Over the past decade, private debt has emerged as a mature asset class within global financial markets. It encompasses a range of non-listed loans, such as direct lending, mezzanine, venture, and distressed debt, originating from non-bank sources.

This market has grown rapidly, particularly in Europe, as regulatory changes and shifting risk appetites have encouraged borrowers to seek alternative financing. The aftermath of the Global Financial Crisis (GFC) was a turning point as banks tightened lending standards, paving the way for private lenders to fill the gap.

Typical private debt categories

Direct lending involves a loan that is bilaterally negotiated between a borrower and a single lender or a small group of lenders, with the expectation that lenders hold the loan until maturity.

Mezzanine debt is subordinate to primary debt, but senior to equity.1 It often includes an equity component, such as a warrant, which gives the lender an option to buy equity in the company.

Venture debt provides financing to venture capital-backed companies. Similar to mezzanine debt, it is a hybrid between equity and fixed income, often including rights embedded in the loan that allow the lender to buy equity.

Distressed debt involves lending to companies in financial distress. The key to success in this high-risk category is finding a good company with a bad balance sheet.

Special situation debt covers a wide range of loans characterised by unique factors or circumstances that influence the loan’s quality rather than the fundamentals of the issuer.

Key characteristics and advantages

A key characteristic of private debt is its illiquidity: these loans are not traded on public exchanges, making them harder to sell, but offering unique benefits.

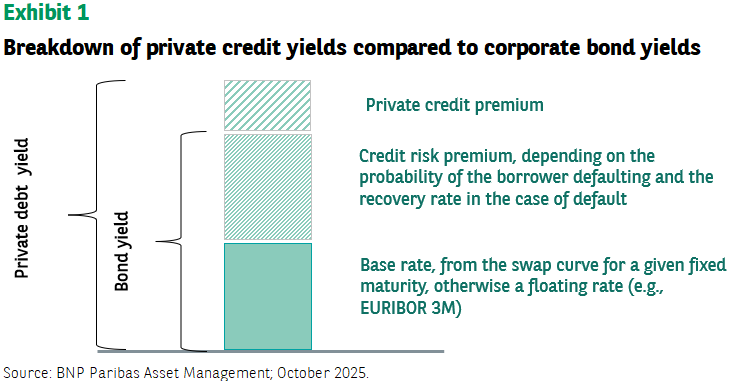

In private debt, there are bilateral agreements between the borrower and the lender(s) with limited bank involvement. Therefore, investors reap most of the rewards from financing the loan, and the illiquidity typically translates into a higher yield than for a comparable corporate bond.

This ‘illiquidity premium’ compensates for the risk and inconvenience of locking up capital for an extended period.

Market evolution and investment activity

The private debt market’s expansion is closely linked to the decline in traditional bank lending.

Direct lending has become the dominant strategy, representing half of all assets under management in the private debt market.

Of the activities financed with private debt, most concern leveraged buyouts and public-to-private transactions.

Financing these activities carries specific risks. Investors seeking a more diversified exposure to private debt should be aware of the high concentration of buyout-related debt in the market.

Returns, risks, and portfolio impact

Investors are drawn to private debt by its attractive risk-return profile.

The yield on private debt is composed of a base rate, a credit risk premium, and the illiquidity premium. While the returns appear stable given the less frequent valuations, this ‘return smoothing’ can mask underlying risks, especially during market stress.

Credit risk remains a central concern, but private loans often include covenants and security packages that can improve recovery rates in the event of default.

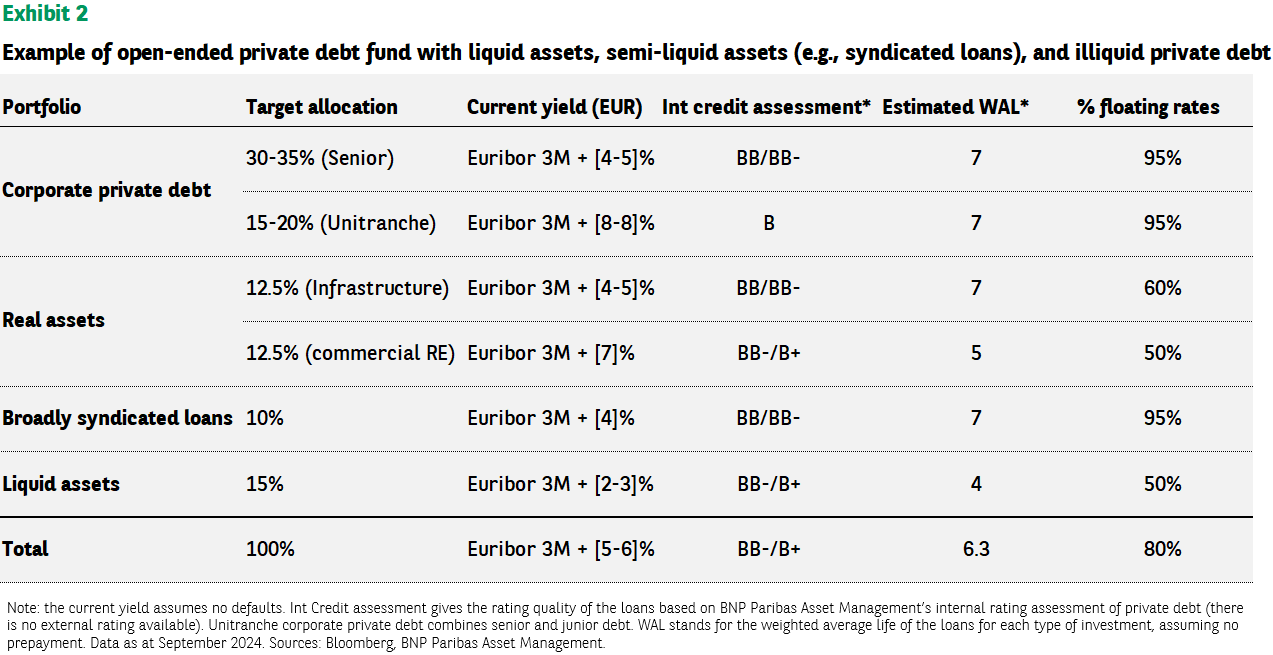

Most private debt is structured with floating rates, reducing its sensitivity to interest rate changes compared to fixed-rate bonds.

New fund formats and regulatory shifts

Traditionally, private debt exposure was limited to closed-ended funds with high minimum investments and long lock-up periods.

Recent regulatory changes, especially in the EU, have democratised access. The introduction of the European Long-Term Investment Fund 2.0 (ELTIF) regulation allows for open-ended funds that are accessible to retail investors.

These new structures offer greater flexibility, lower minimum investments, and enhanced liquidity management tools such as swing pricing and gating mechanisms which help protect investors during periods of high redemptions.

Conclusion

Private debt has matured as an asset class. It offers investors attractive returns and unique risks.

As regulatory reforms open the market to a broader range of investors, understanding the nuances of fund structures, liquidity management, and risk is more important than ever.

For those seeking yield and diversification, private debt presents compelling opportunities, provided they are approached with diligence and a clear grasp of the risks involved. For more details on private debt as an asset class details, see Navigating the Private Debt Landscape: Insights and New Fund Formats

[1] In terms of the priority of different sources of capital, senior debt creditors will be paid first in the event of financial distress, while shareholders will divide what remains after all creditors are paid