2024 was the hottest year on record according to the World Meteorological Organization, and the first calendar year in which the global average temperature exceeded the 1850–1900 average by 1.5°C – the limit set in the Paris agreement. And last year was no aberration – the past 10 years were the warmest on record. While the risks are clear, what about the way forward?

The effects of higher temperatures can be seen in severe weather-related events. In 2024 alone, extreme episodes included catastrophic flooding in Spain, a heatwave across west Africa that was exacerbated by climate change, and the worst drought on record in Brazil.

The risks are clear. Even though it might seem like it is too late, we believe all stakeholders should double down and take collective action to prevent the problems from getting much worse.

The 1.5°C target – An overview

At the multilateral COP21 climate talks in Paris in 2015, 196 countries agreed an international treaty to keep the increase in the average global surface temperature to well below 2°C above pre-industrial levels by the end of the 21st century, and preferably within 1.5°C.

The 1.5°C limit was chosen because scientists assessed that if temperatures rise by more than this amount, there would be profound consequences for nature, society and the economy.

While the 1.5°C threshold has already been breached, we note the Paris Agreement targets are for 2100, so we believe it is not too late to act to minimise further increases or even reduce global temperatures.

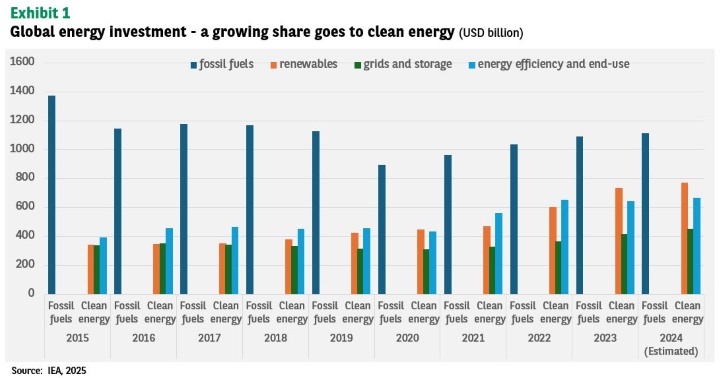

Progress is being made, but not enough

Many scientists around the world believe that rising temperatures are due to human actions, but there is growing scepticism among the general public about our role and the need to reduce carbon emissions. This is being reflected at the government level – most notably with the US withdrawing from the Paris Agreement for the second time in early 2025.

The good news is that progress is being made in the fight to limit the effects of climate change.

For example, the world is electrifying rapidly. According to the International Energy Agency (IEA), electricity use rose twice as fast as overall energy use between 2010 and 2023, and between 2023 and 2035 it is expected to grow six times as fast, partly due to greater uptake of electric vehicles and heat pumps [1].

The IEA points out that half of the world’s electricity will likely come from low-emission sources by 2030, helped by huge investments in clean energy. Global investment in clean energy has outstripped fossil fuel investment every year since 2016. Of the $3 trillion of investment in energy around the world in 2024, around $2 trillion will have gone into clean energy technologies and infrastructure.

Many companies have invested significantly in the energy transition and it seems unlikely that they will revert to their previous business models. A notable example is Danish energy company Ørsted*, which was once among the most coal-intensive companies in Europe. It has been able to adapt its strategy to become an almost pure renewable company. Meanwhile, major firms such as Amazon* have become the world’s largest corporate purchasers of renewables, and Google* has announced its interest in supporting the development of nuclear energy.

Investors are playing a part in financing the energy transition. According to Morningstar, global assets under management in climate funds have increased every year since 2018, although it looks likely that 2024 will be the first year of net outflows from these strategies (assets under management still rose because of market gains).

Government buy-in is vital, though. Unfortunately, some countries appear to be backpedalling on their commitments. Apart from the US, Denmark is a prominent example. After announcing in 2020 that it would award no more licenses to explore oil and gas reserves in the North Sea, it changed course by awarding new licenses less than two years later.

However, other countries are pressing forward – not least China, which invested an estimated $675 billion in clean energy technologies in 2024, well ahead of Europe ($370 billion) and the US ($315 billion).

While these figures look impressive, they are still well short of the level of investment needed if the world is to meet its urgent climate targets, including the goal of tripling renewables capacity by 2030, which was set out at COP28 in 2023.

What’s next?

The exit of the US from the Paris Agreement raises questions. Will other major countries backtrack on their climate commitments? Or will they step up and assume responsibility for driving the world’s transition towards a lower-carbon future?

China has been at the forefront of green technologies in recent years and has a huge role to play given the size of its economy, the scope it has to cut its own emissions, and its control of the supply chains for many of the minerals that are crucial for the energy transition.

We believe Brazil could be set to play an important role as the host of the next COP and a key member of the BRICS. It might be keen to play a bigger part in climate negotiations and act as a voice for developing nations.

Investors can also do more. For example, by increasing their allocations to companies involved in the energy transition. This is not solely about doing good. Climate change involves physical risks to the assets they hold. Transition risks linked to the move to a low-carbon economy impact asset returns. There are also wide-ranging opportunities as climate solutions providers have considerable scope to rise in value.

The 1.5°C threshold has been breached and we believe it is therefore vital that efforts to contain global warming increase. Climate change is a reality. All stakeholders need to sharpen their focus on adaptation by supporting, for example, the building of flood defences, the development of drought-resistant crops, and the relocation of communities at risk from higher sea levels.

With adaptation set to be one of the main focuses at the next COP, it is something we are going to hear a lot more about. Investors will have a significant role to play in this, too.

*References to specific securities are for illustrative purposes only and should not be considered as a recommendation to buy or sell, or investment advice. No investment decision should be made solely based on this information. BNP Paribas Asset Management may or may not hold positions in the companies mentioned.

[1] https://www.iea.org/spotlights/the-world-is-moving-at-speed-into-the-age-of-electricity