The world of finance in two minutes. This week:

The Middle East conflict has dampened global economic growth expectations and lifted inflation forecasts, according to the latest Organisation for Economic Co-operation and Development outlook. The organisation revised down its 2027 global growth forecast to 3.0% from 3.1% but left its 2026 forecast unchanged at 2.9%. Inflation in the G20 advanced economies is now projected to be 4.0% this year, 1.2 percentage points higher than previously expected. The OECD warned however that a prolonged disruption to the oil market “could lead to significantly worse outcomes”. Global markets continued to endure further volatility last week with the MSCI World NR Index falling 1.5% over the week to Thursday’s close*.

*In US dollar terms. Source: FactSet, data as of 26 March 2026

Around the world

In the wake of the challenging geopolitical backdrop, business activity slowed in several major economies in March, the latest Purchasing Managers’ Indices showed. In the US, the provisional reading for the S&P Global composite activity index fell to an 11-month low, to 51.4 down from 51.9 in February, but remained in positive territory as a reading above 50 indicates expansion. Businesses reported a slightly weaker upturn in new orders and higher prices following the outbreak of the Iran conflict. The composite Eurozone PMI fell to 50.5, from 51.9, a 10-month low. Meanwhile the UK flash PMI slowed to 51.0 from 53.7, a six-month low.

Figure in focus: 1.3%

Japan’s annual inflation slowed to 1.3% in February, its lowest rate since March 2022 and down from January’s 1.5%. The lower-than-expected headline rate was largely driven by stabilising food prices and renewed electricity and gas subsidies. Core inflation, which excludes fresh food, fell to 1.6% from 2% while the closely watched ‘core-core’ inflation measure, stripping out fresh food and energy, eased to 2.5% from 2.6%. Separately, Japan’s business activity slowed in March as its composite PMI decreased to 52.5 from 53.9 a month earlier.

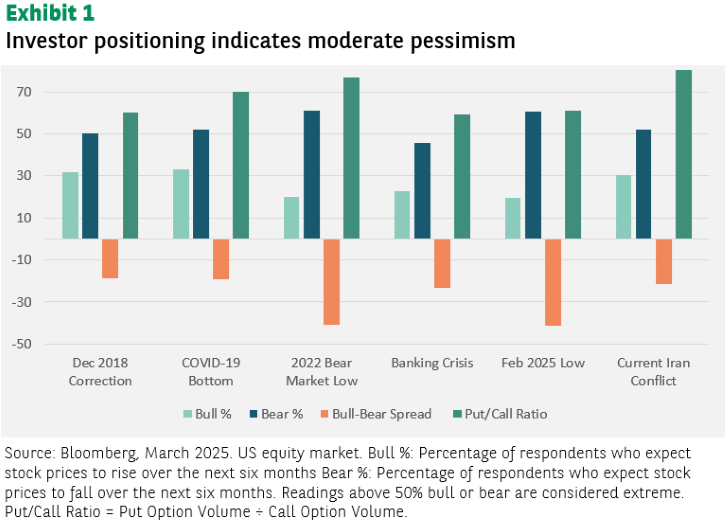

Chart of the week

Current investor positioning reveals a market caught between rebound expectations and caution. The relatively less pessimistic sentiment, along with elevated hedging activity, suggests investors are positioned protectively, in expectation for sentiment to gradually normalise. This cautious positioning could provide fuel for a market rally, based on possible catalysts for a de-escalation of the Middle East conflict, as heavily hedged markets often experience sharp gains when fear subsides, and protective positions are unwound. Short-term volatility could eventually give way to a rebound, as the market re-centres around the fundamental growth picture, which for now has not been altered.

Words of wisdom:

Zettajoule: A zettajoule is a unit of measurement used for extremely large amounts of energy. Where one joule describes the amount of energy transferred when one watt of power is used for one second, a zettajoule is equal to a billion trillion joules – a number with 21 zeros. The rate of ocean warming was around 11.0-12.2 zettajoules over the past two decades, more than twice the rate seen between 1960 and 2005, according to a new report by the World Meteorological Organization. Along with other indicators, this suggests that Earth’s climate is more out of balance than at any time in observed history, it said.

What’s coming up?

Monday sees the Bank of Japan issue its Summary of Opinions from its latest monetary policy meeting. On Tuesday a final estimate of UK fourth quarter GDP growth, and a flash estimate of Eurozone inflation for March, are published. The bloc issues its latest unemployment rate on Wednesday. On Friday, final PMIs are published for Japan, China and the US while the US also issues jobs data.