The world of finance in two minutes. This week:

The US Federal Reserve left interest rates on hold at 3.5%-3.75%, reflecting uncertainty over inflation and the economic outlook in the wake of the Middle East conflict. The decision was widely anticipated, though one of the 12-member committee voted to lower the target range by 25 basis points. Fed Chair Jerome Powell said it was “too soon to know the scope and duration of the potential effects” the ongoing conflict may have on the US economy. However, the Fed revised up its expectations for GDP growth to 2.4% for 2026 and 2.3% for 2027, compared to its December forecast of 2.3% and 2.0% respectively.

Around the world

The European Central Bank also left interest rates on hold, keeping its main rate at 2% for the sixth consecutive meeting despite confirmation that Eurozone annual inflation increased to 1.9% in February from 1.7% in January. Core inflation – excluding energy, food, alcohol and tobacco – rose to 2.4% from 2.2%. The headline rate remained below the ECB’s 2% target, but it warned the conflict in Iran has created “upside risks for inflation and downside risks for economic growth”. Elsewhere, both the Bank of England and the Bank of Japan kept interest rates unchanged. In contrast, the Reserve Bank of Australia hiked its cash rate by 25bp to 4.1%.

Figure in focus: 1.33 milliseconds

Earth’s days are lengthening as the planet is spinning more slowly because of human-induced climate change, which has implications for technology, according to a new scientific study. Previous research indicated that days were becoming 1.33 milliseconds longer per century due to rising sea levels. A new study, published in the Journal of Geophysical Research: Solid Earth, found that this increase is unparalleled over the last 3.6 million years. Though slight, these changes could potentially cause problems for technology, impacting accuracy in computing systems such as GPS and satellite navigation. If global heating continues, the length of a day could be extended by 2.62 milliseconds by the end of the century, scientists predict.

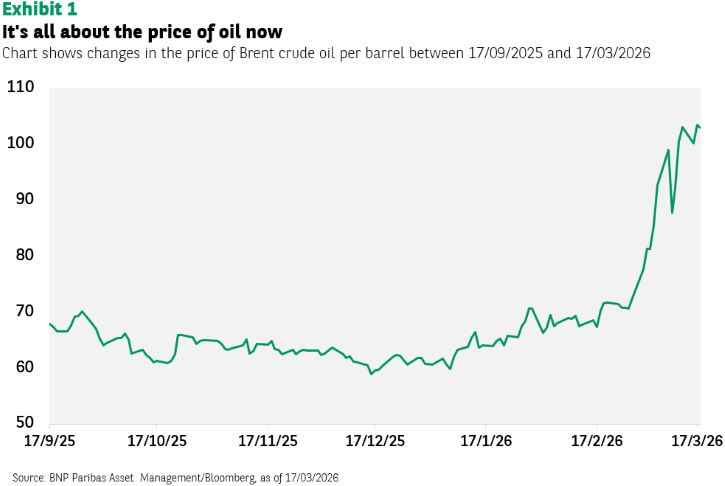

Chart of the week

The effective closing of the Strait of Hormuz, described by the International Energy Agency as the “largest supply disruption in the history of the global oil market”, has driven oil prices up by around 40% since the start of the Middle East conflict. Barring a sudden resolution and the Strait reopening, the energy shock could worsen, leading to higher inflation, which would negatively impact consumers’ real incomes and business profitability. The longer it goes on, the more the growth outlook is threatened. For this reason, the oil price is significant for investors. What comes next in terms of returns depends now on the size, breadth and persistence of this energy shock.

Words of wisdom: Industrial Accelerator Act

The European Union’s draft Industrial Accelerator Act intends to boost the bloc’s competitiveness through prioritising locally made and low-carbon products and technologies. EU countries and local authorities would need to meet “Made in EU” requirements when spending public money or offering subsidies in certain sectors, such as electric vehicle components. Meanwhile overseas companies investing in particular EU sectors would need to guarantee job creation. The draft regulation aims to increase manufacturing’s share of EU GDP to 20% by 2035, from 14.3% currently, and is seen as an effort to respond to competition from China.

What’s coming up?

On Tuesday, Japan posts inflation numbers for February; its annual inflation rate dropped to 1.5% in January, from 2.1% in December. In addition, several flash Purchasing Managers’ Indices are released, including those covering Japan, India, the US, UK, and Eurozone. On Wednesday the BoJ publishes the minutes of its latest monetary policy meeting, Germany issues its closely followed Ifo Business Climate index while the UK issues its own inflation update. The UK follows up with retail sales data on Friday.