This article is part of the Fixed Income Quarterly Outlook for Q3 2026, covering Emerging Market Debt, Euro Credit, Euro High Yield, Sovereign Bonds and US Agency Mortgage-Backed Securities.

By Olivier Monnoyeur, European High Yield Portfolio Manager

- European high yield delivered a solid second quarter amid very strong issuance and robust investor demand, despite geopolitical volatility and energy price fluctuations.

- Credit fundamentals remain supportive, with low default rates, stable balance sheet trends, and a manageable refinancing profile.

- While the third-quarter outlook remains positive due to attractive carry and low default expectations, tight spread levels require a more selective investment approach.

European high yield delivered a solid second quarter despite increased volatility driven by the US-Iran conflict, energy price fluctuations and concerns about global growth.

Market performance was supported by strong technical considerations, attractive yield levels and continued investor demand for carry, i.e., income less funding costs.

Spreads compressed by 54 basis points in Q2 to 315bp. Return for the year stands at +1.7%. The market remains bifurcated between performing, high quality names and the rest, which is illustrated in the extremely wide spread of the CCC index at 1260bp versus BB at 211bp according to J.P. Morgan.

Record primary market activity

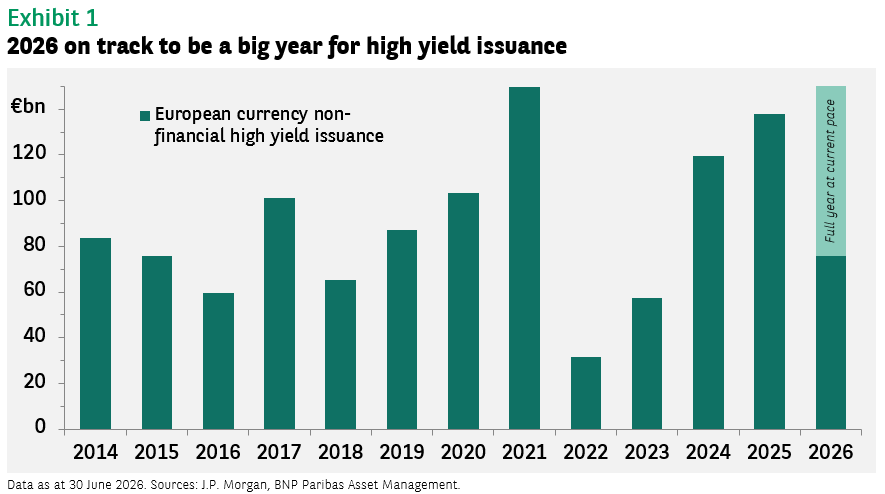

The second quarter was one of the busiest quarters on record for European HY issuance. Gross issuance reached approximately €49bn according to J.P. Morgan, a new quarterly record, while market access remained strong across sectors and rating categories.

The issuance mix remained skewed towards higher-quality issuers (58%), although single-B activity increased (36%) compared with Q1 (25%).

Importantly, the market absorbed this large supply without any significant widening in spreads, highlighting the strength of demand.

Investor demand remained exceptionally strong throughout the quarter, supported by attractive all-in yields relative to cash and investment grade alternatives as well as continued demand for income-generating assets.

In addition, there was limited refinancing pressure while spreads remained narrow at close to post-global financial crisis levels, reflecting the scarcity of yield, the dominance of the BB sector and the continued search for carry.

Credit fundamentals remain supportive

The first quarter’s earnings season was solid, and expectations were for profit and cash flow to remain robust in Q2.

During Q2, corporate fundamentals continued to prove resilient as default rates remained very low with expectation for a drop to 2.4% by the end of 2026, according to J.P. Morgan.

Most issuers maintained good access to capital markets and refinancing risk remained manageable given limited near-term maturities while balance sheet trends were generally stable across the market.

Outlook: Constructive backdrop, less room for error

We remain constructive on European HY entering Q3, although risk-reward appears less compelling than earlier in the year as spreads remain historically tight.

