Elida Rhenals, Co-Head of Inflation, Senior Portfolio Manager

- The Middle East conflict has led investors to consider the risks of stagflation

- Bond yields have risen sharply with investors pricing in tighter monetary policy as central banks will need to tackle higher inflation

- Short-duration inflation-linked bonds offer potential protection from rising inflation and swings in interest rates

Global bond markets suffered in March as inflation fears created by the Middle East conflict led to a major rise in interest rates.

The upward move was triggered by surging energy prices in the wake of the war, which has all but halted oil and gas flows from the Middle East.

The backdrop has fuelled inflation worries. Should the war drag on, time will play against the global economy and price stability, with a rising risk of stagflation — increasing inflation mixed with stagnant growth.

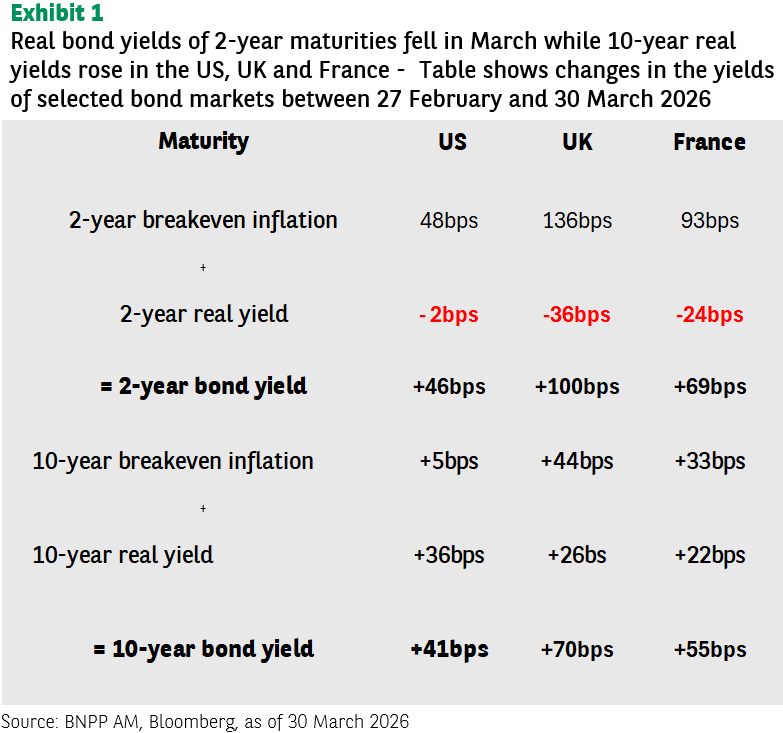

A combination of low growth and high inflation is a rare and unpleasant experience in developed economies, since a weak economy normally means tepid demand and a fragile labour market, dragging down price rises. Markets now expect central banks to raise rather than lower interest rates in 2026. As a result, short-term debt bore the brunt of March’s sell-off, as investors abruptly shifted from anticipating central banks interest rate cuts to hikes to counter higher inflation. Exhibit 1 shows the changes in selected bond yields in the US, eurozone and UK in March.

But inflation-linked bonds offer potential protection

Higher Inflation tends to weigh on conventional bonds, whose fixed nominal yields are not correlated to rising prices. While investors continue to receive the stated coupon, their real value is eroded as inflation picks up, compressing real returns.

Inflation-linked bonds in contrast enable investors to stay ahead of inflation because the cash flows paid out are adjusted to reflect the rise in prices. Inflation-linked bonds benefit from daily indexation to total inflation, including the food and energy components.

Principal and coupons grow over time thanks to this daily indexation process. As time passes, the principal increases at the same rate as the corresponding inflation rate.

The inflation indexation works gradually over time, meaning that in highly volatile environments, like those markets are currently experiencing, inflation linked bonds returns are mainly driven by movements in real interest rates.

But by focusing on short-dated inflation linked bonds (i.e. one-to-five year maturities) an investor can limit the impact of changes in real interest rates on returns and focus on the benefits of inflation indexation.

If you came for breakevens, stay for realised inflation

Short-dated inflation-linked bonds’ performance in March demonstrates their capacity to protect investors from an inflation shock. Inflation breakevens delivered +1.15% of performance and absolute performance of short-dated inflation linked bonds is +0.05% (month-to-date as of 30 March). This compares with the performance of -1.10% for short-dated nominal bonds (performance data is USD hedged).

We remain constructive on the outlook for short-dated inflation-linked bonds. In our view, inflation breakevens are currently perfectly pricing higher energy prices in the short term and therefore higher inflation for the rest of the year.

This means that for breakevens to rally further, we need to experience a further sustained increase in energy prices from current levels or any other shock on inflation (tariffs, supply chain disruptions, higher wages, etc.)

Such a shock could result from an unfavourable scenario, with persistence of very severe constraints on traffic through the Strait of Hormuz, keeping hydrocarbon – oil and gas -prices at very high levels – e.g. an average of $100 per barrel in 2026, before falling back (to around $80) in 2027.

This scenario would imply persistent strains on European gas supplies, particularly during the pre-winter stock-building period; prices would reach around €70 per megawatt hour on average in 2026 and €61 per MWh in 2027. In addition, we could also consider second round effects from the strains in Hormuz coming from higher fertilizer prices (leading to higher food inflation) and the lower supply of byproducts of gas production like helium.

With what we see as a fair pricing of inflation expectations, we believe that the main source of performance for short-dated inflation-linked bonds increasingly relies on realised inflation: The recent energy shock and the consequent uplift in prices will translate into higher income coming from inflation indexation.

