The 150 basis point (bp) increase in US Treasury yields since June 2020 has not yet posed a problem for equities, though there is always the worry that further rapid increases could prove too much for the stock market to bear.

One reason that equity markets have welcomed the increase is that higher US real yields reflect higher growth expectations, and the rise in inflation should be reflected in higher nominal company earnings.

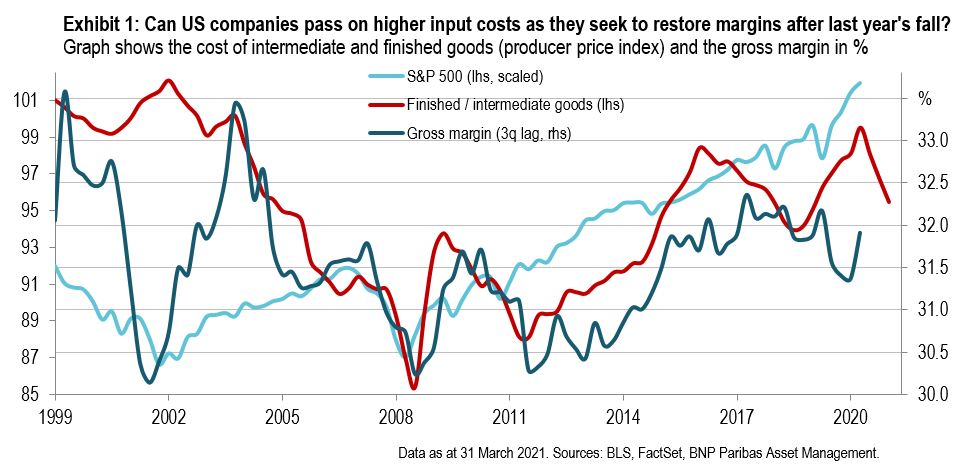

Do US companies have pricing power?

Whether inflation proves to be so benign will depend on whether companies are able to pass on higher input costs to consumers.

Intermediate goods costs have already been rising faster than the prices of finished goods, increasing the pressure on the margins of US companies further.

Owing to the pandemic, companies had already seen gross margins fall over the course of last year from 32.2% to 31.4% (see Exhibit 1).

We do not, however, see a significant risk on this front. As the US economy continues to reopen, consumers will likely be more tolerant of paying higher prices for activities that had until now been suspended. Competition will also be limited as not every business will be able to resume trading. In fact, some companies might use the resumption to restore margins to at least pre-pandemic levels.

For more insights, read our asset allocation monthly for April