- The nearly $4 trillion green, social and sustainability (GSS) bond market offers investors the chance to capture the current opportunities offered by the global fixed income universe – with the added benefits of positive and transparent impact

- A flexible, unconstrained approach may be a new way to unlock the GSS market’s full potential, offering investors potentially higher risk-adjusted returns while broadening the scope of impact

- In a world of uncertainty and unpredictability, such an approach could be attractive for investors aiming to navigate periods of market volatility, mitigate downside, and create more resilient portfolios.

Why GSS bonds should not be overlooked

The green bond market may have reached maturity, with established issuance patterns and fewer surprises in store, but maturity does not mean a less attractive market for investors nor that its full investment potential has already been reached.

One should not ignore the considerable attributes we believe the GSS bond universe has to offer, as well as alternative investment approaches that could more effectively seize opportunities and build greater portfolio resilience.

Green bonds represent just 60% of the overall GSS market.1 When taken together with social and sustainability bonds, the combined market stands at close to $4 trillion in value, exceeding the euro investment-grade credit segment and offering access to more than 1,100 issuers spread across regions, sectors and currencies.2

The GSS segment has outperformed the global broad market by 3.4% on a cumulative basis since the end of 2022.3 This partly reflects the market’s larger proportion of credit and its higher sensitivity to European interest rates which could resonate with investors looking to diversify away from the US.

While it can be an attractive terrain to exploit, we believe an unconstrained non-benchmarked approach, with the freedom to invest across segments regardless of their index weighting, can bring out its value. Coupled with flexible and dynamic duration management, it could help mitigate against drawdown periods and navigate more volatile market environments.

This approach, well-known in the conventional bond market, surprisingly remains a rarity among GSS bond strategies. Yet it may offer what we see as a unique opportunity for investors to avoid having to choose between the aims of maximising return, limiting drawdowns and delivering positive impact.

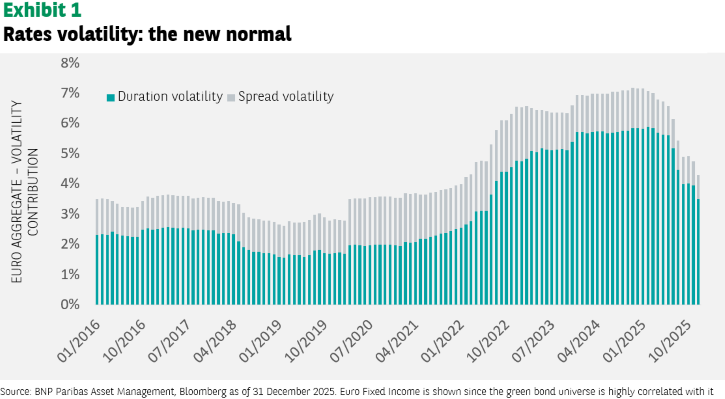

Agile duration management is key amid market volatility

The past few years have seen an historic increase in bond market volatility, predominantly stemming from interest rates. While this can pose a challenge for investors, we believe this could also create opportunities to seek returns.

Having significant leeway to calibrate duration can be critical in terms of not only aiming to protect the attractive yields the universe provides – limiting downside risk across cycles – while keeping the amplitude to capture the upside when rates rally.

Following an unconstrained approach can help unlock greater sources of alpha from yield curve positioning. With green bonds issued along the entire maturity spectrum, investors can look to move along the yield curve depending on their views on the monetary policy, growth and inflation prospects, as well as issuers’ fiscal profile and supply and demand dynamics.

In addition, global bond markets can often be closely correlated, yet also present idiosyncratic differences, so investors who follow an unconstrained approach have the potential to take greater advantage of cross-market opportunities to enhance returns.

Using the breadth of an unconstrained allocation

On a standalone basis, the green bond market offers a broad spectrum of segments to invest across – from investment-grade and high-yield to sovereigns and credit, as well as developed and emerging markets. An unconstrained approach allows investors to seek out the most attractive opportunities wherever they lay. Crucially, it also affords the possibility of significantly investing in underrepresented segments such as high-yield or emerging market debt.

Emerging markets continue to be an under-allocated segment, although their climate and social financing needs are often among the most acute. In the meantime, stepping out of the often-exclusive benchmark focus on investment-grade debt could enable investors to capture the carry opportunity of high-yield bonds.

Enhancing value through social and sustainability bonds

Decarbonisation is often at the forefront of investment strategies, yet social aspects should not be overlooked. Social inclusion is a key part of achieving a climate-resilient future, and in many parts of the world, social progress remains a key preoccupation.

We believe that social and sustainability bonds can offer interesting opportunities from an impact and investment perspective.

Sustainability bonds – whose proceeds can be invested in both green and social projects – is a fast-growing dynamic segment that saw record levels of issuance in 2025.4 They can offer access to a wider variety of sovereign and industrial issuers while being able to support similar themes as social bonds. The format has been particularly appealing to EM issuers as sustainability bonds now represent 36% of total emerging market debt in the GSS bond market.5

We believe a blended GSS bond allocation, with a dominant green bond tilt, can be a solution for investors who might not have scope for a dedicated social strategy alongside green bonds and for whom achieving net zero is a stated priority.

Ultimately, adopting a flexible, unconstrained approach to the GSS bond market has the potential to offer competitive returns, help investors navigate different market conditions and drive meaningful change.

[1] Source: BNP Paribas Asset Management, Bloomberg as at 27/02/2026 (green, social and sustainability bond market ex CNY, excl. outstanding <$300mio).

[2] Source: BNP Paribas Asset Management, Bloomberg as at 27/02/2026 (green, social and sustainability bond market ex CNY, excl. outstanding <$300mio).

[3] Source: BNP Paribas Asset Management, Bloomberg. Euro hedged cumulative performance of the ICE SSAG and GBMI indices from 31/12/2022 to 27/02/2026.

[4] What next for green bonds after a year of resilience? | Core Investments

[5] Source: BNP Paribas Asset Management, Bloomberg as at 27/02/2026 (Green, Social and Sustainability bond market ex CNY, excl. outstanding <$300mio).