On 4 March, Friedrich Merz, Germany’s chancellor-in-waiting, proposed a constitutional amendment that would pave the way for an extensive programme to boost defence spending and overhaul German infrastructure. By employing, in English, the phrase “whatever-it-takes”, Merz made sure there was no doubt about the scale of his intentions.

“In view of the threats to our freedom and peace on our continent, ‘whatever it takes’ must now also apply to our defence,” said CDU chairman Merz.

The ‘debt brake’, enshrined in Germany’s constitution since 2009, has been a guarantee of the country’s fiscal rectitude. The proposal to now bypass the rule reflects the acceptance by Germany policymakers of the need to ensure Germany’s own defence – whatever the cost.

The magnitude of the proposed measures took financial markets by surprise. Yields of German government bonds (Bunds) have risen sharply in reaction to an unexpected, abrupt and significant change in German policy that could fundamentally change the economic outlook for both Germany and Europe.

What are the proposed measures?

Chancellor-to-be Merz has agreed a deal with his party’s likely coalition partner to inject hundreds of billions of euros in extra funding into Germany’s military and infrastructure. It represents a paradigm change and does away with Germany’s previous fiscal straitjacket.

The new measures are intended to revive the economy and re-arm the country in reaction to recent declarations from the new US administration. To obtain political buy-in for the plan, Merz has agreed to also propose a major increase in spending on improving Germany’s infrastructure

Just a week after winning the federal elections, Merz explained that his Christian Democratic Union (CDU), its Bavarian sister party (CSU) and the rival, centre-left, Social Democrats (SPD) will jointly present a bill in parliament in the week of 10 March to reform the constitution and relax the strict borrowing rules. The bill foresees the following measures:

- A provision to exempt defence spending above 1% of GDP from the ‘debt brake’ that caps government borrowing. This would allow Germany to raise a potentially unlimited amount of debt to fund its armed forces and to provide military assistance to Ukraine

- A second constitutional amendment to set up a €500 billion fund for infrastructure, which would run over 10 years. The federal states would receive €100 billion from this fund

- A loosening of debt rules for the 16 German federal states allowing them to take out debt to the tune of 0.35% of their economic output. This was previously only possible for the federal government.

What happens next?

The intended timeline is for the first reading of the legislation to take place on 13 March. Then it will go to the committee stage prior to a vote in the federal parliament (Bundestag) on 17 March before the federal council (Bundesrat) reviews and votes on the legislation on 21 March.

The proposed legislation necessitates a change to the constitution. This will require a two-thirds majority in both the Bundestag and Bundesrat. Currently, the CDU/CSU and SPD together hold 403 of the 733 seats in parliament. A two-thirds majority requires 489 seats. Obtaining a majority would thus require at least 86 votes from either the Greens (who hold 117 votes) and/or the FDP (who have 90 seats).

In the Bundesrat, it will also require a two-thirds majority – 46 votes. Among the coalitions governing some of the federal states are parties opposed to any changes in Germany’s fiscal rectitude. All the federal states governed exclusively by the CDU, CSU, SPD, Greens or the liberal FDP could provide 49 votes, which would suffice.

However, it is by no means certain that the FDP will vote in favour, which could prevent the two-thirds majority being reached. So, there remain considerable hurdles to be overcome before the ‘whatever it takes’ proposal becomes law.

It’s urgent!

The passage of this legislation is further complicated by the fact that the objective is to push the proposals through the current parliament. The new German parliament elected on 23 February must convene no later than 24 March, so the window of opportunity is narrow.

Following the elections, in the parliament’s new composition, the Green Party is diminished, as is the SPD. Therefore, a two-thirds majority would require either the Left Party or the far-right Alternative for Germany (AfD) to support the CDU/CSU and SPD in their motion, which looks unlikely: The AfD rejects any change to the debt brake, while the Left Party opposes any increase in military spending.

Merz’s explicit reference to doing ‘whatever-it-takes’ suggests that the level of commitment to ensuring the successful implementation of this legislation will enable any necessary compromises to be reached in the negotiations with other parties. But markets will be following developments closely and, as we have been reminded, a week is a long time in politics.

