Curve steepening combined with compressed equity and credit risk premia could pose a challenge for insurers, requiring skilful management of duration and risk.

This article is part of our 2026 Investment Outlook.

Political concerns together with expected increases in sovereign bond issuance could lead to higher long-term rates, which would be positive for some insurers, but could also drive market volatility.

Insurers may need to further diversify and manage their risk exposure more actively, requiring agility; though constrained, insurers do have room for manoeuvre.

We live in a fast-changing world where organisations need to adapt to thrive – and this is especially true for insurance companies. Insurers are impacted by economic cycles and fundamentals, but unlike many other sectors, they must also navigate financial market risks and developments in regulatory frameworks. In the current fluid environment, agility and risk management are key.

Looking back over the past five years from the pandemic to the present day, it has been a bumpy road for insurers. After a decade of ultra-low interest rates, post-pandemic-driven supply-side disruption, followed by the Russia-Ukraine conflict, led to an unprecedent spike in inflation, monetary policy tightening and a surge in interest rates and interest rate volatility.

However, the typical adverse consequences of more restrictive financing conditions did not materialise, with the US particularly showing surprising resilience. The influence of much tighter monetary policy has been offset by stronger-than-anticipated consumption and investment as well as a significant fiscal expansion.

This period offered a mix of challenges and opportunities for insurers. Interest rate volatility is complex to manage, but all in all, yields at multi-year highs and resilient risk assets have allowed insurers to rebuild book yields – that is, bond yields locked in at purchase time – and to strengthen their balance sheets.

Easing back

Inflation and monetary conditions have been progressively easing, although at different rates, across different economies. Gloomier macroeconomic conditions in Europe and a faster convergence toward its target inflation rate pushed the European Central Bank to start normalising its policy rate as early as mid-2024, reaching 2% in mid-2025. The Organisation for Economic Co-operation and Development (OECD) expects Eurozone GDP growth of 1.2% in 2025 and 1.0% in 2026.1

However, the situation in the US is different, with the fed funds rate at 3.75%. Market expectations are for US rates to fall to 3.0% in 2026, reflecting both the expected softening of the labour market and GDP growth, and above-target inflation. Notably, market expectations are still subject to uncertainty over the economic impact of President Donald Trump’s trade tariffs and overall policy. The OECD is forecasting US GDP growth to fall from 2.8% in 2024 to 1.8% in 2025 and 1.5% in 2026.2

A global easing cycle, with downward rate adjustments along the curve, can pose a challenge for insurers. Such an environment calls for sound management of duration and reinvestment risks, especially for those insurers whose liabilities are not properly matched – but this time it seems to be different.

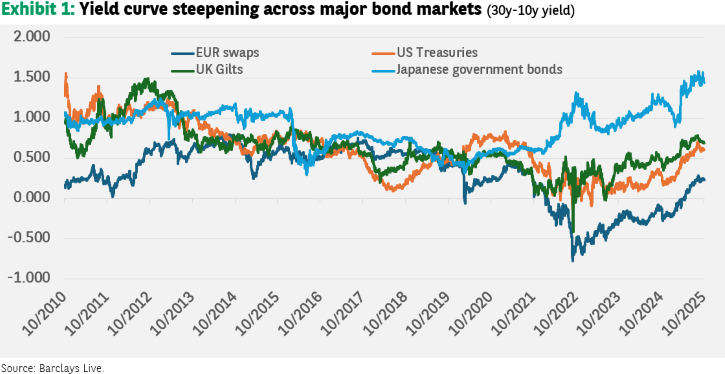

Curve steepening, compressed credit and equity risk premia

Despite a softer growth and inflation outlook, interest rate curves have steepened in most major markets, reflecting political uncertainty and the resurgence of concerns over fiscal expansion, fiscal deficits and debt sustainability. The US and French situations are symptomatic, as illustrated by recent credit rating downgrades.

Political instability combined with expected increases in net issuance might reinforce a shift in sovereign risk premia. Other technical factors could exacerbate curve steepening such as the Dutch pension system reform, which is expected to drive a significant reduction in long duration positions held by pension funds, potentially leading to further increases in long-term rates and volatility.

On paper, steeper interest rate curves benefit insurers, especially those running long-term liabilities as they can capture higher yields and generate higher investment earnings. But it is not always that straightforward.

