Gold has shone on the financial markets in 2024. Is investing in gold still relevant after such a rally? Is it time to diversify your exposure to precious metals? What is its potential for appreciation for 2025?

Gold in 2024

Over the past 12 months (through November), the price of an ounce of gold on international markets has increased from around USD 1 900 to over USD 2 650 for a gain of almost 40%.

There are several major factors driving gold prices higher:

- Fears of inflation have led investors to use gold as a hedge against the risk of currency devaluation. In 2024, central banks bought 694 tonnes of gold, according to data from the World Gold Council, diversifying their holdings away from the US dollar.

- President-elect Trump’s purported policies are seen as likely to weaken emerging market currencies, leading some central banks to spend US dollar reserves to defend their currencies from capital outflows and prevent excessive weakening.

- Geopolitical tensions in Ukraine and the Middle East have reinforced gold’s role as a safe-haven asset.

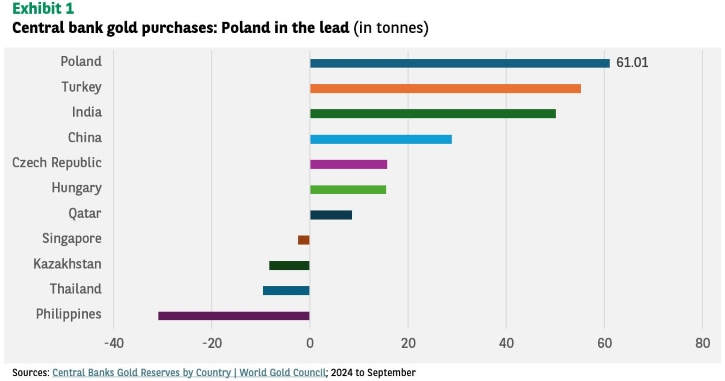

- Central banks, particularly those in emerging markets, have maintained their pace of gold purchases – initiated in February 2022 – to diversify their reserves. While China’s purchases slowed in the second quarter, India accelerated its buying to become the third largest buyer between January-September 2024. More surprisingly, the National Bank of Poland (NBP) has led central bank buying since early 2024 with 61 tonnes purchased. With now 420 tonnes of gold reserves, Poland has doubled its allocation in three years. It now holds more gold than Portugal, the United Kingdom, or Spain. Governor Adam Glapinski aims to increase gold’s share of the NBP’s reserves to reach a level of 20%.

- Central bank purchases seem be motivated not just by an objective of gradually diversifying reserve holdings away from US dollar dominance despite the US’s ‘economic exceptionalism’. There is also interest in exploring alternatives to the US dollar-based payments system that has been at the core of the international financial system for around 80 years.

Donald Trump’s decisive victory in the US presidential election reset market expectations as investors assessed the potential impact of his likely policies. Markets now price in fewer US interest rate cuts and have pushed the US dollar higher in foreign exchange markets on the assumption that potential tax cuts and higher import tariffs would boost inflation.

As an asset with no yield, gold tends to benefit from lower interest rates (higher interest rates raise the opportunity cost of holding such an asset). A strong US dollar – the currency in which gold is priced – also typically weighs on the precious metal’s price.

And what about silver?

The price of silver has also risen this year, but in a strikingly similar proportion to that of gold.

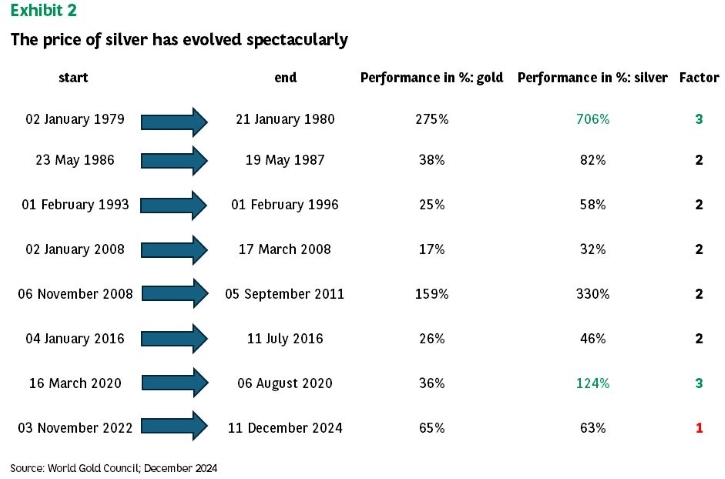

From an historical perspective, the price of silver has evolved spectacularly, amplifying by a factor of two on average the variations of gold prices depending on the periods and contexts (see Exhibit 2).

The reasons are related to the market for silver being smaller and less liquid than that for gold. Silver also has a dual role (as a precious metal and an industrial metal). Its market volatility is higher: in 2011, silver jumped by 416% to its peak compared to 163% for gold.

Silver’s faster and more marked increase preceded a sharp correction linked in particular to the slowdown in industrial demand. More recently, the market has gone from a long-term structural surplus to a deficit. The reason is essentially the steady growth in industrial demand related to the manufacture of photovoltaic panels, electric vehicles and 5G networks.

In addition, silver is mined mainly as a by-product of the extraction of gold, copper or zinc. As the production of these has increased little or not at all, the quantity of silver put into circulation (excluding recycling) has also not increased.

Catalysts could now accelerate the ‘catch-up’ of silver on gold. India, for example, is on track to double its silver imports compared to 2023. Silver plays an essential role in the generation of solar energy and is therefore strategically important in terms of national energy security.

Generally optimistic sentiment on precious metals is beginning to arouse interest in silver from speculative investors attracted by

- a valuation that is more attractive than that of gold

- an asset that cannot be depreciated by the monetary authorities.

Conclusion

The factors that supported the price of gold in 2023 and 2024 remain in place. In fact, they even seem to be strengthening given the pace of purchases from central banks. Gold should continue to rise. Silver now appears to offer an opportunity for diversification with a strong potential to follow gold higher.

While gold has reached new highs in 2024, silver is still down 40% from its peak in 2011. Investing in silver in 2025 would be risky due to its higher volatility, but the potential for appreciation is at least twice that of gold. To be continued in 2025.