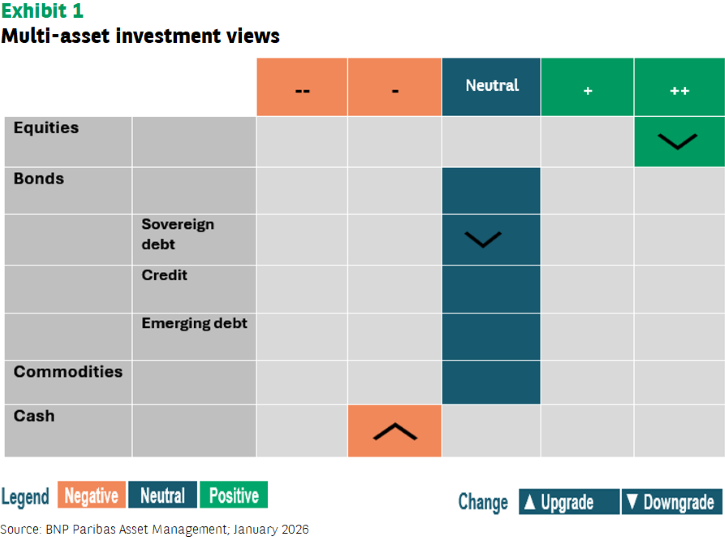

These are the core investment decisions from this month’s report on our multi-asset investment views.

We opted to reflect increased uncertainty by marginally reducing the overweight stance of our equity allocation

The widely-anticipated year-end rally was late, but welcome. Over the November-December period, equity markets struggled to regain momentum. A pick-up in volatility pricing, albeit from muted levels, weighed on sentiment.

Markets focused primarily on communication around the US Federal Reserve’s December meeting. Despite delivering the expected fed funds rate cut, this exposed a growing lack of consensus on the path of future policy.

We maintained our allocation to the Eurozone and its financial sector. We also retained our emerging market exposure via broad China equity indices

Much ink has been spilled over the short to medium-term impact the boom in capital spending on artificial intelligence (AI) will have on company earnings, GDP and productivity growth. While we do not believe that from a valuation perspective equity indices are in a bubble, the fourth quarter of 2025 witnessed a noticeable cooling of investor appetite towards the AI theme and high momentum trades in the US. We reduced our exposure to technology stocks by cutting some exposure to the Nasdaq and China tech indices.

We closed our position in short-dated German government bonds and adopted a neutral exposure in terms of interest rate sensitivity

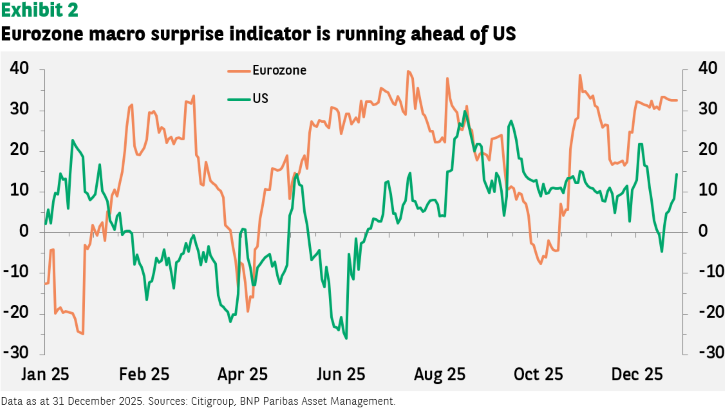

While we remain convinced that the ECB’s increasingly hawkish stance is somewhat over-zealous – given the persistent weakness in European exports, the strength of the euro, softer energy prices and the ongoing risk of imported deflation from China – we acknowledge the move in market pricing and the persistence of positive macroeconomic surprises.

Trimming our strong allocation to equities

The Federal Reserve (Fed) delivered its third consecutive interest rate cut in December – despite the absence of much public macroeconomic data due to the US government shutdown, and questions hanging over the quality of some of the data which was subsequently published.

There was volatility surrounding monetary policy going into 2026 (with two policymakers voting for no policy change). The Fed board consensus under Chair Jerome Powell has begun to break down. This has had a mildly negative impact on investor confidence, but President Donald Trump’s appointment of the next Fed Chair will likely materially shift the focus to further policy accommodation.

Beyond that, recent macro numbers have been supportive of further easing without raising concerns over a more marked deterioration either in the labour market or inflation. The Fed faces a bifurcated economy whereby lower income households and small businesses require policy help, yet the rest of the economy is doing well, as aggregate GDP growth and corporate earnings continue to show.

For the Eurozone, markets have begun to price the possibility of a European Central Bank rate increase in 2026, largely due to concerns that the German fiscal boost, along with lagged spending for the NextGenerationEU programme (especially in Italy), will raise the neutral rate for the Eurozone as a whole.

We have marginally reduced our strong allocation to equity markets. Our quantitative signals play a foundational role in the construction of our investment views and their translation into our portfolio construction. In general, we have seen a weakening of the intensity of the positive signals that had accompanied our decision to increase risk in our equity allocation. While the intensity has clearly abated, it is only to a neutral level rather than a negative one.

The small rise in uncertainty in the US monetary policy outlook following the Fed’s December meeting was a negative factor, along with small moves in market volatility pricing. Adding some optionality into the start of the year, by receding marginally from near-maximum levels of risk appetite for our portfolios, indicates some prudence rather than any fundamental concerns. We remain significantly overweight equities.

We have maintained a keen focus on the evolution of investor sentiment and positioning indicators to appreciate the potential for new investor flows into or out of asset classes, but especially in equity markets. A common theme has been the weak support from discretionary investors since the extreme moves in April and May. While falling levels of volatility have driven systematic investors – those who use data-led quantitative models to make decisions – to re-engage with risk, discretionary investors appear to have been reluctant to engage above neutral on an aggregate basis.

More recently, retail investors proved less aggressive in countering market weakness to increase their positions. We are encouraged that the recent brief spikes in volatility have reduced systematic positions from elevated levels, while discretionary investors will likely be forced to chase the market from historically prudent levels of equity risk exposure. This means that, bar a new shock, we see space for investors to add to their equity positioning.

Neutral on corporate bonds

We remain neutral (structurally invested) on credit as we prefer to concentrate our positive risk assessment in equity markets. Flows into investment-grade bonds were again strong in 2025 despite concerns over the increasing demand for financing from technology companies to build AI infrastructure with borrowing rather than from cash reserves.

High-yield has generally lagged these flows from investors as spreads have hovered around historically tight levels. While investment-grade investors have shunned government bond markets in favour of tapping marginally higher yields in credit for their duration needs, it appears high-yield investors have likely looked for better risk-reward from equity markets in their allocations.

The combination of further policy accommodation from the Fed (and other central banks), the lagged impact of ECB easing, fiscal stimulus in the US, Eurozone, Japan and perhaps China, plus resilient corporate earnings and the rising probability of a ceasefire in Ukraine all underpin a favourable setting for the start of 2026.