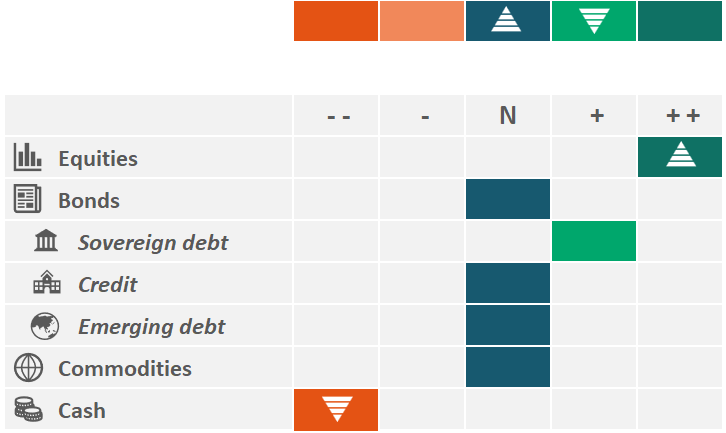

- Significantly overweight global equities. Following a period of neutrality ahead of the Iran ceasefire, we have since rebuilt our equity allocation, initially to a maximum overweight. When it became clear that both Iran and the US were willing to enter negotiations, it materially reduced tail risks

- Taking advantage of more attractive entry points. With the Iran conflict resolution still unfolding, we rebalanced our overweight exposure from the worst‑hit markets (emerging markets, Japan and Europe) to stronger near-term segments, notably US technology

- Long EU duration, neutral on US Treasuries. We maintain a long position in euro five‑year yields, expecting the ECB to show some restraints despite earlier hawkish signals. The Federal Reserve is also likely to stay in a wait-and-see mode, with labour market data not yet weak enough to fully offset inflation risks and tighter financial conditions.

By Clément Dupire, Senior Multi-Asset Portfolio Manager, BNP Paribas Asset Management

From a financial market perspective, the Iran war closely resembles previous geopolitical shocks: a sharp but short‑lived sell‑off followed by a rapid and near‑complete recovery in risk asset prices.

The equity rally which followed the ceasefire announcement was frantic, initially driven by one‑way flows from discretionary investors and subsequently reinforced by systematic strategies.

As cross‑asset volatility declined, these strategies mechanically rebuilt their equity exposure, helping propel equity markets back toward new highs.

Our initial positioning was geared towards a scenario in which the assets and regions most impacted, alongside the US market, would recover.

Moving beyond this perceived normalisation led by lower volatility, improved sentiment and increased investor risk appetite, we have subsequently reverted to more pertinent fundamental considerations and information gleaned from our quantitative investment signals. We have therefore taken some profits on our equity allocation but remain significantly overweight.

In practice, market behaviour delivered two clear signals.

- First, investors demonstrated a willingness to re‑engage with long‑term structural winners, particularly in US technology and semiconductors, once valuations had reset to more reasonable levels.

- Second, the market is implicitly waiting for a more pronounced decline in oil prices to confirm the transitory nature of the energy shock.

As long as a definitive peace agreement with Iran has not been formally agreed, oil prices will continue to embed a residual risk premium. This elevated energy cost acts as a temporary drag on import-heavy economies in Europe and Asia.

Our multi-asset views

Earnings season kicks off

The US earnings season got off to a strong start. At the time of writing, 83% of S&P 500 companies have beaten earnings-per-share estimates, putting the US on track for expected year‑on‑year earnings growth of more than 13%.1

