Major economies have continued to recover from lock-down induced slumps in the first half of the year, although to varying degrees. In terms of what to expect, we should look to the countries where the virus arrived (China and (Asian) economies closely linked to it). They may indicate what we are likely to see in Europe and then in the US.

Staying the course or slowing down?

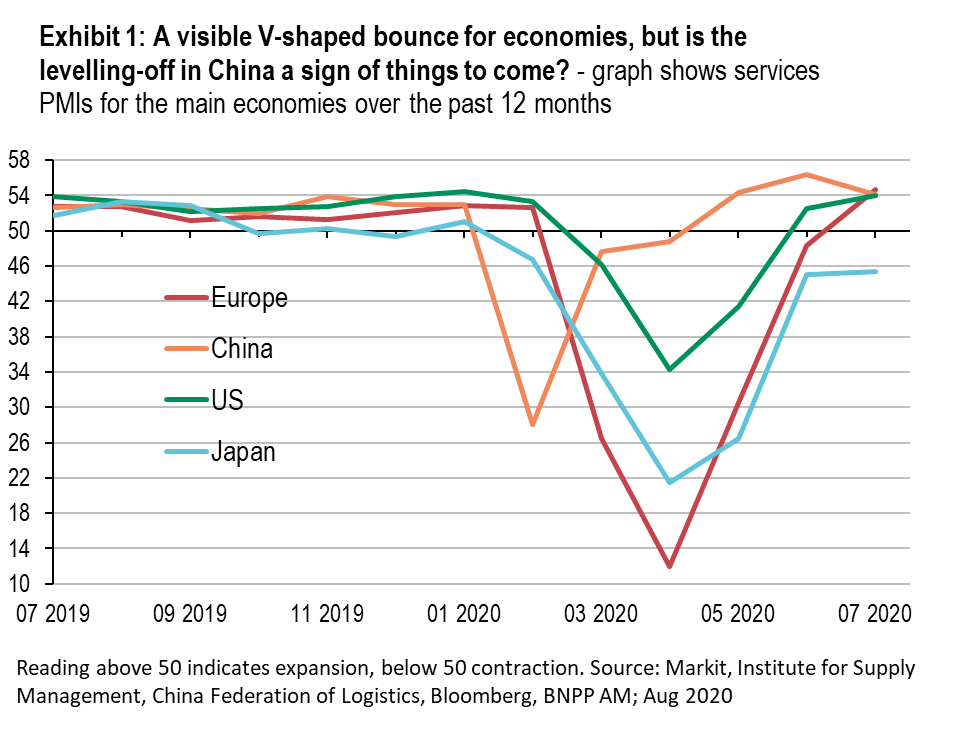

Can we assume that the bounce-back in China, first and foremost in business sentiment, but also in consumer demand, will be seen elsewhere? And are we looking at a V-shaped recovery with a relatively rapid return to pre-pandemic levels or will things slow down as we leave summer behind (and face a renewed rise in infections in the autumn and winter)?

Looking at the latest purchasing managers indices (PMIs), business sentiment surveys that foreshadow trends in the economy, momentum has slowed only in China. This is what you would expect given that the recovery has been going on for longer there. In Japan, the index has levelled off, while still below 50, indicating continued contraction. In the US and Europe, momentum still seems intact (see Exhibit 1).

Let’s look at services

We are focusing on the services sector. This sector was hit hardest by the lockdowns and has struggled to re-open as many restrictions remain in place and consumers are reluctant to return to pre-pandemic activities. It is also the largest sector in many economies.

The manufacturing sector, meanwhile, is often driven by internal and external demand and potentially less of a solid measure of the state of the domestic economy. It should be noted that manufacturing in China is often centrally guided and production levels more supply driven.

Guiding light from the east

Nevertheless, China can be used as a barometer since the recovery there is about two months ahead. The latest services PMI showed a pullback after the index set a high in June. This can be seen as an indication of caution creeping in about how quickly the economy can rebound, particularly in the face of new, local outbreaks which have led to the selective re-imposition of restrictions. As a general comment, it is difficult to see how the services sector can recover without a vaccine.

Worries over second waves will likely intensify after the summer. Geopolitical and social tensions will remain high at least until the US presidential election. The recovery from the COVID-19 lockdowns remains halting.

Consequently, a return to pre-pandemic levels of economic activity may be pushed further out. Talk of V-shaped recoveries and the associated market optimism might make way for fretting about whether central bank and government stimulus will need to be raised to prevent another dip in economic growth.