Rates and credit returns come together in corporate bond market

Corporate bond returns are comprised of a risk-free yield and a credit spread, which compensate investors for taking on more risk relative to government bonds.

Spreads have been in trend decline for over a decade. However, underlying yields have increased since 2022. As such, the credit spread share of total yield is at its lowest point since the global financial crisis (roughly 20% of investment-grade and 50% for high-yield corporate bonds).

Our macroeconomic outlook is benign, with little expected change in underlying yields or credit spreads. High-yield, which is shorter duration, is more suited to a buoyant outlook and ongoing equity performance. Any rise in underlying yields would have a limited impact on total returns.

Investment-grade indices, which are longer duration, would be less impacted by a deteriorating credit environment – any widening of spreads would be compensated by lower underlying yields.

Indeed, as more central bank interest rate cuts are expected, investment-grade returns should remain healthy, as they were in 2025. A reversion of the credit share of total yield to the historical average is not in our base case.

Overall, the fixed income outlook remains positive, and credit should perform well in 2026.

Positive outlook for equities with gains spread more evenly

Equity markets started 2026 with a bang. Global equity indices rose sharply in the first few days of the year.

Growing investor enthusiasm for non-US and non-technology shares has been (partially) validated so far: Emerging markets, Japan and Europe all outperformed the US.

Looking ahead, we expect the performance gap between tech and non-tech indices to narrow, but tech will still take the lead. The development of artificial intelligence (AI) technologies will likely continue to drive superior earnings growth, but the implementation of AI in other parts of the economy will allow companies to increase revenues and/or cut costs, driving a quicker increase in profits.

Although the Nasdaq index has lagged recently, emerging market tech stocks have topped most others. Europe should do better thanks to a significant increase in government spending on defence and infrastructure, which should help offset the drag from US tariffs and stiff competition from Chinese imports. Europe equity valuations are also meaningfully lower than those of US (value) stocks.

Japan’s strategic rise

2025 marked a pivotal year for Japan. The economy has emerged from a prolonged deflationary cycle, and Prime Minister Sanae Takaichi’s new administration has redirected efforts toward areas with the potential to boost long-term growth.

Japan’s economic policy emphasises advancing artificial intelligence and robotics; strengthening defence capabilities; continuing corporate reforms; and implementing inflation countermeasures alongside social security reforms.

The OECD has upgraded Japan’s 2025 growth estimate to 1.3% and expects inflation to stabilise at around 2%. As growth accelerates, surplus corporate cash presents opportunities to create new value through increased investment, higher wages, and shareholder returns.

Japan’s ascent is not without its challenges, however. The nation is balancing a ‘responsible and active fiscal policy’ amid high debt levels and ongoing monetary policy normalisation. Low interest rates have kept the yen weak, benefiting exporters, but consumers have faced declining purchasing power.

Geopolitical tensions and potentially higher oil prices pose additional risks. To sustain its rise, Japan has sought to evolve across multiple fronts, including increasing its strategic autonomy in areas such as energy and developing domestic alternatives to imports.

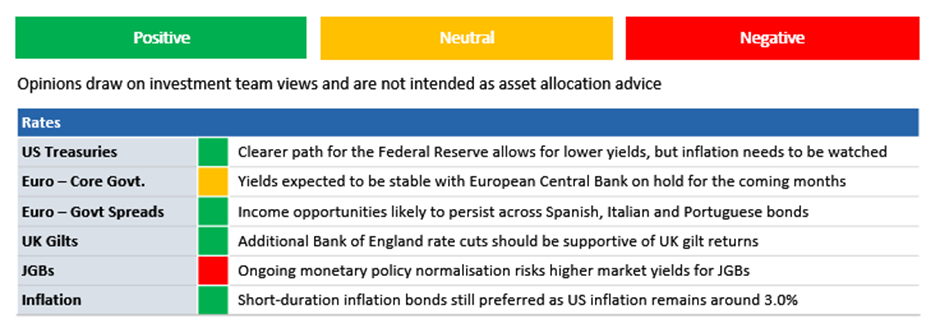

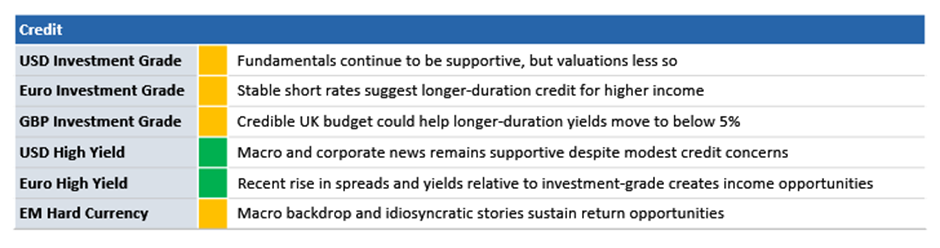

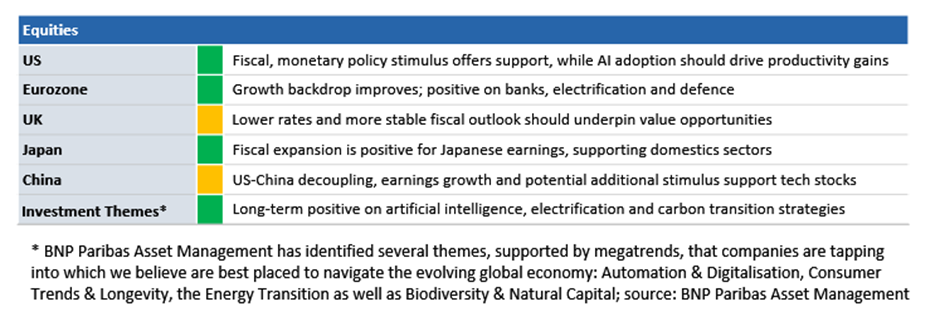

Asset class views