These are the core investment decisions from this month’s report on our multi-asset investment views.

Staying overweight on global equities

2026 began with unsettling actions ranging from the US arrest of Venezuelan President Nicolás Maduro and threats against Iran to the criminal probe into Federal Reserve Chair Jerome Powell and tensions within NATO over Greenland’s sovereignty. We view these as largely short-term distractions. The economic reality is what matters for markets, and the backdrop still appears to be a ‘Goldilocks’ scenario. In the US, inflation has been cooling, the labour market has been stabilising, and GDP growth has accelerated. Our machine-learning-powered indicators are signalling we are firmly in bull market territory. With a supportive earnings season underway, we remain constructive on risk assets.

Long risk, but more diversified

We entered 2026 with a marked preference for Europe validated by its outperformance. We now expect this to fade and have reduced our position. We have broadened our allocation with an increased exposure to emerging markets and added Japan. We expect Japan’s Prime Minister Sanae Takaichi to secure a mandate for fiscal expansion in February’s lower house elections, reinforcing the expansionary policy backdrop. Tactically, we re-engaged with the tech-heavy Nasdaq at month-end, expecting ‘Big Tech’ earnings to reassure markets after the segment’s relative underperformance at the end of 2025.

Neutral duration, watching Japan

Our focus has shifted in the near term to the potential impact of a further steepening of the Japanese yield curve. The market is pricing in a consolidated majority for the ruling Liberal Democratic Party and consequently a relaxation of fiscal prudence. With longer-dated Japanese government bond yields pricing higher, we are mindful of a de-anchoring from other developed market curves as Japanese investors can now find attractive yields at home and reduce their appetite for foreign bonds. The spillover was masked by ructions in markets during the World Economic Forum’s meeting in Davos, but US yields are getting closer to levels associated with the ‘danger zone’ for risk assets, even without a repricing for the remaining two US rate cuts expected this year.

Looking through the noise

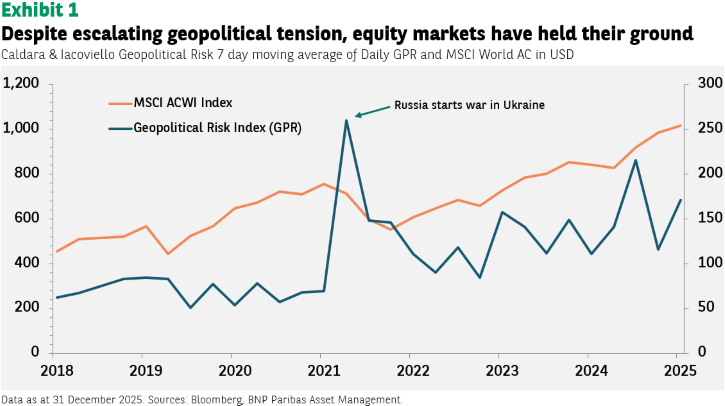

Recent geopolitical developments have proven unpredictable and unsettling, but we have chosen to look through the ‘noise’. From a financial standpoint, markets have remained largely unfazed. Events in Venezuela and Iran briefly lifted oil prices, but crude oil remains burdened by a significant supply-demand imbalance.

Some geopolitical shocks can alter economic fundamentals in a lasting way, but many do not (see Exhibit 1). Only global flashpoints that fundamentally reshape key cost structures or supply chains can move the pricing landscape durably. Recent headlines do not meet that threshold.

The unpredictability and sensationalism that characterise today’s policy environment tends to saturate the media landscape, carrying the risk that long-term investors could lose sight of underlying fundamentals.

What matters for us right now is clear: real US GDP growth in the fourth quarter of 2025 has likely accelerated to above 5% annualised, disinflation has remained largely on track, and the technological revolution of artificial intelligence has been advancing steadily.

We are witnessing a healthy broadening of market participation, extending to both within and outside of the US, and crucially, beyond the technology sector. In the US, this is marked by a solid performance in high-beta, lower-quality segments. Simultaneously, valuations of the tech giants have retreated in relative terms, reflecting market anxiety over a potential capital expenditure hangover.

