The second quarter earnings season has started off poorly. Earnings guidance from Samsung Electronics pointing to operating profit growth of nearly 20 times versus the same period a year ago saw the stock price drop by nearly 12% as the forecast was below expectations. Flash consensus earnings estimates for 2026 have fallen by 8% since.

By Daniel Morris, Chief Market Strategist

The market reaction illustrates how high investor expectations are, particularly for the technology hardware companies that have benefited disproportionately from the massive increase in investment supporting artificial intelligence technologies.

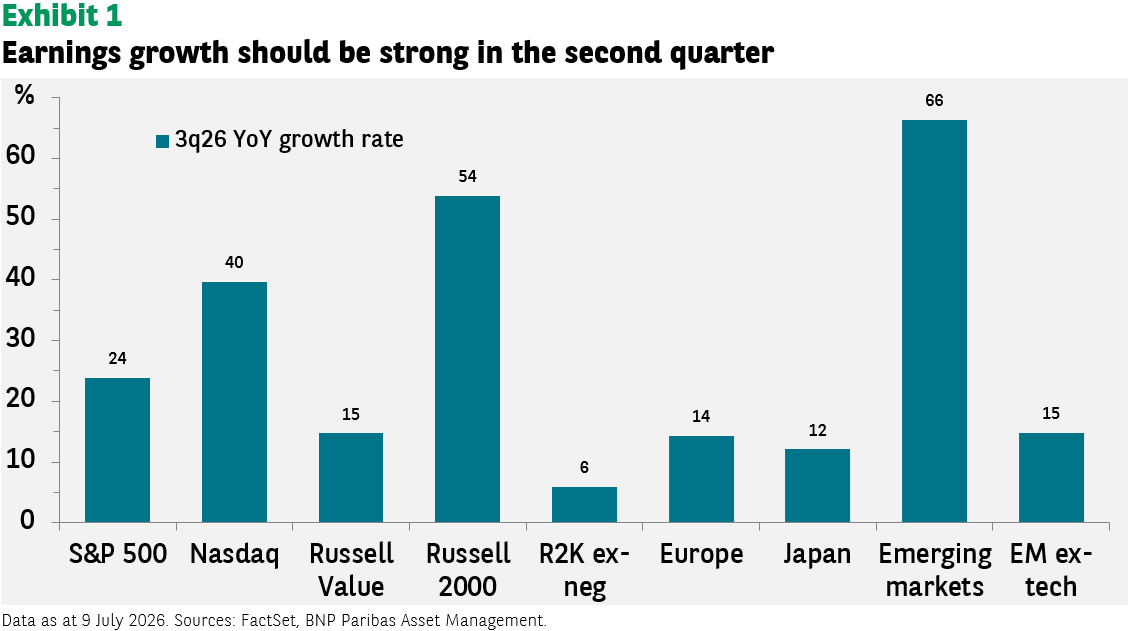

It is nonetheless likely to be a very good earnings season as far as actual results are concerned. Aside from the spillover from AI investments, tariffs and deregulation has boosted US corporate profits, with the S&P 500 forecast to see earnings growth of 24% this quarter (see Exhibit 1).

Not surprisingly, it is the technology stocks that are driving much of the growth, as evidenced by the 40% earnings-per-share gain expected for the Nasdaq 100 index.

But even for the rest of the market, growth is strong. Value stock earnings are expected to rise by 15%. Yet better is the 50% plus gain in profits for small cap stocks. This figure, however, is boosted by the large share of negative earners in the index. To what degree a smaller loss this quarter than a year ago can be considered earnings ‘growth’ is debateable. If you strip out the negative earnings, the growth rate for the Russell 2000 index drops to 6%. In terms of the correlation between EPS growth and price appreciation, which should be one-to-one if valuations are constant, the true earnings growth rate for the index is somewhere between these two extremes.

Other developed markets are also doing well, even if the figures appear lacklustre compared to the growth rates for technology stocks. Fourteen percent higher earnings for Europe are good for the region, and Japan is also in double digits.

The top of the charts is, however, emerging markets, where the biggest tech hardware winners lie. Here earnings are forecast to go up by 66%, but there is a wide gulf between the tech leaders and the rest of the market.

Emerging tech hardware earnings are expected to rise over 250%; for Korea the increase is nearly 10-fold. Exclude technology and earnings growth is a far more modest, but still respectable, 15%.

Tech sell-off

Given how high these forecasts are, it is not surprising that any disappointment is punished by the markets.

The risk that investors may be let down by the tech sector is higher simply because of the newness and power of the AI phenomenon and the inherent uncertainty about how the industry will evolve and who the winners and losers will be.

The key consideration, however, is that above-average volatility around these estimates does not change what for us looks to still be a strongly positive trajectory. The decline in estimates for Samsung Electronics’ 2026 earnings mentioned above lowered the forecasted growth rate from 590% to 535% for the year.

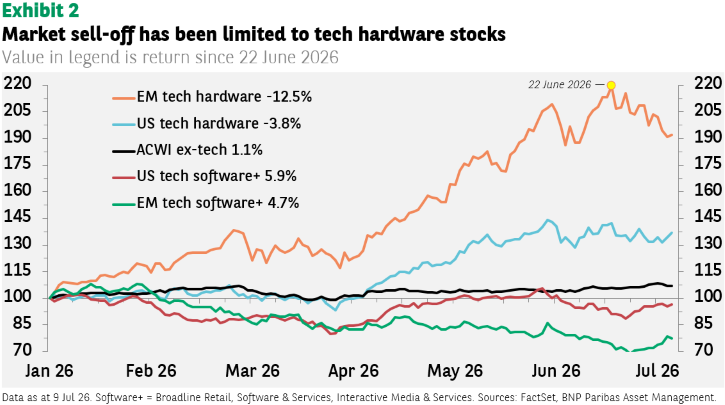

The correction in emerging market tech hardware stocks also needs to be put in context of the phenomenal price appreciation this year. At the peak in the index on 22 June, aggregate EM tech prices were up 120%, reflecting the increase in earnings discussed above, as opposed to higher valuations. Even now, after the declines, the advance for the year is around 90% (see Exhibit 2).

At the same time, the rest of market has risen, modestly for non-tech stocks (up 1.1%), and a bit more for non-hardware tech, reflecting the occasional phenomenon that what is good for companies providing the AI infrastructure is bad for those financing it. The returns also belie the notion that the bursting of any AI ‘bubble’ would lead to a broader collapse of equity markets.

Iran risk

Lurking in the background are worries about a restart of the Iran war. US President Donald Trump has declared the truce over (even as negotiations continue). While many investors had wanted to move on from the war, oil prices have jumped over the last week.

The reaction has been more modest than what was seen in March, with Brent up 6% versus a 12% gain after the initial hostilities. The subsequently much larger increases in oil prices in March came with the closing of the Strait of Hormuz, while the smaller gains now are occurring even as the Strait is effectively closing again.

The market’s reaction is seen by some as complacent, but it may rather be a more realistic appraisal of the potential impact of (temporarily) higher oil prices on the economy.

The medium-term impact of the earlier spike in oil prices on inflation and growth in developed markets seems to have been limited. The most pessimistic predictions that oil prices would only slowly return to pre-war levels due to damaged infrastructure in the Gulf and delays in getting ships through the Strait have turned out to be overwrought.

Oil analysts were again talking of a possible oil glut next year. The market’s implicit assumption seems to be that even if the Strait closes again, oil prices will revert to February levels fairly quickly once it reopens.

Data sources: FactSet, BNP Paribas Asset Management as of 9 July 2026 (unless otherwise stated). Past performance should not be seen as a guide to future returns.