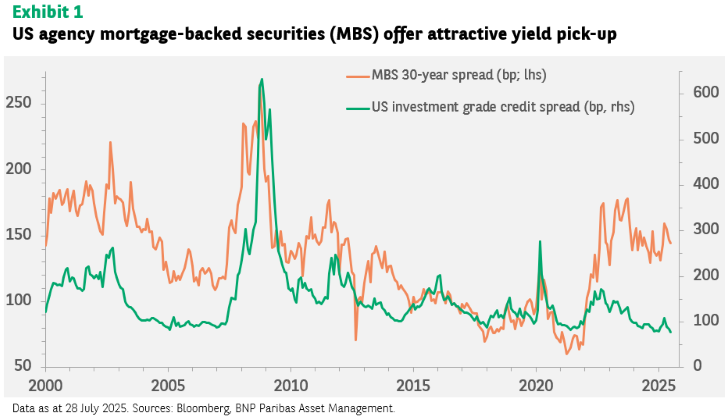

At a time when spreads on US investment-grade corporate bonds are at record lows, US agency mortgage-backed securities (MBS) offer better credit quality plus a pickup in yield. What’s more, these securities offer investors potential return streams that are uncorrelated with other fixed income segments.

The primary risk with US agency MBS is not credit risk (they benefit from the implicit backing of the US Treasury), but volatility via prepayment risk.

US agency MBS is a large component of the global bond universe: it makes up about 12% of the fixed income market globally and about 23% of the US bond market (source: Bloomberg, June 2025). That size means market liquidity is deep.