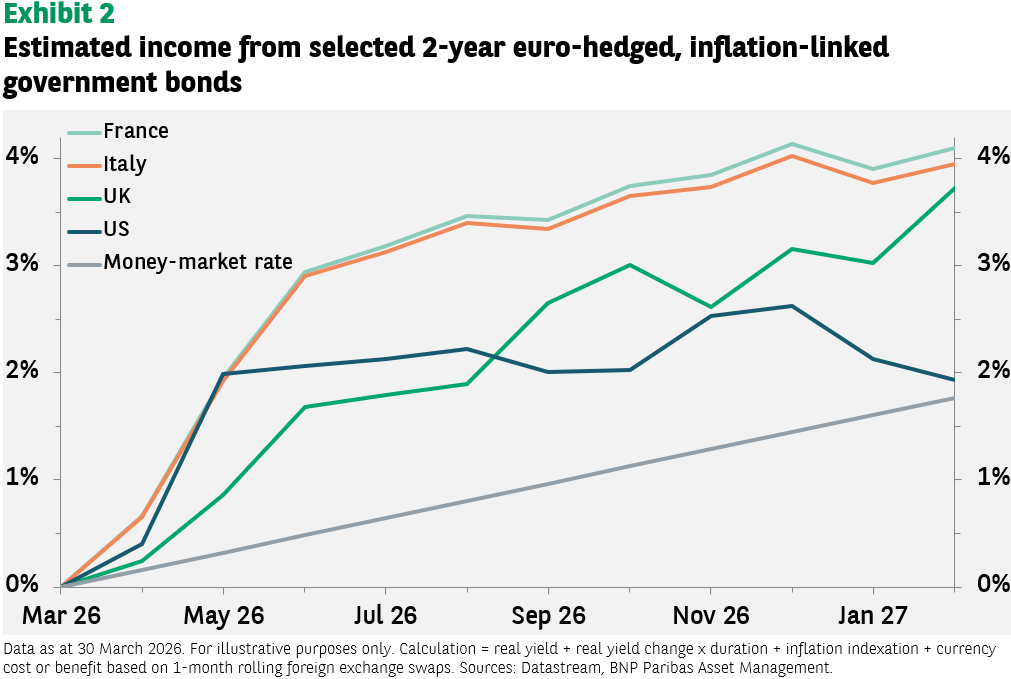

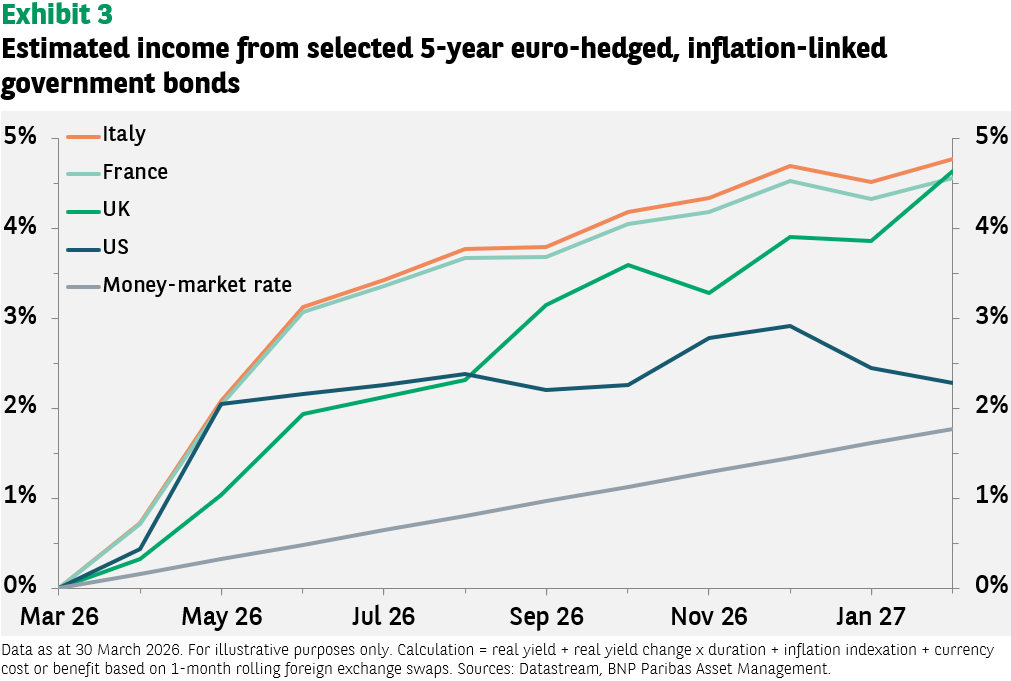

As seen in the chart below, under current market conditions, we estimate the income from short-dated inflation-linked bonds will be between 3% and 3.5% between April and year-end, driven primarily by the inflation indexation mechanism:

We believe the amount of inflation indexation in the future months will be high enough to provide protection against a material sell-off in real rates, as occurred in 2022, a period with some similarities to today’s environment: an inflationary shock and fears that central banks would be forced to tighten monetary policy.

Moving towards stagflation

The tension in the Middle East constitutes a major supply shock, pushing inflation risks higher just as growth momentum across advanced economies was starting to deteriorate. Activity indicators were already pointing to weakening demand and softer labour markets. As a result, the macroeconomic backdrop increasingly resembles a stagflationary mix of slowing growth and persistent inflation pressures.

In this context, we favour short-dated inflation-linked bonds, particularly in the eurozone. This segment has proved to provide efficient protection against higher realised inflation while limiting exposure to interest rate swings. At the same, we believe they will benefit from potential repricing of overly hawkish policy expectations, becoming the most efficient hedge against a stagflationary macroeconomic mix.