The world of finance in two minutes. This week:

The International Monetary Fund revised down its 2026 global economic growth forecast to 3.1%, from the 3.3% it predicted in January. While the IMF said the Middle East war is threatening to throw growth “off course”, it left its 2027 projection unchanged at 3.2%, but warned that a prolonged conflict could slow economic expansion to around 2% this year. However, the IMF added that growth could increase if artificial intelligence-driven productivity gains materialise faster. Elsewhere, global stocks rose on hopes of an end to the Iran war with the S&P 500 breaking through the 7,000 mark for the first time while the Nasdaq and Japan’s Nikkei 225 also reached fresh highs.

Around the world

Eurozone inflation rose to 2.6% in March, up from 1.9% in February and above the preliminary estimate of 2.5%. The increase largely reflected a surge in energy prices on the back of the Iran conflict. Inflation now stands at its highest level since July 2024, and above the European Central Bank’s 2% target for the first time this year. Core inflation, excluding energy, food, alcohol and tobacco, eased to 2.3% in March, from 2.4% in February. Eurozone inflation is expected to average 2.6% through 2026, according to the ECB’s latest forecast.

Figure in focus: 5%

China’s economy grew by 5% in the first quarter of 2026, beating analyst estimates of 4.8%, and up from 4.5% in the previous quarter. Stronger exports and manufacturing helped drive growth, offsetting sluggish domestic consumption and falling property investment. China recently lowered its annual growth target to a range of 4.5% to 5%, from a previous target of ‘around 5%’, its lowest goal since 1991. Separately, China’s trade surplus reached its lowest level in over a year in March as export growth slowed to 2.5%. Meanwhile, China’s imports surged by 27.8%, marking their strongest growth in more than four years.

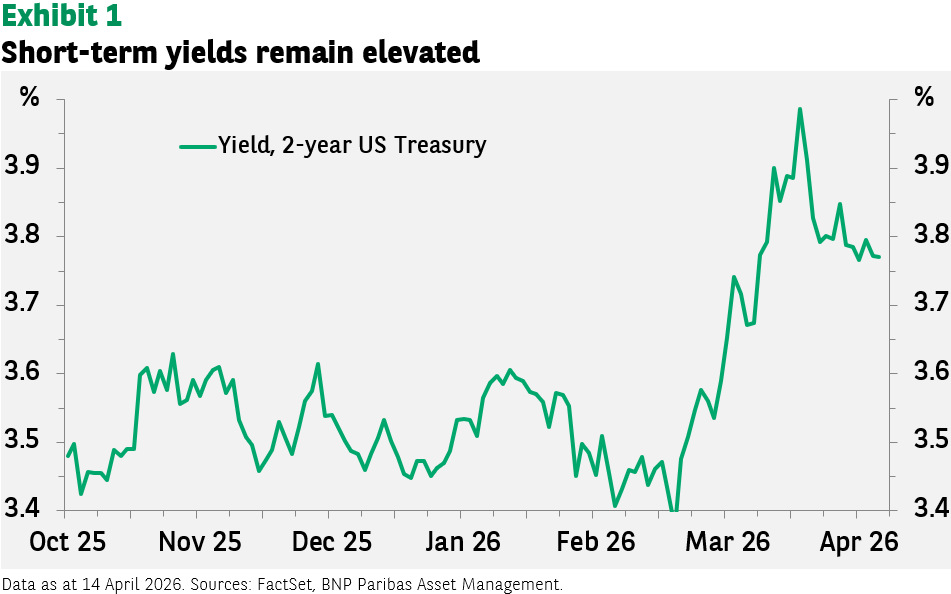

Chart of the week

Equity markets have recovered strongly since a two-week ceasefire in the Middle East was announced. Short-dated bond yields have, however, remained high – two-year US Treasury yields are still close to 3.80%. Short-term bond yields are driven by expectations of future central bank interest rate policy. Higher energy prices and the inflation shock have put an end to hopes of looser US monetary policy in 2026. Financial conditions are tightening, which makes things tougher for US consumers and corporates.

Words of wisdom:

Super El Niño: An unusually strong climate pattern that could cause extreme weather events and push global temperatures to record levels next year. El Niño is the warming phase of sea temperatures in the tropical Pacific Ocean – a naturally occurring climate pattern, whose counterpart is La Niña, the cooling phase. Where a standard El Niño phase is defined by sea surface temperatures rising by at least 0.5°C above the long-term average, a ‘super El Niño’ phase is marked by a rise of at least 2°C – which according to reports has only occurred a few times since 1950.

What’s coming up?

Canada updates markets with its latest inflation data on Monday. On Tuesday the Eurozone’s ZEW Economic Sentiment Index is published while the UK reports unemployment figures and follows with inflation data on Wednesday. Thursday sees several flash Purchasing Managers’ Indices published, including those covering the US, Eurozone, UK and Japan. On Friday, Japan releases inflation data while Germany issues its closely watched Ifo Business Climate index.