly rejected the idea that President-elect Trump could curtail his term (which runs until May 2026) as Chair of the US Federal Reserve.

Tariffs, tariffs, tariffs

Looking further ahead, one macroeconomic risk for global markets is the possibility of a significant increase in US import tariffs – a Trump election pledge, and a measure that appears to have bipartisan support.

Tariffs tend to be inflationary in the short term (during the first year after implementation), but ultimately deflationary.

Increasing the tariff rates on existing imports and raising the share of imports on which tariffs would be levied would reduce US economic growth as the negative effect via lower consumption and investment would overwhelm the financial benefits generated from higher tariffs. This negative impact on growth would be due to higher inflation.

Currently, about 25% of global (ex-China) imports to the US are subject to an average tariff rate of 4%. In addition, 60% of Chinese imports are subject to an average rate of 17%.

Full implementation would mean 100% of imports – from all countries except China – would be subject to a blanket rate of 10%; while imports from China would be subject to a 60% tariff.

Such a worst-case scenario could boost global inflation in the short term and stymie medium-term global growth. More open economies would be hit harder by the new tariffs.

For example, Asia’s small open economies could feel more heat: they mainly import capital goods from the US. These are difficult to source from elsewhere.

Europe would be hit by a 10% blanket tariff hike through its export exposure to both the US and China. Germany and Italy are more exposed than France and Spain on both these fronts.

Germany has a higher export exposure to China than other eurozone countries have, meaning it could suffer more if the tariffs were to weaken China’s economy.

An overview of scenarios

Tariffs can be seen as negative supply shocks, just like higher oil prices.

If a global tariff war breaks out and intensifies, it may push up the US dollar’s value yet further, hampering US exports. Other countries might react by devaluing their currencies to fight the damage tariffs do to their exports.

All else being equal, this could prompt the Fed to cut US interest rates quickly and/or deeply to counteract the deflationary pressures from a strong dollar. This would be positive for bonds.

Conversely, any short-term rise in inflation caused by tariffs may prompt the Fed to delay further interest rate cuts. Indeed, markets have scaled back their expectations of rate cuts since the election.

If the Fed looks beyond the transitory inflationary shock, it could resume cutting rates as long as inflation expectations remain anchored, and GDP growth slows. In this case, stocks and bonds would suffer an initial shock as the economy slows, but they should recover when the rate-cut cycle resumes.

Finally, if the resultant inflation turns out to be stickier than expected, the economy could fall into stagflation. That would pose a challenge for global markets’ macroeconomic policies and investment strategies.

| Scenario | Impact | Fed response | Market reaction |

| Global tariff war | Push up US dollar value, hamper US exports | Cut US interest rates quickly and/or deeply | Positive for bonds |

| Short-term rise in inflation due to tariffs | Interest rates are unchanged | Rate cuts on hold | Markets scale back rate-cut expectations |

| Transitory inflationary shock; GDP growth slows | Markets adjust rate-cut expectations | Resume cutting rates after inflation flare-up | Initial shock for stocks, bonds; recovery when rate-cut cycle resumes |

| Resultant inflation is stickier than expected | Economy falls into stagflation | Challenge for Fed policies | Challenge for investment strategies |