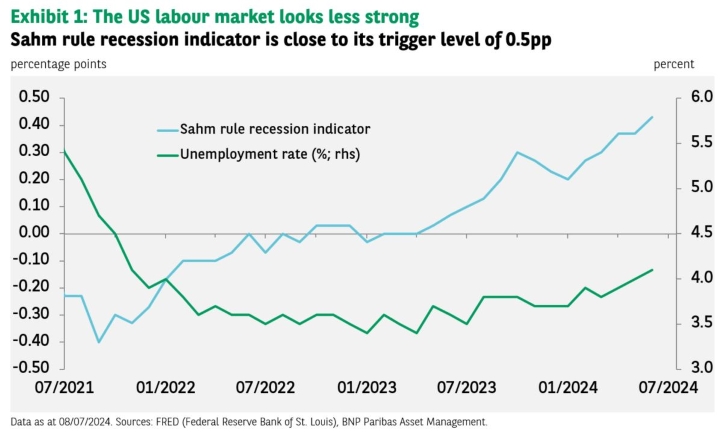

The US unemployment rate continues to rise: It stood at 4.1% in June – up from 4% in May, 3.9% in April and 3.8% in March – and is now at its highest since late 2021. At this level it is no longer far from a trigger point signalling an economic downturn.

This point is defined by the so-called Sahm rule, developed by former US Federal Reserve (Fed) economist Claudia Sahm. One way to summarise the rule is to say that when the unemployment rate’s three-month average is just half a percentage point above its 12-month low, the economy is in recession.

With the indicator at 0.43pp in June, we are close to this point.

The Sahm rule is based on the idea that, when people start losing jobs, they cut back on spending, and this causes more job losses.[1]

Research by the St Louis Fed has established this warning signal works (that may puzzle those economists who see the unemployment rate as a lagging indicator showing changes in economic activity after they have happened).

Investors don’t need to panic: Claudia Sahm herself, who is now a private economist, recently told CNBC that recession is not her base case. Nevertheless, the US labour market is beginning to send less encouraging signals, to say the least: nonfarm payrolls disappointed in the second quarter; jobless claims have now risen for two consecutive months.

What could this mean for the Federal Reserve’s interest rate policy?

The US central bank has a dual mandate: it is to foster both stable prices and maximum sustainable employment. On the latter, the minutes of the latest policy meeting show that “some participants observed that, with the risks to the… dual-mandate goals having now come into better balance, labour market conditions would need careful monitoring’.

The Sahm rule could certainly help in this monitoring exercise.

References:

[1] Source: https://www.washingtonpost.com/opinions/2024/07/09/economy-recession-risk-sahm-rule/