The impact on markets

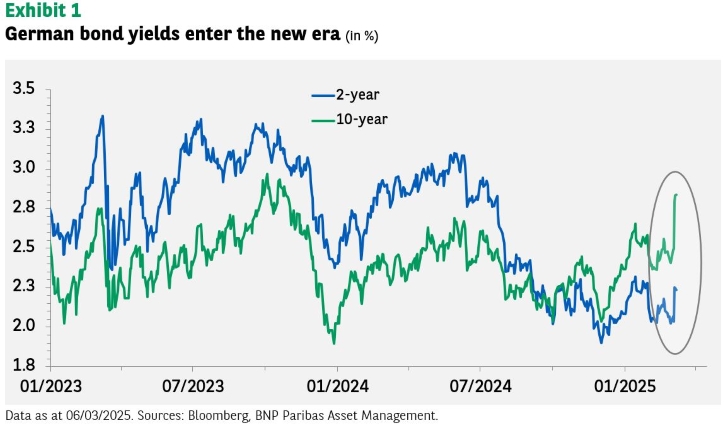

Yields of benchmark 10-year German government bonds surged by the most in 28 years on 5 March, as markets anticipated a major boost to Germany’s economy from the proposals to fund extensive investment in the military and infrastructure.

The yield on the 10-year Bund has risen this week by around 37bp to around 2.85% as markets reprice debt on the expectation of an increase in government borrowing.

The consensus view is that the combination of the European Council’s declarations on European defence, the European Union’s ReArm Europe plan, Germany’s €500 billion infrastructure investment fund and the tweak to its debt brake constitute a seismic shift in public spending.

These measures are likely to have a significant positive long-term impact on both growth and inflation, increasing the level of potential GDP by 1.5% in Germany and 0.8% in the eurozone by 2030.

A significant acceleration in German growth could be expected as early as the second half of 2025, with growth rates possibly approaching 2% per annum. This is in sharp contrast to previous forecasts of continued stagnation. Germany’s GDP has shrunk for the last two years as the economy has struggled with high energy costs, weak corporate investment and feeble consumer demand.

For yields of eurozone government bonds, the combination of a better growth outlook and higher supply implies a structurally higher range over time. A surge in bond supply alone could push forward pricing of German government debt significantly higher out to 2028, suggesting that this week’s repricing in 10-year Bund yields constitutes a re-anchoring to higher levels rather than a short-term move which will fade.

Spreads between eurozone government bonds should benefit from the positive impact of spending on growth, as well as the scope for more European Union-wide bond issuance.

In foreign exchange markets, the euro should benefit as the fiscal reforms presage a structural shift, in our economist’s views. The euro should be bolstered by relative capital allocation and European investors being crowded into domestic fixed-income markets.

This week’s sell-off in German government debt markets does not appear to reflect market concerns about the sustainability of Berlin’s debt, which at around 63% of GDP is far lower than the level in other big western economies.

In contrast with recent rises in borrowing costs in countries such as the UK, which have threatened their fiscal plans, markets are pricing in a better growth trajectory, boosting risky assets such as stocks at the expense of safe-haven government debt.

The ECB waits to see

At its policy meeting on 6 March, the ECB signalled a possible slowdown in rate cuts, as policymakers reduced the benchmark interest rate by a quarter point to 2.5%. The move was widely expected. It is the sixth cut in the ECB’s deposit rate since the start of the rate-cutting cycle in June 2024, when the benchmark stood at 4%.

There was a change of tone in the ECB’s communication that potentially signals a less dovish stance. The ECB said that ‘monetary policy is becoming meaningfully less restrictive’. This may mean a slowdown or pause in future rate cuts is ahead. It compares with the ECB’s previous wording that ‘monetary policy remains restrictive’

Christine Lagarde, ECB president, specified that the shift in wording was ‘not an innocuous little change’. She also raised the prospect of pausing the ECB’s series of rate cuts, saying they remain data-dependent.

The outlook for the eurozone economy could clearly be affected by moves by Germany’s new government to take on hundreds of billions of euros in borrowing to boost defence spending and overhaul Germany’s infrastructure. The prospect of this fiscal bazooka had prompted markets to reduce their expectations for ECB rate cuts prior to the ECB meeting.

In projections that did not consider the proposed German policy change, the ECB cut its growth forecast for 2025 — its sixth successive downgrade for the year — as well as for 2026 and 2027. It now expects eurozone GDP to increase by only 0.9% in 2025, compared with its December projection of 1.1%.

Christine Lagarde noted that ‘high uncertainty, both at home and abroad, is holding back investment and competitiveness challenges are weighing on exports,’ emphasising that policymakers face an acutely uncertain environment.

She added that ‘an increase in defence and infrastructure spending could add to growth’ and ‘could also raise inflation through its effects on aggregate demand’.