We think the Middle East conflict will have a measured impact on the growth/inflation mix which we expect to improve in 2027 with 1.3% of growth supported by the German investment plan and a possible recovery in construction activity which has been depressed since 2022.

We can see three supportive factors:

- Attractive carry: All-in yields remain elevated at 5.74% including CCC (5% excluding CCC) compared with long-term averages and continue to provide a meaningful cushion against moderate spread widening based on J.P. Morgan data. Carry is expected to remain the primary driver of returns in the coming quarter

- Favourable refinancing profile: The HY maturity schedule remains relatively benign over the next two years, reducing refinancing concerns and supporting corporate fundamentals

- Stable default environment: Default expectations remain low and credit metrics across much of the market remain adequate despite slower economic growth

Key risks to monitor

In our view, the main challenge for the asset class is valuation. Current spread levels leave limited room for disappointment should macroeconomic conditions deteriorate or geopolitical tensions escalate.

And Middle East developments remain the most significant macro risk for credit markets; any further disruptions to energy markets or shipping routes could trigger renewed volatility in risk assets and increase pressure on energy-intensive issuers.

Overall, European growth remains positive but modest. The market is transitioning from a broad beta rally to an environment where issuer and sector selection are likely to play a greater role in performance generation.

Investment implications

Currently, going into Q3, we have a preference for performing single B vs high BB and bonds with higher carry and less focus on capital appreciation.

We are neutral beta with a reduced exposure to hybrid bonds and additional tier one (AT1) bonds which we think are too crowded. We are also cautious on CCC as many have vulnerable fundamentals, with weak cash flow and some difficult 2028 and 2029 maturities to manage

But we do favour defensive sectors with resilient cash flow profiles (telecommunications, healthcare and real estate), companies with clear deleveraging paths and good free cash flow generation and positions offering attractive carry without requiring further spread compression to generate returns, including floating rate notes

However, we remain more cautious on highly leveraged issuers, cyclical credits with limited free cash flow visibility and companies exposed to sustained energy cost inflation.

Since the US and Iran signed the Memorandum of Understanding we have re-focussed our attention to sectors and names that have been negatively impacted by the conflict.

These include rate sensitive sectors like real estate, or anything related to construction, packaging and some consumer companies.

Dispersion was elevated in Q2 and there are quite a few situations whose bonds have lost value on reduced investor confidence and some shorting activity by hedge funds.

There will thus be solid opportunities for recovery for investors with risk appetite willing to express conviction. We have targeted some names that fit these criteria and continue to scout for opportunities.

We think three themes will focus most of our attention and will drive the outperformance potential for the rest of the year:

- AI winners and losers. We very early on reduced our exposure to artificial intelligence-threatened software companies. We continue to underweight the sector but there are some nuances between more protected and more exposed business models. We continue to do more work on the topic. Conversely, we continue to gain exposure to the AI theme. We expect to see more issuance and that theme to grow in importance for our market

- Anything linked to construction: Investor sentiment to the theme is weak. We think this is an opportunity. While we don’t expect a recovery in 2026, expectations are for a modest rebound in 2027. Some names have a more significant exposure to renovation and maintenance than new build. They can afford to wait for the rebound, while their cash flows cover their cost of capital. We as bondholders are being paid to wait in nonconsensual situations

- Chemicals: We need to differentiate between the commodity chemicals and the specialty. The specialty usually has a more robust business model, or at least less cyclical. They offer some cyclicality but there are some nuances and some sub sectors that are more stable with robust cash flow profiles. The commodity ones have had a very volatile ride year to date. The Strait of Hormuz closure created massive disruption in the sector, which has supported their margin and market share (to the detriment of Asian and Middle East operators). The market has concluded that its reopening brings them back to where they were before the war. We disagree and are positioned accordingly.

The next stage

European HY delivered another strong quarter powered by exceptional technicals, robust investor demand and record issuance volumes. Looking ahead, the outlook remains constructive, supported by attractive carry, low default expectations and manageable refinancing needs.

However, with spreads at historically tight levels and geopolitical risks elevated, we believe selectivity will become increasingly important in generating excess returns during the second half of 2026.