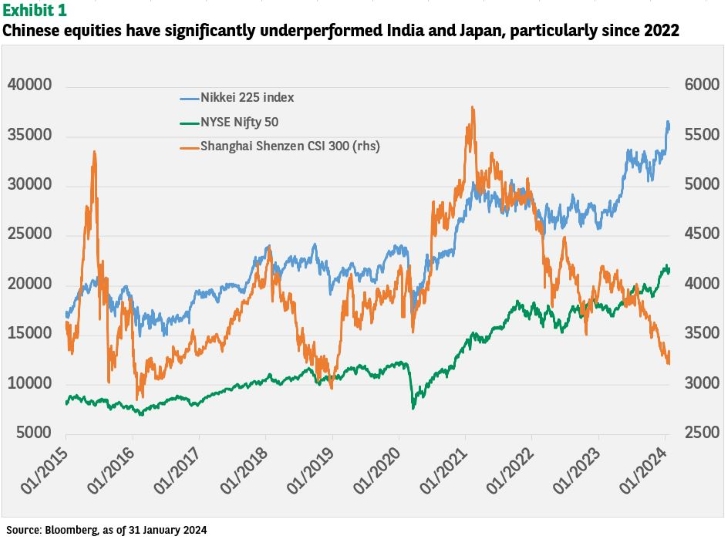

China’s stock market has been one of the worst performing in the world, with the Shanghai Shenzhen CSI 300 dropping by around 20% since August 2023 (see Exhibit 1). This fall is partly due to steadily deteriorating expectations of China’s growth — aggravated by underwhelming macroeconomic and fiscal stimulus.

In recent weeks, China’s authorities have announced measures to bolster stock markets. This follows a dismal start to the year for Chinese stocks with Tokyo overtaking Shanghai as Asia’s biggest equity market, while India’s valuation premium over China has hit a record.

Confidence in China’s economy remains depressed despite the recent efforts by China’s government to add stimulus. Measures undertaken include facilitating access to long-term cash for banks, tightening rules on the lending of shares for short selling and broadening developer access to loans.

Nothing so far has led to a meaningful turnaround in either economic activity or in the ongoing stock market selloff that’s wiped out some USD 6 trillion in value. The onshore benchmark CSI 300 Index has recently slid as much as 1.3%, on track to wipe out all gains in the last week of January spurred by hopes of stronger government support. A gauge of China stocks listed in Hong Kong lost as much as 1.8%. The offshore yuan was little changed, while China’s 10-year government bond yield dropped to 2.43%, at the lowest level since 2002. The Australian dollar — which is risk-sensitive and seen as a proxy for China — declined 0.5%.

Here are the factors our Multi Asset investment team are taking into account in assessing the outlook for Chinese stocks:

- Earnings: On some measures, China looks to be the weakest of global equity markets. The net upgrade ratio and the percentage change in consensus earnings-per-share forecasts are both poor. From a cyclical perspective earnings may be depressed but there is little evidence of mean reversion.

- Monetary policy: At the margin policy is certainly easing, but at the moment, we do not see it as sufficiently material to offset the drag from the real estate crisis.

- Valuations: This remains the central part of a bullish thesis with traditional equity multiples at historically low levels. However, a low multiple does not necessarily equate to value as long as profitability trends remain unattractive.

- Sentiment: Investor sentiment is depressed. Admittedly, this could act as a contrarian support for Chinese equities.

- Price trends in Chinese stock indices: The pattern of lower lows and lower highs continues, and the slope of various moving averages remains negative.

On this basis, our Multi Asset team have little appetite to take advantage of the recent sell off in Chinese equities given the opaque nature of the policy reaction function. There could be short-term opportunities on the basis that some of the fall in markets in the last two weeks was based on forced selling and unwinding of structured products. There have been three rallies exceeding 10% in the last 12 months despite the firm downward trend.

Disclaimer