Moving into long-duration bonds too quickly can leave insurers with significant unrealised losses and reduce their ability to manage and rotate portfolios. Insurers who are long receiver swaps – that is, receiving a fixed interest rate and paying a floating interest rate – could see their liquidity needs increase and their stock of eligible collateral diminish.

For life insurers with long-dated liabilities and a negative duration gap, higher long-term rates can boost balance sheets. This positive effect is expected to be even stronger with the implementation of the Solvency II reform in 20273 (higher sensitivity beyond the Last Liquid Point4).

On the other hand, widening swap spreads are not completely captured by the volatility adjustment (VA) – a counter-cyclical measure that reduces the impact of changes in credit spreads on insurance liability valuations under the standard formula – and the actual portfolio can diverge from the regulator’s benchmark.

While sovereigns are under pressure, risk premia on risk assets are compressed despite the political uncertainty, concerns over trade wars and tariffs, a softening growth outlook and rising geopolitical risks.

High all-in yields across the credit spectrum have supported strong demand for credit over the last few years. So far, credit fundamentals have been resilient, monetary conditions are easing, and corporate bond issuance is running at elevated levels, but given the valuations and risks on the radar, the sector remains vulnerable to shocks.

The same applies to equity markets, at least in the US. Optimism around the potential benefits of artificial intelligence (AI) have led to massive amounts of capital being deployed across a handful of companies that made the bulk of total returns over the recent period. Earnings will have to be proportionate to the general enthusiasm around the AI boom to not trigger any correction.

Room to manage change and uncertainty

Recent history shows insurers need to be ready and equipped to manage changes and uncertainty. That may sound obvious, but against this uncertain backdrop, the golden rule remains to properly diversify risk exposures. This also applies to liability duration-matching portfolios; in many European countries, over half the government bonds held by insurers are issued by their own government.5

Insurers can now find more opportunities to diversify via bonds from European institutions or supranational organisations. They can also aim to mitigate swap spread risk by combining high-grade bonds and interest rate derivatives.6 Derivatives can offer value and flexibility, but require a sound collateral management framework.

The Solvency II reform should incentivise insurers to better diversify their portfolios to better align with the VA benchmark that is estimated to be more diversified than most actual portfolios.7 The formula specifies that bonds, loans and securitisations can be considered to calculate the VA, not derivatives, which should also inform the use of interest rate swaps.

The home bias found within risky assets and corporate bond investments in particular is generally lower than for high-quality fixed income assets, but the potential for enhanced diversification remains significant. Diversifying into foreign credit markets and across economic areas can substantially reduce concentration risk and offers more relative value opportunities.

Diversifying away from the domestic market requires hedging against unwanted risks. Here, again, interest rates and currency derivatives are useful. They can give insurers more flexibility and allow them to adjust the spread risk exposure to market conditions as credit portfolios can be more agnostic about the liability profile.

There are degrees of possible diversification in a fixed income portfolio, the ultimate step being to implement a global multi-sector approach and exploit the entire risk spectrum across developed, emerging, public and private markets.

For instance, for a similar level of rating, certain asset-backed securities can exhibit a significant risk-adjusted spread pickup compared to corporate bonds. Of course, insurers should consider the return on capital requirements, and in this regard, the lower capital charge proposed in the Solvency II reform for securitised products will likely reduce the breakeven.

Consider enhanced risk diversification

With multiple risk factors on the radar, insurers must be agile and consider enhanced risk diversification in their portfolios. As usual, the complexity lies in combining a more active and sophisticated investment management approach with regulatory and accounting constraints.

Insurers that run portfolios valued using the Variable Fee Approach model under the new International Financial Reporting Standards (IFRS) 17 standards should find this new accounting framework provides more flexibility to manage the risk return profile of portfolios more actively.8

However, more broadly, we believe there is room for manoeuvre across all portfolios whatever the applicable regulatory framework, meaning insurers have scope to adapt, and thrive.

[1] OECD Economic Outlook, Interim Report September 2025 | OECD

[2] OECD Economic Outlook, Interim Report September 2025 | OECD

[3] European Commission proposals for Solvency II reform published in July 2025

[4] Updated technical RFR documentation applicable as of 30 June 2025 – EIOPA (Last Liquid Point – LLP – re-Solvency II refers to a change in risk-free rates calculations

[5] FINANCIAL STABILITY REPORT, EIOPA June 2025

[6] Derivatives are investments whose value depends on the changes in an underlying asset or security. The stock is not physically held but there is a contract based on several predictions in time or price in the future.