Furthermore, we believe this broadening still has room to run. The monetary easing provided by the Fed’s three recent ‘insurance’ cuts, combined with the fiscal impulse from President Donald Trump’s ‘Big, Beautiful Bill’, is fuelling a cyclical recovery in earnings for small caps and sectors outside the technology sphere. Also, the US administration’s focus on affordability — ahead of November’s mid-term elections — should continue to provide a floor for consumer‑oriented sectors.

Technology backdrop remains strong

Despite the broadening, we have added exposure back into mega-cap technology stocks. Flow analysis suggests the conditions are increasingly favourable for a reversal as positioning among discretionary investors in both technology and cyclical firms has converged toward neutral.

In our view, current discretionary positioning does not adequately reflect the path of expected earnings. The fundamental backdrop for ‘Big Tech’ remains strong, and the upcoming earnings releases may be the catalyst needed to re-energise investor interest and restore momentum to the sector.

Outside the US, we have shifted a portion of our risk allocation toward emerging markets to increase our sensitivity to Asia and the region’s tech‑oriented companies as we head into the earnings season.

The Eurozone has delivered a strong performance since last summer, and with expectations now running high, we see value in locking in profits and further broadening exposure. We remain exposed to the Eurozone banking sector specifically where we continue to see solid fundamentals that we believe can justify further upside from a re‑rating.

Key risks to monitor

On fixed income, our focus remains on the potential for higher rates after developments in Japan,but also the outlook for Fed policy given the strong US macroeconomic background.

The repricing of Japanese government bonds matters far beyond Tokyo as seen at times in 2025. Japanese yields are still at the lower end of the developed market spectrum, and as a result, the adjustment has the potential to translate into reduced overseas demand and spill over into higher US and European rates. That move has been visible in recent weeks and is a key risk to monitor.

One implication is that the broadening we have seen in equities may face a more challenging environment should global rates rise.

Several of this year’s market-leading pockets – rate‑sensitive segments, speculative growth, and smaller capitalisations – typically benefit from falling discount rates and easier financial conditions. Our framework suggests the ‘danger zone’ for US duration begins at yields of around 4.40% on the 10‑year Treasury, roughly 20bp above current levels.

A continued steepening of the yield curve – whether driven by the Japanese government bond curve, firmer inflation or renewed political pressure on the Fed’s independence – could push yields on long-dated bonds starting with the 30‑year towards or above 5%.

Such a move would likely weigh more broadly on asset prices and provoke consolidation across risk assets. We are also monitoring credit spreads as an early indication of any waning risk appetite given the currently tight spread levels and their positive correlation to market expectations for future monetary policy.

In the current scenario, gold remains one of the most effective hedges in a multi‑asset portfolio. We favour exposure, either directly or via gold miners. The latter offer leverage to spot gold prices, while benefiting from improving fundamentals. With the US dollar trending weaker, and messaging from Washington unclear, we see a case for maintaining exposure to this diversification, where possible, within our global allocation.

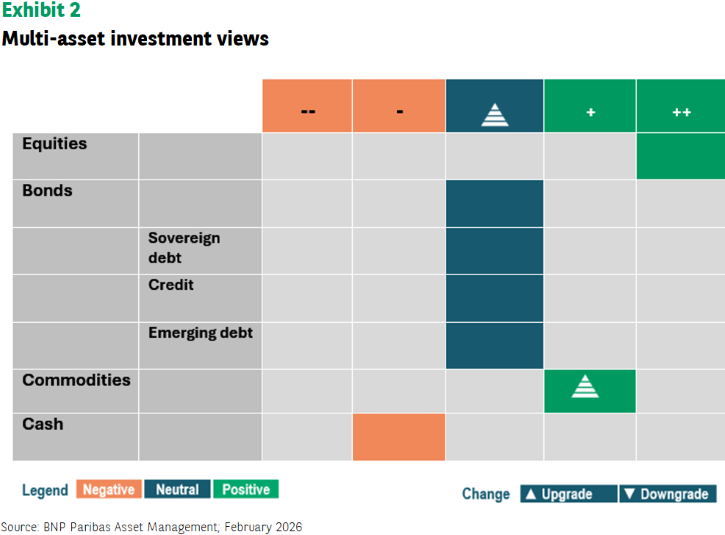

Asset class views