This article is part of the Fixed Income Quarterly Outlook for Q3 2026, covering Emerging Market Debt, Euro Credit, Euro High Yield, Sovereign Bonds and US Agency Mortgage-Backed Securities.

By John Carey, Head of Structured Securities

- The mortgage-backed security sector has been resilient, with positive year-to-date total returns

- Agency MBS fundamentals remain strong due to elevated mortgage rates and a lock-in effect that has stabilised prepayment behaviour and limited new supply

- The outlook remains good and we prefer a modest overweight position to MBS, driven by high-quality carry, liquidity, and diversification benefits

Fundamentals

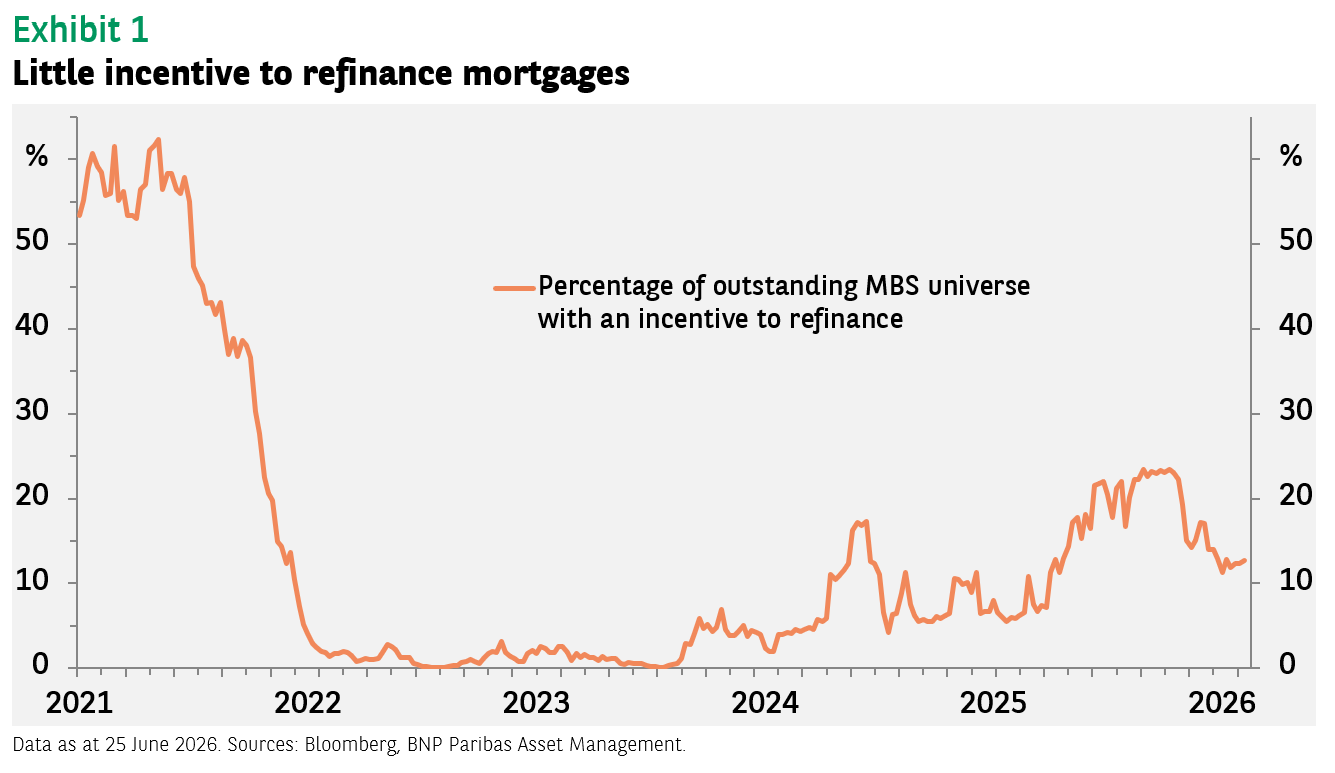

Agency mortgage-backed securities fundamentals remain supported by a combination of elevated mortgage rates, limited refinancing incentives, constrained housing turnover, and low net supply.

Primary mortgage origination rates have remained around the mid-6% area. This rate environment continues to limit refinancing activity and new origination supply, while the broader lock-in effect has kept a large portion of the mortgage universe out of the money.

Prepayment behaviour has therefore remained relatively stable and well behaved. The June prepayment report showed an 11% decrease in 30-year Federal National Mortgage Association aggregate speeds, with elevated mortgage origination rates slowing refinancing activity more than anticipated in higher coupons.

Lower coupons rose only marginally due to seasonal housing turnover, while mortgage origination rates stayed near 6.45% during the month. Only 12% of the mortgage universe has a meaningful incentive to refinance, reinforcing the case for a stable prepayment profile.

Demand and supply technicals also remain favourable. The current environment is one with good investor demand from money managers, banks, real estate investment trusts and overseas investors, alongside range-bound mortgage origination rates that are limiting refinancing activity and new origination supply.

Spreads and valuation

Agency MBS valuations remain broadly fair relative to other high-quality fixed income sectors, although spreads have tightened from the wider levels observed during the March volatility episode.

Coupon nominal spreads were around +100 at the end of July and attractive versus US Treasuries.

From a relative value perspective, Agency MBS continues to compare favourably with investment grade credit with attractive spreads versus investment grade credit, diversification benefits, and high-quality income without corporate credit risk.

Investor demand is strong, and stable mortgage origination rates and favourable technical factors further support the asset class.

Absolute yield levels also remain a key part of the valuation case. The Bloomberg US MBS Index yield is approximately 5.01%, with current coupon nominal spreads around +100 bps and current coupon option adjusted spread is around +12 bps (data from JPM DataQuery as at 1 July 2026).

The current coupon parity yield is approximately 5.46% (data from JPM DataQuery, 7 July 2026 ) and that to-be-announced dollar rolls in production coupons continue to offer attractive carry. These levels suggest that, even if spreads are no longer cheap versus their own recent history, the sector continues to offer meaningful carry and liquidity in a high-quality framework.

Present outlook

The current environment therefore supports a positive bias toward MBS, particularly for institutional investors seeking high-quality carry, liquidity and diversification relative to credit sectors.

At the same time, the valuation argument is more nuanced. Spreads are no longer as wide as they were during the March dislocation and are closer to when they were much narrower, meaning further spread tightening may be more limited. We are therefore neutral on spreads given valuations near the tights.

We currently prefer a modest overweight to Agency MBS, focused on carry, liquidity and relative value versus investment grade credit. We initiated an MBS overweight driven by absolute yield levels and fair spreads, with a preference to increase exposure only on cheaper valuations or further progress in the peace process.

We maintain our overweight recommendation for MBS for carry and diversification benefits, while monitoring Fed policy under Warsh’s leadership.

The main risks are a renewed rise in rate volatility, additional curve flattening, tighter spread valuations and uncertainty around Fed policy.

However, with mortgage rates limiting refinancing activity, net supply low, and demand supported by multiple investor bases, the medium-term outlook remains constructive, with carry likely to be the dominant return driver.