This article is part of the Fixed Income Quarterly Outlook for Q3 2026, covering Emerging Market Debt, Euro Credit, Euro High Yield, Sovereign Bonds and US Agency Mortgage-Backed Securities.

By Alaa Bushehri, Head of Emerging Market Fixed Income

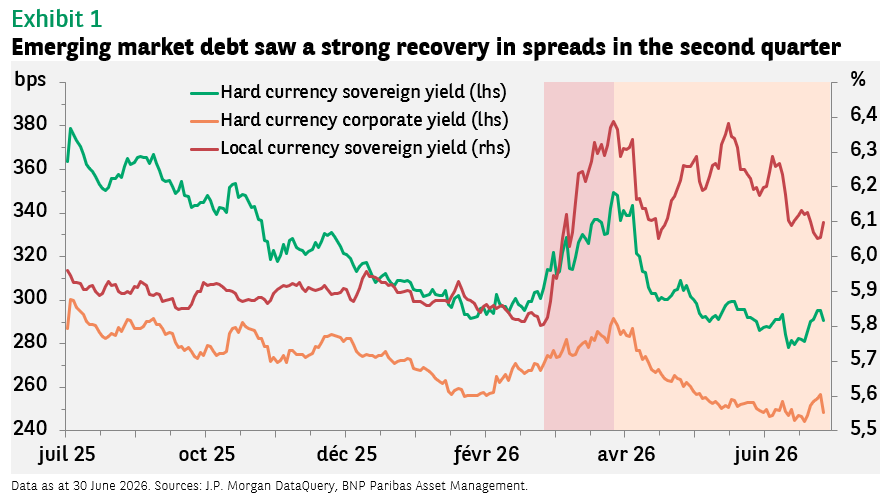

- Emerging markets demonstrated significant resilience during the second quarter of 2026, despite ongoing volatility driven by the Middle East conflict, energy crises, and geopolitical uncertainty

- The geopolitical landscape has created a clear distinction between EM beneficiaries — specifically oil-exporting nations with stronger fiscal revenues — and vulnerable oil-importing economies facing higher inflation and import costs

- As broad market returns tighten, the focus has shifted toward disciplined country selection, prioritising markets with durable fundamentals, credible monetary policies, and attractive real yields to ensure sustainable returns

Emerging markets endured continued volatility arising from the Middle East conflict and resultant energy crisis in the second quarter.

But while geopolitical flare-ups remain an ongoing risk, we believe investors can still potentially benefit from resilient fundamentals, compelling yields, and idiosyncratic drivers unique to emerging markets.

Normalisation, or too soon?

The second quarter began against a backdrop of heightened conflict in the Middle East, testing several long-standing vulnerabilities across EM, including regional energy-price sensitivity, supply-chain fragility and renewed geopolitical uncertainty.

The situation remains fluid, with repeated setbacks in negotiations, attacks on neighbouring infrastructure and disruption risks around key global chokepoints. This environment reinforces several important considerations for both Middle East dynamics and the broader EM outlook:

- As geopolitical shocks increasingly reverberate through energy markets, shipping routes, food systems and broader supply chains, we are likely to see a further acceleration in regionalisation and de-globalisation. Countries may continue to become more inward-looking, rely on a narrower set of strategic partners, and place greater emphasis on economic security, protectionism and supply-chain resilience, particularly in critical areas such as technology and energy.

- The oil price rise has sharpened the distinction between those countries that benefit from it and those that are more vulnerable. Oil-exporting markets, including the Gulf Cooperation Council (GCC), have generally benefited from stronger fiscal revenues, improved terms of trade and more resilient external balances. By contrast, oil-importing economies, such as India and Turkey, have faced higher import bills, renewed pressure on inflation and a greater potential drag on the current account.

- Developing markets are likely to continue demonstrating resilience, even against a backdrop of elevated geopolitical uncertainty and the risk of prolonged conflict. Importantly, this resilience is increasingly underpinned by country-specific fundamentals, with many markets benefiting from improving growth dynamics, credible central bank policy and greater fiscal discipline.

Inflation considerations

We have seen higher energy prices already starting to filter through to consumer prices, and for now at least, inflation remains a concern for central banks globally.

Therefore, we have seen market expectations of Federal Reserve rate cuts shift from two cuts by the end of the year to no cuts or even hikes, which could be enough to inspire some EM central banks to keep rates on hold and shift any planned cuts into 2027.

Moreover, the scope for fiscal policy to cushion external shocks remains constrained, as elevated debt burdens and higher financing costs limit the ability of governments to deploy the broad-based, untargeted support measures seen during the pandemic.

