The International Monetary Fund has revised up its forecast for global economic growth in 2026 to 3.3% from the 3.1% it expected in October. The US and China – and artificial intelligence investment – are underpinning much of the improvement. The IMF expects a slight slowdown to 3.2% in 2027.

The IMF warned of potential risks from the concentration of technology investment in AI and related tech and the ongoing disruption to global trade.

Earlier, the World Bank had said the global economy was more resilient than expected despite persistent tensions over trade and policy uncertainty. It lifted its forecast for global GDP growth to 2.6% in 2026 and 2.7% in 2027, from the 2.4% and 2.6% respectively it predicted in June.

Around the world

The cost of ultra-long borrowing in Japan surpassed 4% last week, marking the highest yield on any Japanese sovereign debt in over three decades. The 40-year yields surged as traders sold bonds after Prime Minister Sanae Takaichi called a snap election for February, though yields later fell back.

Meanwhile, the Bank of Japan has kept interest rates on hold after news that December’s inflation rate fell to 2.1% from 2.9% in November.

Elsewhere, Eurozone annual inflation came in at 1.9% for December, down from the flash estimate of 2.0% and November’s 2.1%. US core PCE inflation for November – the Federal Reserve’s preferred inflation measure – was 2.8%, still above the Fed’s 2% target.

Figure in focus: 5%

China’s economy expanded by 5% in 2025, meeting the government’s official target, as a rise in exports helped offset sluggish domestic demand. Net exports accounted for almost a third of growth, marking their highest contribution since 1997 despite tensions over US tariffs.

Fourth-quarter growth slowed to 4.5% from 4.8% in Q3. China continues to suffer from a weak property market and subdued household consumption; its birth rate fell to a record low last year, underlining the long-term structural issues in the world’s second-largest economy.

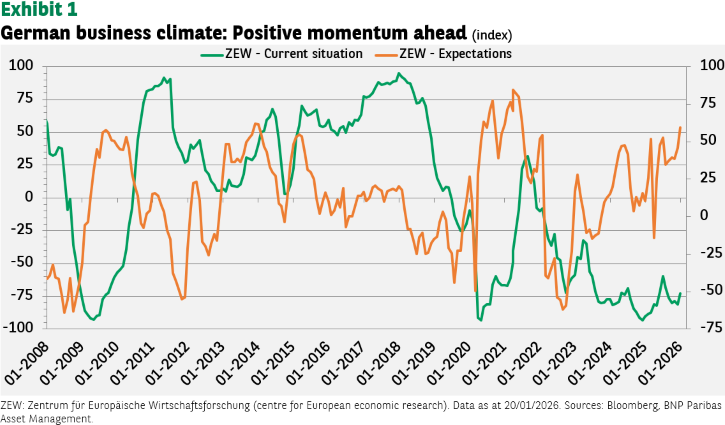

Chart of the week – German economic sentiment

The ZEW Indicator of Economic Sentiment – based on a survey of German financial analysts and investors – increased markedly in January, to its highest level since July 2021. This reflects hopes for ‘new momentum’, fuelled by Germany’s plans for massive infrastructure and defence spending. Order books are on the rise and industrial production at the end of 2025 was significantly higher than expected. Respondents’ assessment of the current economic situation improved, albeit modestly, but this is nevertheless encouraging.

Is it time to become more confident in Germany’s potential?

Words of wisdom – Creative destruction

A process where new technologies and innovations displace established economic structures, bringing short-term disruption, but ultimately shifting capital and labour towards greater productivity and growth.

A report from the World Economic Forum published during its recent annual meeting in Davos found that creative destruction today is powered “less by isolated breakthroughs and more by the combination, convergence and compounding of multiple technologies”.

The next wave of technological convergence is being driven partly by robotics moving from factories to human spaces, the WEF said.

What’s coming up?

- Germany’s closely watched Ifo Business Climate Index is issued on Monday.

- On Wednesday, the Bank of Canada and Fed hold their respective interest rate-setting meetings – the Fed is widely expected to keep rates on hold.

- Wednesday also sees the BoJ issue its latest monetary policy meeting minutes.

- On Friday, the Eurozone publishes a flash estimate for Q4 GDP growth along with the latest unemployment rate.