A ‘perfect storm’ of concerns over investments in artificial intelligence (AI), the US economy possibly slipping into recession, and an unwinding of yen carry trades triggered the global market sell-off on ‘Black Monday’, 5 August. The surge in intraday volatility suggested this was driven more by technical considerations than fundamental worries.

Listen to the article

In our view, a US recession is unlikely. We expect risk appetite to recover further, with investors buying risk assets more selectively.

Wrong recession signal?

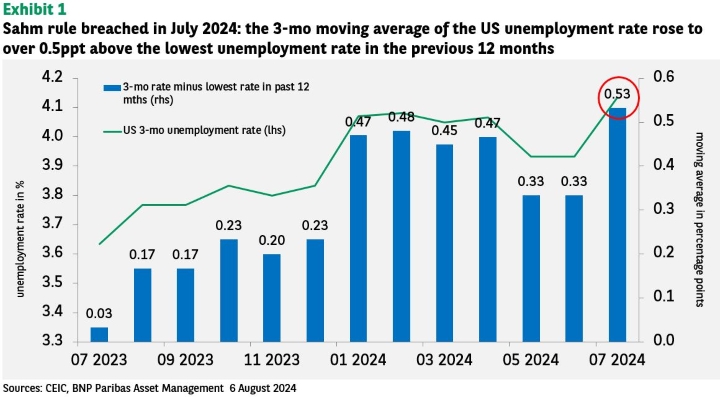

The US non-farm payroll report published on 2 August showed a slowing in the pace of hiring in July. The parallel rise in the unemployment rate caused the so-called Sahm rule, watched by many economists, to be breached and set off market concerns over an imminent recession. This abruptly replaced hopes for a soft landing and unleashed a market sell-off.

The rule says recession is imminent when the three-month moving average of the jobless rate rises more than 0.5 percentage points above its lowest rate in the previous 12 months. That threshold was crossed when July’s 4.3% unemployment rate pushed up the three-month average to 0.53ppt above the lowest unemployment rate in the past year (see Exhibit 1).

Simultaneously, the market euphoria over AI investments faded as many players began to doubt the monetisation timelines for these often massive outlays.

To cap it all, a fierce unwinding of the yen carry trade aggravated the market sell-off. The strategy of borrowing cheap yen and swapping it into higher-yielding currencies and assets soured when the Bank of Japan (BoJ) raised key rates on 31 July and announced the implementation of quantitative tightening. The yen strengthened in response.

The prospect of yen funds now being repatriated to Japan will likely weigh on global risk asset prices. That would include US tech stocks where part of the carry trade flows went.

What do the fundamentals say?

The Sahm rule may not be relevant this time because it does not reflect what is happening in the US labour market. The unemployment rate was driven up by a rising supply of labour (due to increasing labour participation and immigration in 2022 and 2023) rather than falling demand (as would be the case in an imminent recession).

Even Claudia Sahm, the former Fed economist who created the rule, has said she doubts the US economy is in contraction. She has pointed to continued growth in household income, consumer spending and business investment.

The Chair of the US Federal Reserve (Fed), Jerome Powell, has weighed in, referring to the Sahm rule as a statistical regularity, not a tool for assessing economic reality.

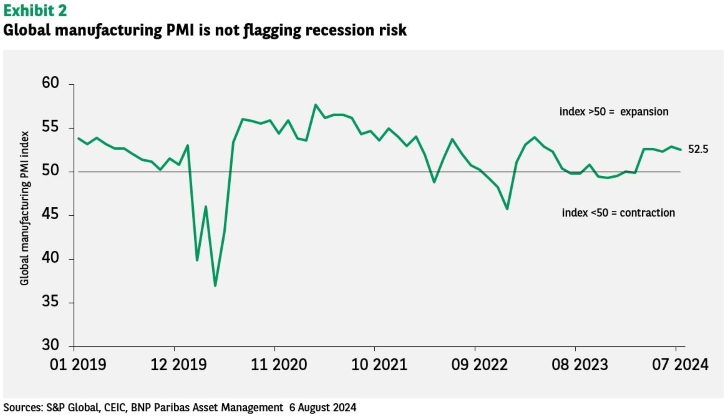

Although the recovery in the global manufacturing purchasing managers’ index appears to have peaked (see Exhibit 2), it is not flagging a forthcoming recession. The PMI has hovered above the 50 boom-bust line since early this year, with July’s index at 52.5 after 52.9 in June.

Even China, a major component in the global PMI, has recently ramped up support to counter the weaknesses in its consumer and property sectors. At the Politburo meeting in late July, Beijing unveiled a 20-point push to boost consumption and an action plan to promote urbanisation. These initiatives are expected to help income and consumption growth and to stabilise the property sector.

With more central banks moving to a more aggressive pace of monetary easing, there should be tailwinds, not headwinds, for global growth. Economic fundamentals are still broadly supportive of (slow) growth and do not point to a recession.

What next?

Given the sharp moves in financial markets, the changes in monetary policy have been priced in quickly. However, the narrative around rate cuts by the US Fed has not changed. The overriding question is whether the Fed will start its easing cycle in September with a 25bp or a 50bp cut.

Indeed, inflation in the US has remained benign. That should give the Fed room to deliver rate cuts as needed. While core personal consumption expenditures (PCE) inflation is still 60bp above the Fed’s 2% target, the three-month annualised rate has dropped to 2.3%, with improving labour cost and housing price growth dynamics.

The main risk is the possibility of a self-reinforcing market sell-off plunging the US (and global) economy into a recession via negative wealth effects and tightening financial conditions. If this were to happen, the Fed could cut rates swiftly and aggressively.

The spillover effects could drag Japan into a recession as falling US demand and a drop in the USD-JPY exchange rate would hit demand hard, reducing inflation. Under such circumstances, the BoJ would likely have to suspend its policy normalisation efforts.

Volatility likely to last

With the probability of a ‘Goldilocks’ scenario having declined sharply after the recent steep sell-off, US employment data will likely be key to the Fed’s policy outlook – and to equity market volatility. Exacerbating it are geopolitical risk and uncertainty over the outcome of the US election.

This backdrop implies that we may see a rotation into defensives out of cyclicals in the near term. The recent shift into, and strong performance of, small caps will likely only be sustained if the US economy manages a soft landing.

Investors’ current anxiety about a recession means that small caps may suffer in the near term. And, given that fear of recession is still circulating, equity market volatility is likely to rise relative to bond market volatility.