- Europe is investing heavily in technology, energy, defence and other areas, aiming to ensure its strategic autonomy

- It faces multiple challenges amid a fragmented regulatory and policy backdrop

- We believe its drive towards independence is creating attractive investment opportunities as part of a long-term structural theme.

Geopolitical tensions and an uncertain economic outlook underline the importance of strategic autonomy – the idea that nations are able to make their own policy decisions, ensuring security and economic expansion, without depending on other countries.

The permacrisis backdrop – be it the pandemic, the Ukraine war, trade wars, or the Middle East conflict – has highlighted the need for Europe to assert its own strategic autonomy. The region wants to boost economic growth, protect supply chains, foster greater innovation and competitiveness and ensure security in the changing geopolitical landscape.

For Europe, acting autonomously requires reducing dependencies in several key sectors – food, health, energy, industry and technology, as well as defence. They are interconnected, with one key theme running through them all: technology.

From high-tech defence capabilities to smart energy grids supporting the low carbon transition, technological infrastructure is key to European strategic autonomy.

Structural themes at the heart of investment

By our calculations, to make the bloc more autonomous, nearly €1.5 trillion of investment will be deployed across Europe by 2035. This includes

- The Readiness 2030 defence spending plan

- Germany’s 2025 spending package with as a significant infrastructure component as well as defence

- Investment in clean energy solutions with the dual objective of achieving energy independence and decarbonisation

- The European Chips Act aiming to double Europe’s market share in semiconductor chips production.

We see many potential investment opportunities in the companies exposed to sectors which should benefit from the increased spending and development. This is a long-term, structural theme allowing investors to seek returns while helping to finance Europe’s effort towards strategic autonomy.

However, the path towards strategic autonomy is not always straight. Yet we believe that Europe is moving in the right direction, even if the pace may have to accelerate.

European governance, and its development, is a case in point – against a fragmented regulatory and policy backdrop, there is increasing awareness that decision-making lacks agility and must improve.

The recent ‘E6’ proposal by France and Germany, which brings together six leading European economies to strengthen the region’s competitiveness and defence capabilities, illustrates this shift.1 The plan aims to overcome the inherent slowness in decision-making among the 27 member states and enable a core group of countries to make faster progress on economic and strategic priorities.

The defence spillover effect

While several EU measures include lower import quotas and increased customs duties to protect its steel industry,2 member states are also rapidly increasing defence spending, with some set to meet NATO’s 3.5% GDP target ahead of 2035.

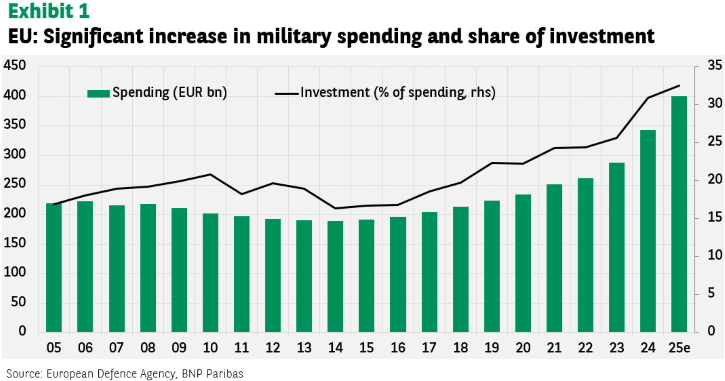

The Readiness 2030 €800 billion investment plan has seen strong progress with commitments being met; EU countries are estimated to have spent €392 billion on defence in 2025.3

According to the European Defence Agency, investment represents a growing share of defence spending, and research and development is increasing rapidly.4 Spillover effects are emerging in European industry, contributing to the rebound in production.

The EU has adopted new mechanisms to facilitate the increased investment, such as the Security Action for Europe programme (SAFE) which offers financing through long-term loans. Military spending is projected to reach 2.5% of European GDP (an increase of 0.6 percentage points in two years) and exceed the previous 2% of GDP NATO target in over three-quarters of EU member states.5

Space has emerged as a focal point on the geopolitical stage, in terms of both economic prosperity and strategic importance in the coming decades. The European Space Agency approved a record €22 billion budget for 2026-20286 – a more than 30% increase – aiming to strengthen Europe’s strategic autonomy in space technologies and missions.

More recently, the Middle East conflict has reinforced the importance of resource independence and energy security, especially in Europe.

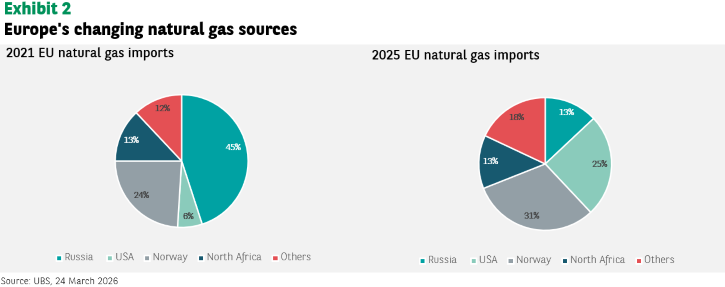

Europe has stepped up the diversification of its energy mix since 2021 via an increase in liquefied natural gas, high stock levels and expanded suppliers (see Exhibit 2), but it remains vulnerable to global markets and competition with Asia, particularly regarding gas.

The acceleration of the RePowerEU plan supporting the transition to clean energy, investments in energy networks, the revival of nuclear power and the development of renewables should support the resilience of Europe’s energy mix.

These proposals and decisions, while not exhaustive, demonstrate that Europe is moving forward in its governance approach and taking concrete action towards strategic autonomy.

A new chapter for Europe

Nevertheless, there are still challenges to overcome: interests and priorities naturally differ from one country to another within the EU’s 27 member states.

Coordination issues are particularly visible in major European projects. For example, the reported dispute between France and Germany regarding the project governance of the Future Air Combat System7 or delays around the Main Ground Combat System, a joint project to develop a next-generation military vehicle.8

Disagreements over such programmes can create uncertainty for investors around the theme of strategic autonomy. However, looking at the medium to long-term trajectory, we believe it is clear that Europe is still moving in the right direction.

Defence is, however, just one component of a much broader strategy that encompasses energy, industry, technology, sustainability and more. Long-term government funding plans are important supports for this structural change which create a myriad of potential investment opportunities as well as the prospect for investors to be at the forefront of what may be a new chapter in the history of European integration.

[2] New measures to protect EU steel market from global overcapacity | News | European Parliament

[3] European Defence Agency Defence Data 2024-2025

[4] European Defence Agency Defence Data 2024-2025

[5] Readiness 2030: one year after its announcement, the European rearmament plan is on track

[6] ESA – ESA Member States commit to largest contributions at Ministerial

[7] France’s Macron and Germany’s Merz to discuss troubled fighter project, sources say | Reuters

[8] Germany dispel doubt over commitment to FCAS, MGCS – Army Technology