As demonstrated throughout 2025 and the first half of 2026, the US will continue to play a pivotal role in shaping the direction and volatility of EM assets. While markets are still digesting the impact of earlier tariff disruptions and the ongoing Middle East conflict, the upcoming US mid-term elections create scope for further uncertainty.

US President Donald Trump may adopt a more assertive policy stance to influence the electoral narrative, although there is also the possibility that the administration seeks to reassure markets through measures that promote a degree of stabilisation.

Taken together, these dynamics reinforce the need to separate cyclical volatility from the more durable structural improvements now visible across parts of EMs.

The importance of selectivity

Emerging markets enter the second half of 2026 from a position of established resilience, yet this resilience has made selectivity increasingly important in the sector.

Stronger growth differentials versus developed markets, improving external balances, and credible monetary policy frameworks continue to support the asset class, offering compelling income and diversification potential.

However, valuations have tightened meaningfully across parts of hard currency credit, leaving less room for broad beta-driven returns.

Going forward, investors should therefore distinguish between markets supported by durable fundamentals, credible reform momentum, and attractive risk premia, and those more vulnerable to policy slippage, fiscal pressure, or external shocks.

In local currency, easing cycles and still-elevated real rates remain supportive. Overall, the opportunity set remains attractive, but disciplined country selection, active management, and robust risk controls will be essential to converting EM resilience into sustainable returns.

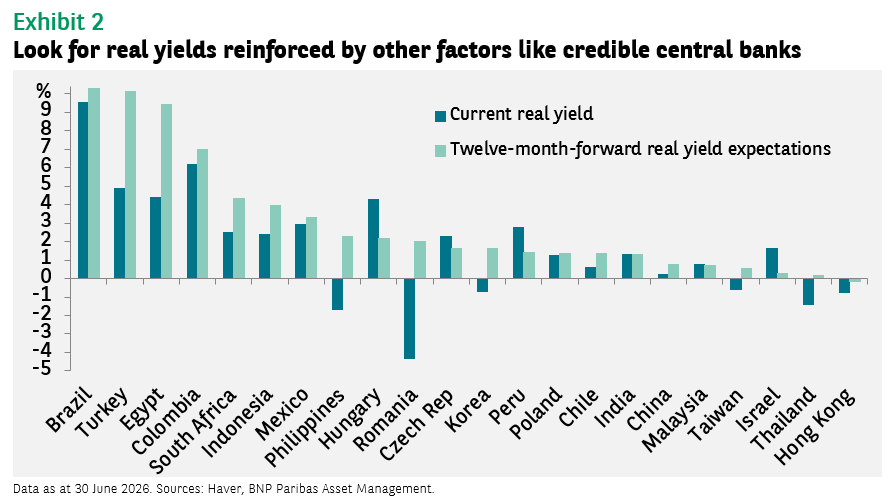

Real yields and undervalued currencies

In our view, local currency emerging market debt remains one of the more compelling areas of the asset class, supported by attractive real yields in places, improving inflation dynamics and a more credible policy backdrop across many key markets.

While the global rates environment remains an important source of volatility, several EM central banks retain scope to ease gradually without compromising macro stability, particularly where inflation expectations are anchored and external balances have strengthened.

This creates an attractive carry and duration opportunity, but one that requires careful differentiation across regions and policy regimes.

Developing market currencies also appear selectively attractive after periods of pressure, with valuation support, lighter positioning and improving current account dynamics providing a constructive medium-term foundation.

However, currency performance is likely to remain highly sensitive to the US dollar, commodity prices and geopolitical shocks. As such, investors should prioritise markets where high real yields are reinforced by credible central banks, disciplined policy frameworks and robust risk management.

Geopolitical fragility – what next for emerging markets?

Geopolitical fragility is likely to remain a defining feature of the EM landscape in the second half of 2026.

For investors, the key question is no longer whether EMs can withstand geopolitical shocks, but which countries are best positioned to absorb them. Energy exposure, external financing needs, food-price sensitivity and policy credibility will all be critical differentiators.

Oil exporters may benefit from improved terms of trade, while import-dependent economies remain more vulnerable to renewed energy price spikes and inflation pass-through.

The upshot

Overall, markets demonstrated commendable resilience over the second quarter despite a highly challenging backdrop. While ongoing geopolitical events suggest that conditions may be becoming more stable and somewhat clearer heading into the second half of 2026.

If a de-escalation occurs, it could help restore investor confidence, support a normalisation in oil prices and encourage a more constructive view on inflation. However, with geopolitics likely to remain a persistent theme, we believe investors should continue to prioritise selectivity and disciplined risk management across EM allocations.