We are constructive on both the US and euro investment-grade segments as company fundamentals and technicals remain supportive in the context of slower growth and fiscal and trade policy uncertainties. This view translates into a neutral position favouring carry-oriented selective strategies.

At the macroeconomic level, the market is pricing in a no-recession outcome across IG and high-yield bonds (HY), leaving little upside, but plenty of downside. This underpins our generally cautious view on both valuations and relative values.

We believe companies are generally in good shape with stable leverage, improving revenues and margins, and a more disciplined approach to capital allocation. Companies have built sufficient cushions to face the risks a slowing economy could pose.

Credit market participants de-risked aggressively in the aftermath of April’s tariff news. That left them underweight when President Trump chose to de-escalate the trade conflict and the market began to rally. May and June was about playing catch-up to rebuild positions, mostly through absorbing supply.

While supply helped investors cover their underweights, they have had to absorb new inflows. In US IG credit, for instance, foreign demand has proven surprisingly resilient despite the significant risks those investments face from a weaker US dollar.

Euro credit

French and Italian life Insurers have again been competing with asset managers for assets, having raised significant new funds through gross premium collections in April.

Anecdotally, there is evidence that foreign investors are showing a new interest in euro credit.

Valuations

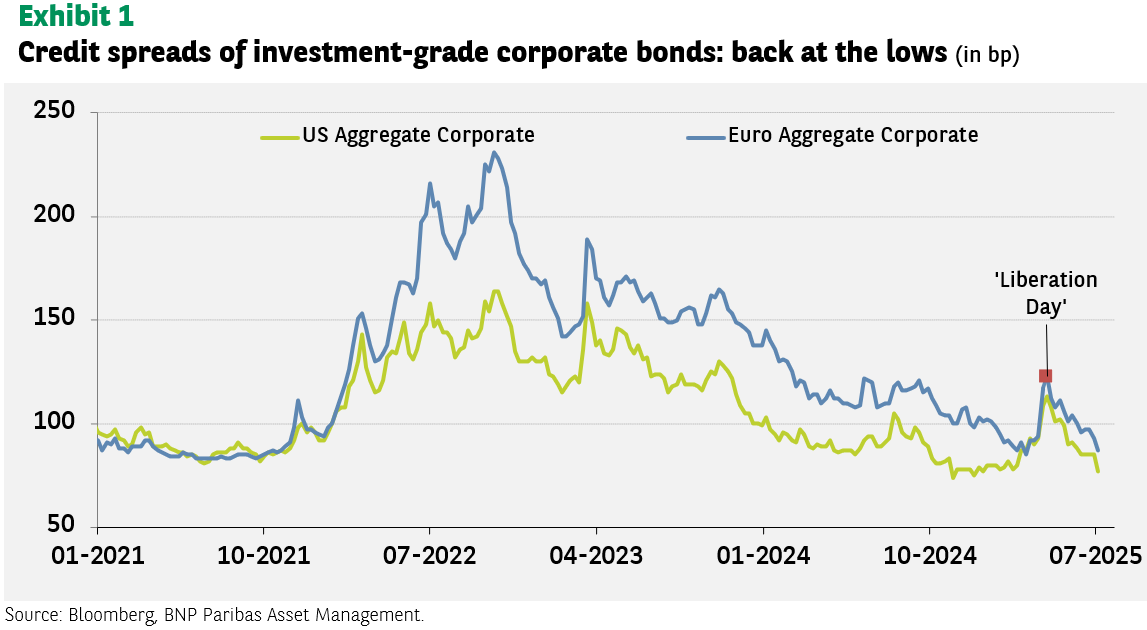

Valuations are approaching the tights of the year once again as strong technicals add to the supportive fundamentals. BBB rated corporate bonds now represent 46% of US IG benchmarks – the lowest level in 10 years. Relatively low dispersion between sectors favours credit selection with opportunities in the car, media, utilities, and financials sectors.

Yield curves

Yield curves are generally flat, and we see more value in the front end or the belly of the curve. The BBB/A spread ratio has come down since ‘Liberation Day,’ but remains high. We like BBB corporates ahead of what we expect what will be a summer of carry.

Credit default swap (CDS) indices are likely to underperform cash, not least given a moderation of supply going into the summer months.

Technicals

Technicals are a key driver of the market as investors reach out for yield and duration despite some softening of buying interest from exchange-traded funds and money market funds, which are more total return oriented. Gross and net supply are running lower than in the same period in 2024, a tailwind for credit spreads. This dynamic is expected to remain for the rest of 2025 given lower mergers and acquisitions activity.

This is an extract from our Q3 2025 quarterly fixed income outlook – full document.