A major reform moving the Dutch pension system from a defined benefit (DB) model to a defined contribution (DC) system is underway. The reform involves transitioning to an asset allocation with a shorter interest rate hedge, leading to less demand for long-dated bonds and possibly increasing volatility in the market for such bonds.

In its latest Financial Stability Review, the European Central Bank (ECB) has warned that the reform of the Dutch pension system may result in a selloff in long-maturity bonds and interest-rate swaps. Demand for these securities will drop as Dutch pension funds shift from the DB to DC model to better suit the needs of an aging population.

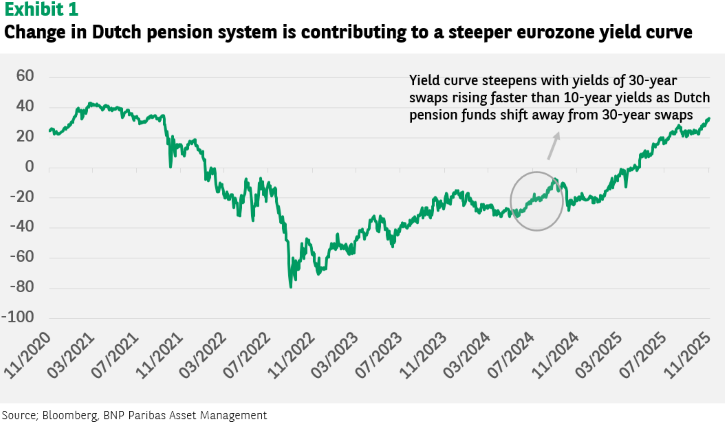

This change has been well-flagged and underway for some time. It will play out over several years. However, the size of the Dutch pension system – according to the ECB, it accounts for around 65% of eurozone pension funds’ sovereign bond holdings – means it is a major change in demand dynamics for long-dated eurozone debt. The gap between 10 and 30-year interest-rate swaps has already risen to around 32 basis points, the highest since 2021.

Our fixed income team have been positioned for a steeper yield curve and are monitoring developments closely.

Apart from the issue of a decline in demand from Dutch pension funds, longer-dated sovereign debt is vulnerable to doubts among investors about debt sustainability.

As the ECB notes in its report, steeper yield curves are a global phenomenon, with 30-year yields reaching multi-year highs across major advanced economies including the US, the UK and Japan. Investors are demanding higher term premia to compensate for fiscal and debt sustainability concerns.