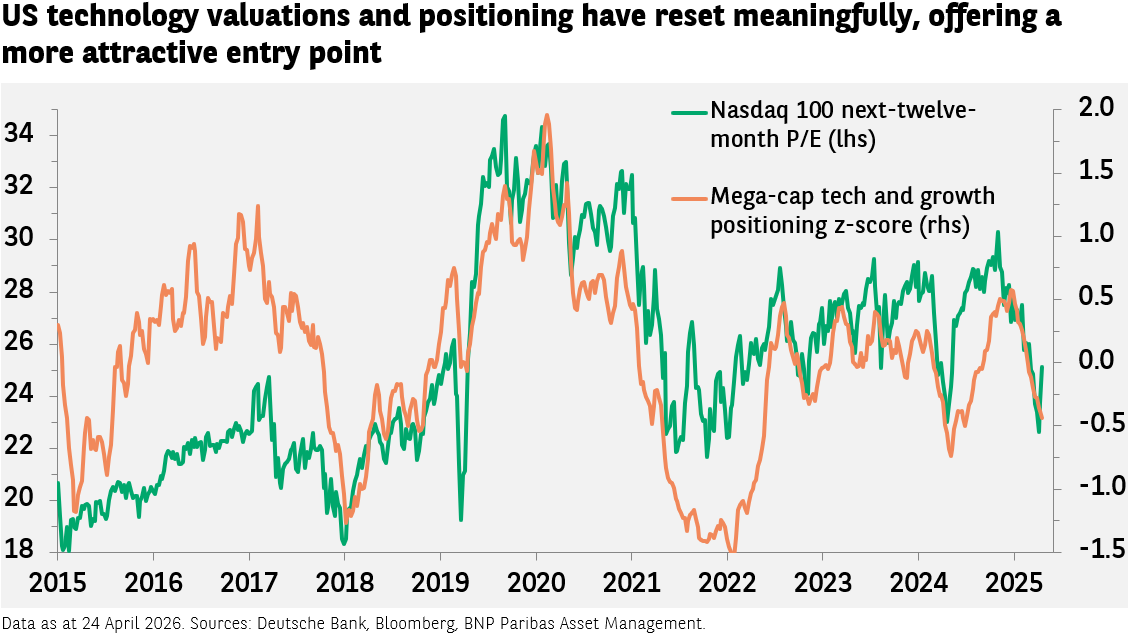

As price-to-earnings multiples have been whipped around by geopolitical fears, broadly improving earnings have driven the market’s resilience. This is especially true for the US technology sector, where valuation and positioning sent strong ‘buy’ signals (see Exhibit 1).

The Philadelphia Stock Exchange Semiconductor Index (SOX) has surged 47% in just 18 sessions following the Iran ceasefire – its longest winning streak on record – reflecting surging artificial intelligence‑driven demand and sharply rising earnings expectations for semiconductors.

Although semiconductors rallied robustly, even the challenged software segment has started to recover from the drawdown triggered by peak AI‑disruption concerns. We see a path between more bearish scenarios and an uneven disruption implied by agentic AI models, making sector‑level discrimination increasingly important.

Inflation concerns persist

We expect oil and gas prices to gradually subside, leading us to position for a pricing normalisation in energy sector equities. In Europe, we increased our exposure to banks, where investor positioning had become materially reduced compared to January’s levels.

On rates, we maintain a long duration position on euro five‑year German bonds. Markets are rightly concerned about the persistence of inflation stemming from commodity prices, but we believe expectations of European Central Bank tightening this year are excessive. Fragile eurozone growth significantly constrains the policy room for the Frankfurt institution.

By maintaining this exposure, we aim to capture potential upside from a rate normalisation that proves less aggressive than the two-plus hikes currently priced before year-end 2026. We see the situation as fundamentally different than in 2022.

The energy crisis at the time was the result of a (permanent) supply shock due to Russia’s invasion of Ukraine and a demand shock coming out of the pandemic. In addition, Russia’s natural gas supply made up 30% of the gas consumed in Europe, while the share of oil and gas directly imported from the Middle East before the Iran war started was more marginal.

We are maintaining a neutral stance on credit. We remain alert to recurring concerns surrounding private credit and shadow banking, where concerns around liquidity continue to resurface periodically in the financial media, but often only focus on redemptions and ignore the positive inflows. In this context, we prioritise the upside potential offered by equities whilst continuing to harvest the income from existing investments in credit markets.

[1] Source: Morgan Stanley