We expect corporate bonds to deliver positive returns in the coming quarters, primarily due to the attractive yields. With money market rates becoming less attractive as interest rate cuts loom, continued inflows into corporate bonds could provide additional support.

The main risk to our view is core US inflation remaining above the Federal Reserve’s 2% target level for longer than the market expects, taking interest rate cuts off the table . While such a scenario looks unlikely, in our view, and could be actually positive for investors attracted by current yields, the combination of inflation and high interest rates could soften risk appetite, eroding some of the demand the asset class currently enjoys.

US investment-grade corporate bonds – Attractive yields

The US has been the strongest economy in the developed world in recent quarters and the one most likely to lead global growth in the year ahead. The deceleration in company earnings seen in recent quarters is increasingly likely to pivot to a reacceleration – a view supported by robust company guidance in the most recent earnings reports.

While many companies remained cautious (to their long-term benefit) in the harder times, eventually lower interest rates should now both increase the availability of funding and reduce its cost, leading to greater enthusiasm for capital expenditures as well as mergers & acquisitions (M&A).

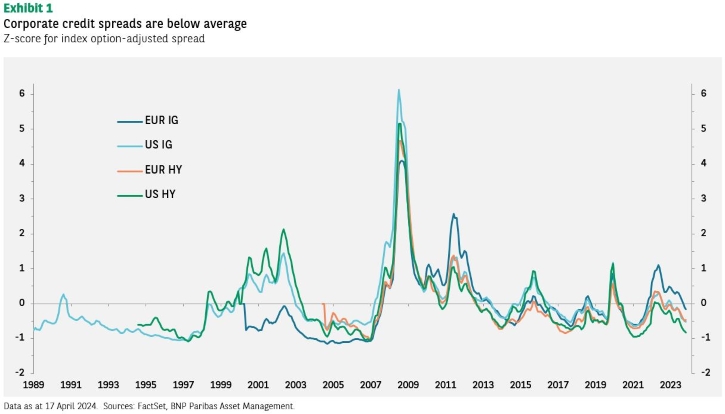

Aggregate yield spreads over US Treasuries have tightened modestly year-to-date (after a substantial rally in the final quarter of 2023) and are currently below the already tight levels seen before the COVID-19 pandemic. However, inflows into the asset class have been strong, from both domestic and overseas investors, and we expect this to not change.

Investment-grade (IG) credit’s absolute yields (currently at over 5.0%) are high by historical standards and lower interest rates should only increase the opportunity cost of holding cash. For investors seeking income, such as pension funds, current yields are the main attraction – not the possibility of capital appreciation due to further spread compression. In our view, investors could be rewarded for following their lead.

US high-yield credit – Cautious, but opportunistic

The outlook for high-yield (sub-investment grade) bonds in the US is less compelling.

The US economy, despite all its strengths and opportunities, has shown signs of weakening. The consumer, to take one example, has been impressively robust, but rising delinquencies (particularly among the lower and middle-income brackets) suggest its strength may be waning. Within the high-yield asset class, the average credit rating has been drifting lower, while an increase in distress ratios suggest a modest increase in corporate defaults is just a matter of time.

In our view, lower interest rates and a turnaround in growth are what is needed to make the high-yield asset class more compelling. While we expect both are coming in the quarters ahead, and inflows into the asset class could accelerate rapidly when the economic outlook improves, the current combination of patchy fundamentals and relatively high valuations suggests that a selective name-by-name approach to identify the higher- quality companies is warranted.

Eurozone IG bonds – Yield and potential for tighter spreads

The eurozone economy has been stagnating, largely due to tighter monetary policy and a more structural slowdown in Germany. However, we expect a mild recovery in the coming months, driven by the more peripheral countries and the broader services sector. As we also see core inflation reaching the European Central Bank’s 2% target in the second half of the year, we expect the ECB to begin a swift series of interest rate cuts mid-summer that results in the deposit rate falling to below 2% in 2025.

Meanwhile, corporate fundamentals have proven resilient, entering the downturn from a high starting point. The high level of cash held by many eurozone IG companies, for example, suggests they were well positioned to weather the recent economic environment. Current valuations are attractive for long-term investment: high yields offer a thicker cushion to absorb a further rise in yields before capital losses materialise.

However, we expect yields not to rise. We also believe that for the region’s bonds, all the conditions necessary to generate strong total returns in the coming quarters are in place: Attractive yields, a soft landing for the eurozone economy, aggressive interest-rate cuts, and robust demand.

Security selection is essential, however, as not all sectors and companies can be expected to perform equally well in this environment. We continue to favour the low-rated segments for the additional yield, while concentrating our exposure in non-cyclical sectors such as utilities, telecommunications, and some consumer sectors and companies with better-than-average earnings growth.

EU high-yield – More cautious, but still opportunistic

The market consensus on the outlook for eurozone high-yield bonds has coalesced around the idea that current yields (however high they may be) don’t adequately compensate investors for the many risks including weaker-than-expected growth, currently tight monetary conditions, the conflict in Ukraine, and the emergence of a more protectionist approach to strategic industrial sectors.

While we agree with this assessment in aggregate, we think it misses the trees for the forest.

Within the asset class, the higher end of the credit spectrum can offer attractive opportunities. While defaults are rising across the asset class, some single-B rated companies may be performing in line with expectations, have relatively low re-financing risks, greater potential in a lower-rate environment, and thus the capacity for a higher total return. Similarly, within individual industries and sectors, there can be compelling opportunities. For example, we continue to see value in higher- rated securities in the financials sector, such as AT1 paper in the banking sector, or selected bonds that mature in 2025 or 2026 from companies with low refinancing risk.