This article is part of the Fixed Income Quarterly Outlook for Q3 2026, covering Emerging Market Debt, Euro Credit, Euro High Yield, Sovereign Bonds and US Agency Mortgage-Backed Securities.

By Victoria Whitehead, Lead Portfolio Manager

- The outlook for the second half of 2026 remains positive, supported by robust corporate fundamentals, a supportive macro backdrop, and favourable technical conditions

- With spreads tight, future performance is expected to be driven primarily by carry and disciplined security selection rather than significant spread tightening

- At present, we prefer European financials, particularly banks, and selected BBB-rated issuers. We also like European industrials benefiting from infrastructure spending and domestic investment

We are positive on euro investment grade credit going into the second half of 2026.

While valuations are increasingly demanding after the strong spread compression observed in the first half of the year, the asset class continues to benefit from a supportive macroeconomic backdrop, solid corporate fundamentals, and favourable technical conditions.

As a result, we expect carry (coupon income minus cost of funding), and credit selection to remain the primary drivers of performance, rather than further significant spread tightening.

Macroeconomic environment

The European economy is expected to continue expanding at a moderate pace, supported by improving domestic demand and fiscal stimulus measures, particularly in Germany.

Inflationary pressures continue to ease, helped by lower energy prices and a more balanced labour market, allowing monetary policy to remain broadly supportive. This backdrop should remain conducive to corporate credit performance.

Nevertheless, investors should remain attentive to geopolitical developments and potential trade tensions, which could periodically increase market volatility and affect risk sentiment.

Valuations and market outlook

Following a resilient first half of 2026, euro investment grade (IG) spreads remain narrow. While this limits the scope for meaningful spread compression, absolute yields continue to offer attractive income opportunities compared with long-term averages.

Consequently, returns are likely to be dominated by carry rather than capital appreciation from tighter spreads.

At the same time, elevated issuer and sector dispersion continues to create opportunities for active managers to generate alpha through security selection.

Corporate fundamentals

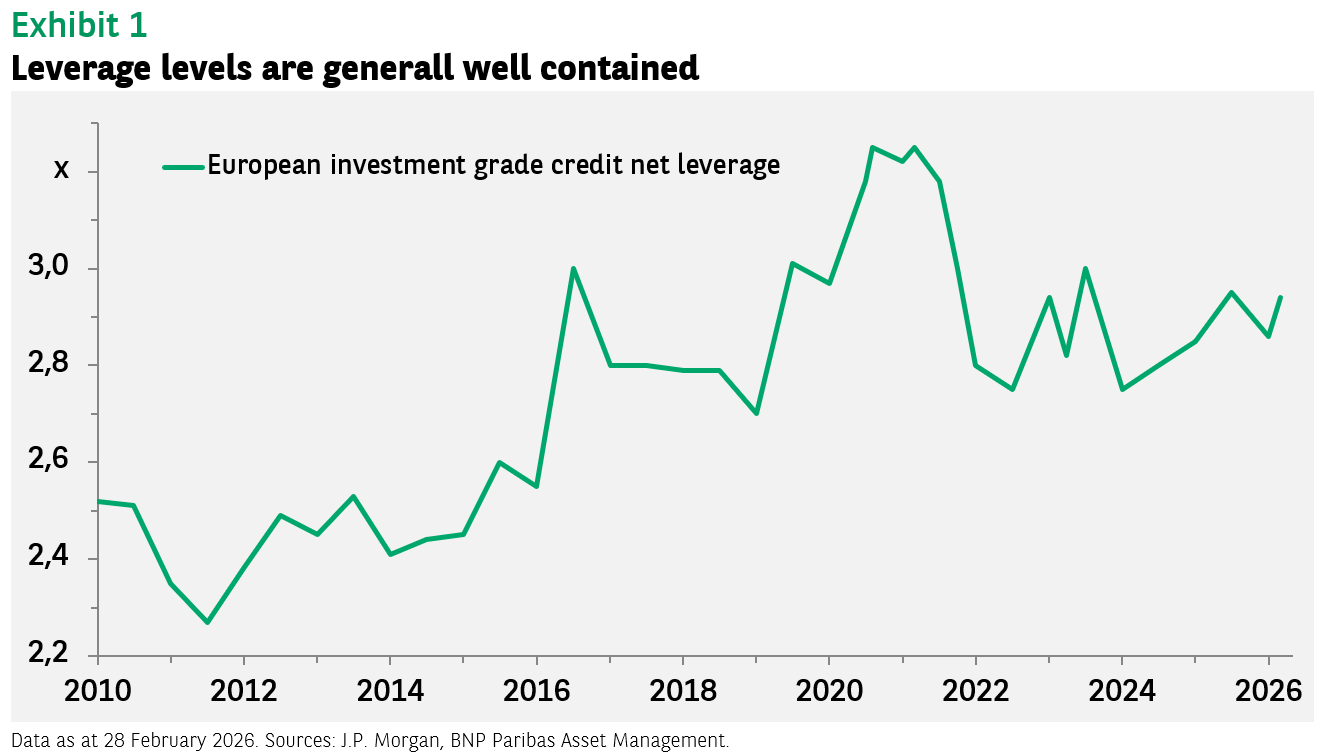

Euro IG corporate fundamentals remain robust. Leverage levels are generally well contained, liquidity positions are healthy, and free cash flow generation remains supportive across most sectors.

Despite a more challenging economic environment than in recent years, European corporates have demonstrated resilience and continue to maintain strong balance sheets.

European banks remain a key area of strength. Capital ratios are comfortably above regulatory requirements, asset quality metrics remain solid, and earnings continue to benefit from a higher-for-longer interest rate environment.

The potential for increased defence spending in Europe as well as huge investment in artificial intelligence infrastructure bodes well for future profitability of the European industrial and manufacturing sectors. As such we are actively looking to invest in this space using new issuance as an entry point.

Technical factors

Market technicals remain supportive despite elevated issuance volumes. The primary market successfully absorbed record supply during the first half of the year, highlighting the continued demand for high-quality credit and attractive income opportunities.

Supply should moderate during the summer period, further strengthening the technical backdrop.

Any periods of spread widening driven by heavy issuance or temporary volatility are likely to offer attractive entry points for long-term investors.

The technology sector is of particular relevance currently, with a huge amount of new issuance from hyperscalers hitting the market predominantly in US dollar IG public and private credit markets.

The euro IG bond market has been relatively untapped so far by the US tech sector, and we expect a significant increase in issuance in the fourth quarter. Current positioning in technology issuers is fairly light and we are underweight the long end of this sector, which we believe could potentially underperform.

Investment preferences

Given the present environment, we continue to favour European financials, particularly banks and selected subordinated debt. We also like European industrial issuers benefiting from infrastructure spending and domestic investment and BBB-rated credits, where spread compensation remains more attractive than higher-rated segments.

Conversely, we remain more cautious on data-centre real estate investment trusts and selected real estate-related credits as well as private-equity-related issuers. We are also more wary of certain US financial issuers accessing the euro market and highly rated defensive sectors where valuations appear particularly rich. We expect to be opportunistic buyers of US tech issuance.